Summary: Yangtze River Port & Logistics (NASDAQ:YRIV)

- We are of the strong opinion that Yangtze River Port & Logistics is a scheme run by its Chairman & controlling shareholder to siphon money away from U.S. public markets.

- YRIV’s only operating entity has been declared insolvent in China and is involved in multiple undisclosed legal proceedings, it has also been ordered to pay back at least $110 million in defaulted loans. YRIV fails to disclose the existence of these lawsuits & judgements in its SEC filings.

- Based on government-sourced documents and interviews with local officials, we believe that at least 77% of the company’s reported assets are fabricated.

- Specifically, YRIV claims to lease 1.2 million sq/m of land from a village that is only 610 thousand sq/m in size. Our investigator spoke to the village committee and they denied that any lease existed. This lease accounted for ~77% of YRIV’s balance sheet assets.

- On the ground visits to YRIV’s construction project during business hours on multiple occasions have shown virtually no signs of business activity aside from a lone gate guard.

- Cash from recent capital raises; has been siphoned to the CEO/controlling shareholder via related-party entities rather than deployed towards the company’s supposed construction projects. Based on our findings we think YRIV is a total zero.

Introduction

We believe that Yangtze River Port & Logistics (NASDAQ:YRIV) is an artifice designed to enrich the company’s Chairman & controlling shareholder. The company currently trades at a market cap of about $2 billion as of this writing. We are confident that it will ultimately be delisted and that every penny of its market cap will be wiped out.

The company has generated no revenue over the past 3 years and its U.S. headquarters is based out of a New York City apartment. Site visits to the company’s Chinese properties, interviews with local officials, and a detailed examination of Chinese and U.S. filings; lead us to believe that the company’s assets have either been grossly exaggerated or are largely fabricated.

Our report includes several areas of research that are either completely new or not fully covered in other reports. These should help investors finally put the pieces of the puzzle together to reach the same conclusions we have reached about YRIV:

- Worthless / Overinflated Assets

YRIV has essentially one project called the Wuhan Yangtze River New Port Logistics Center:

- The constructed part of the project is a cluster of commercial buildings. The company claims that 4 of the buildings in the complex are completed, ( F-12) yet they have failed to produce any revenue from them. A site visit to the properties during working hours found them to be a veritable ghost town; with no signs of activity aside from a gate guard.

- The unconstructed part of the project is a planned “Logistics Center” that YRIV states it will build on 1.2 million square meters of land leased from a local village. On YRIV’s latest quarterly balance sheet, the rights to the land are reported as having a value of $299 million, comprising over 77% of the company’s total assets. ( F-13) Despite claiming to lease 1.2 million square meters from the village, our government-sourced maps show that the total area of the village is only 610 thousand square meters. Moreover, conversations with officials from the village in question revealed that contrary to the company’s claims, YRIV has not leased any land from them.

- Undisclosed Legal Judgements

Despite the company’s SEC filings, which state that there are no material legal proceedings against the business, we found Chinese court records showing that the company has at least 11 judgements filed against them totaling RMB 766 million (USD $110 million).

The company reports total assets of $386 million in its SEC filings (pg. F-1), but we found local court records showing that creditors were unable to locate assets to seize in their attempt to satisfy one of YRIV’s multiple legal judgements. The Chinese court has recently taken the extraordinary step of placing the company on its list of “untrustworthy debtors” due to its mass of unpaid judgements.

- Cash from Capital Raises Have Gone Right to the Chairman

The company issued 19 convertible notes this year alone. (pg. F-16) So where did the money go? Rather than using the proceeds of these notes to advance the company’s purported real estate projects, money instead has gone directly to related-party entities affiliated with the company’s Chairman & controlling shareholder, Liu Xiangyao. Proceeds from past capital raises have similarly ended up being diverted to Xiangyao.

Background

Yangtze River Port and Logistics Limited, is a Nevada holding corporation that originally became public via a reverse merger in December 2015 (pg. 6). YRIV operates through its wholly-owned Chinese subsidiary, Wuhan Yangtze River Newport Logistics Co., Ltd (“Wuhan Newport”).

The company recently attempted to reverse merge into a different entity called Wuhan Economic Development Port Limited (the “Wuhan Port”). The deal fell apart shortly after a Barron’s article questioned the deal’s bizarre rationale:

“It’s puzzling that Yangtze’s board and controlling shareholders want to exchange the Wuhan project for assets worth a mere quarter of company’s total market value. Since last December, Yangtze has been trying to complete a deal in which it would pay $90 million to swap everything it owns for another riverfront business in Wuhan that the company’s own filings appraise at just $454 million. That would appear to leave Yangtze stockholders with something worth just $3 a share.”

On the ground due diligence regarding YRIV’s business operations was completed in the summer of 2018 and we concluded that YRIV’s Wuhan Newport is collectively worth nothing. We waited to see how the deal played out (it eventually collapsed), which leaves Wuhan Newport as the sole operating entity of the company. (pg. F-5) We then followed up with another site visit yesterday to re-confirm our findings.

Evidence Shows That YRIV’s Claim to Its Main Asset Is Likely Fabricated

The unconstructed part of the project is referred to as the Logistics Center, from which YRIV anticipates their “main source of expected income will be derived.” (pg. 3) The Logistics Center is expected to span approximately 1,918,000 square meters. (pg. 4) Based on information presented on YRIV’s website, the layout of the Logistics Project is as follows:

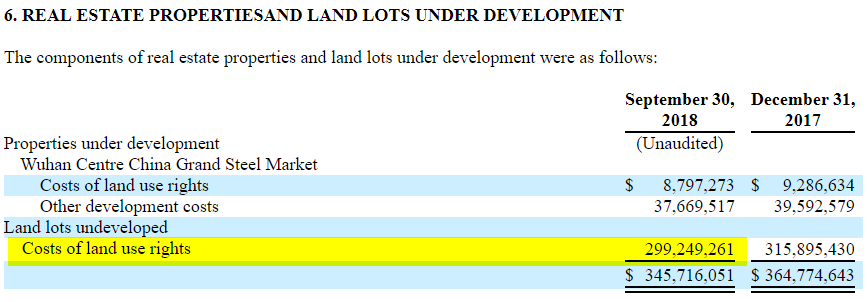

The company’s latest quarterly financials (pg. F-13) break out the company’s assets relating to “Real Estate Properties and Land Lots Under Development.” These assets consist of the Wuhan Centre (the company’s other real estate project) and “Land lots undeveloped”, which, by inference, is the Logistics Center:

Given that the company reports total assets of $386 million (pg. F-1), the undeveloped Logistics Center land use rights comprise over 77% of the company’s total asset base.

The Logistics Center is intended to be built on 1.2 million square meters of land leased from Chunfeng Village. The most recent 10-K highlights this (pg. 33):

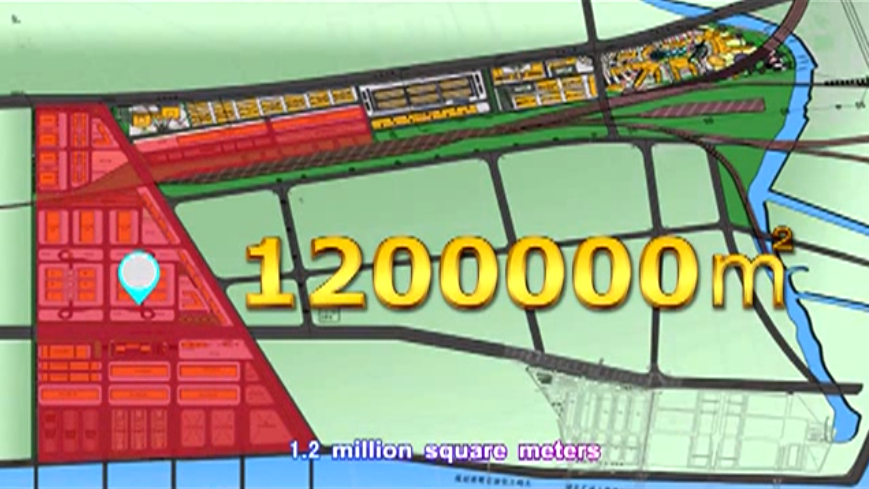

On YRIV’s website, a promotional video displays the 1.2 million square meter leased land area at the 10:51 mark in describing its proposed location of the Logistics Center:

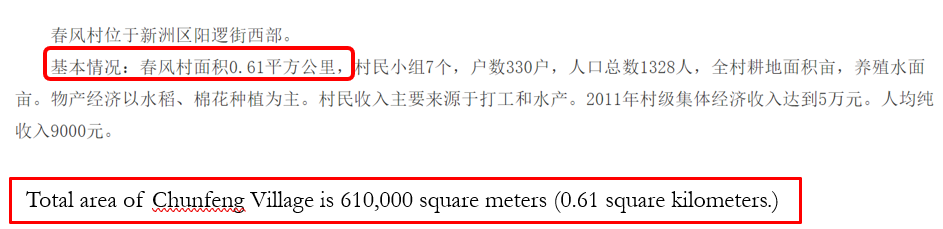

Our first clue that something was amiss came from the Hubei Provincial Government sourced records, which show that the total area of Chunfeng village is 610,000 square meters; only half the size of the area YRIV claims to lease from the village:

Our on the ground team visited the village to inquire with local officials about the discrepancy. Here are some photos of the village, and of the Chunfeng Village Committee from the visit of our due diligence team:

Our team spoke with officials in the village committee and asked about their relationship with YRIV. When asked if they leased any land to the company, they replied that they had not. We also confirmed that the village is currently only 0.61 square kilometers.

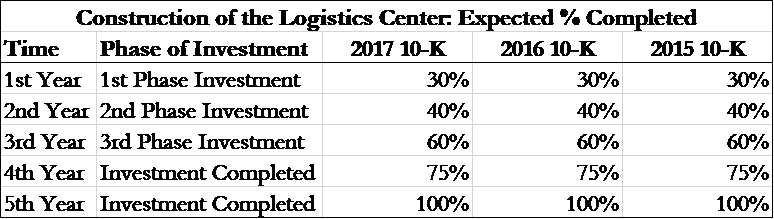

Given the above, it comes as no surprise that the company has reported that its Logistics Center has been stalled for at least three years. The company’s last three 10-Ks describe the anticipated completion of construction on the Logistics Center and show literally zero progress:

(Source: 10-Ks from 2017 [pg 2], 2016 [pg 2], 2015 [pg 4])

Going one level deeper, we found further evidence that the company’s “plan” to build a 1.2 million square meter facility on a plot of land half that size did not comport with geographic reality.

After consulting with local authorities and villagers, the on the ground team learned that most of the area YRIV claimed to lease from Chunfeng Village actually belongs to Junming Village (军民村), Jiangdi Village (江堤村) and/or the Huayou Pipe Base (华油管道基地). Chufeng Village barely overlaps with the area YRIV claims to lease.

We marked up an area map as shown below taken from Google Maps:

All told, we think the supposed leased land for the Logistics Center is a total fabrication.

YRIV’s Constructed Part of the Project Looks Abandoned: We Found Virtually No Signs of Commercial Activity During Our Site Visits

YRIV’s constructed part of the project is a commercial building project formerly called the Wuhan Centre China Grand Steel Market. The project claims to cover an approximate construction area of 222,496.6 square meters (pg. 3). YRIV’s filings state that it sold approximately 22,780 square meters of commercial building space relating to this project.

The company’s latest 10-Q reports an asset value of over $76 million for the completed and in progress buildings and the land use rights related to the constructed part of the project. (pgs. F-12 – F-13)

After visiting the project site our team found that while some of the buildings do indeed look completed, the area appears to have been abandoned. Our first visit was in June 2018 during business hours. Our team saw no signs of commercial activity except for a gate guard. The team saw no other people, saw empty buildings with no movement inside, and heard no sounds that would indicate activity. Some of the properties were overgrown with shrubbery. Overall, the site struck us as a small ghost town. For accuracy, we visited again the site within 24 hours of publishing this article. Here are some photos from the recent visit to the site from 24 hours ago:

We have a very difficult time believing that these empty buildings (in an apparently abandoned location) have a value of anywhere near the $76 million reported by the company.

YRIV Has Numerous Undisclosed Legal Proceedings & Judgements Against it and Its Operating Subsidiary Has Been Declared Insolvent in China

YRIV has repeatedly claimed that they are “not involved in any litigation that [it] believe[s] could have a materially adverse effect on [its] financial condition.” (Source: 2018, 2017) Despite those representations, our research indicates that the precise opposite is in fact the case: the company’s operating subsidiary, Wuhan Newport, has so many claims and default judgements against it that it has been declared insolvent in China, according to our search of Chinese court databases.

In just one example, China Construction Bank is litigating with YRIV’s operating subsidiary, Wuhan Newport, regarding $44 million in loans to the company. The loan is disclosed in YRIV’s filings (pg. F-17):

However, the litigation relating to the exact loan is not disclosed in YRIV’s SEC filings. Here is the Chinese and English translation of the litigation:

原告建行钢城支行诉称,2014年5月28日,原告与被告新港公司签订编号为GCDK2014-090号《固定资产贷款合同》(以下简称贷款合同),约定新港公司向原告借款29000万元,期限6年(2014年5月30日至2020年5月29日),贷款利率为基准利率上浮5%,按季结息;

……

原告于2014年5月30日依约向新港公司发放了贷款29000万元,但新港公司并未依约还款付息,担保人亦未履行担保责任,且新港公司、人和公司已出现涉及重大法律纠纷等情形。根据《贷款合同》的约定,原告有权宣布贷款立即到期并要求新港公司立即偿还《贷款合同》项下的所有到期及未到期的本金、利息和费用。

Translation:

The plaintiff China Construction Bank Gangcheng Branch states, on May 28, 2014, the plaintiff and the defendant Wuhan Newport executed No. GCDK 2014-90 Fixed Assets Loan Agreement (“Loan Agreement”) and stipulated that Wuhan Newport borrowed RMB 290 million from the plaintiff with the term of six years (May 30, 2014 to May 29, 2020), the interest shall be the base interest plus 5 % and quarterly interest payment.

The plaintiff (China Construction Bank) disbursed the loan payment RMB 290 million (USD 44 million) to YRIV on May 30, 2014. However, YRIV did not repay the interest and principal and the guarantor (Renhe Corp. the former shareholder of YRIV) did not perform its guarantee obligation. YRIV and Renhe Corp. were already involved in severe litigations.

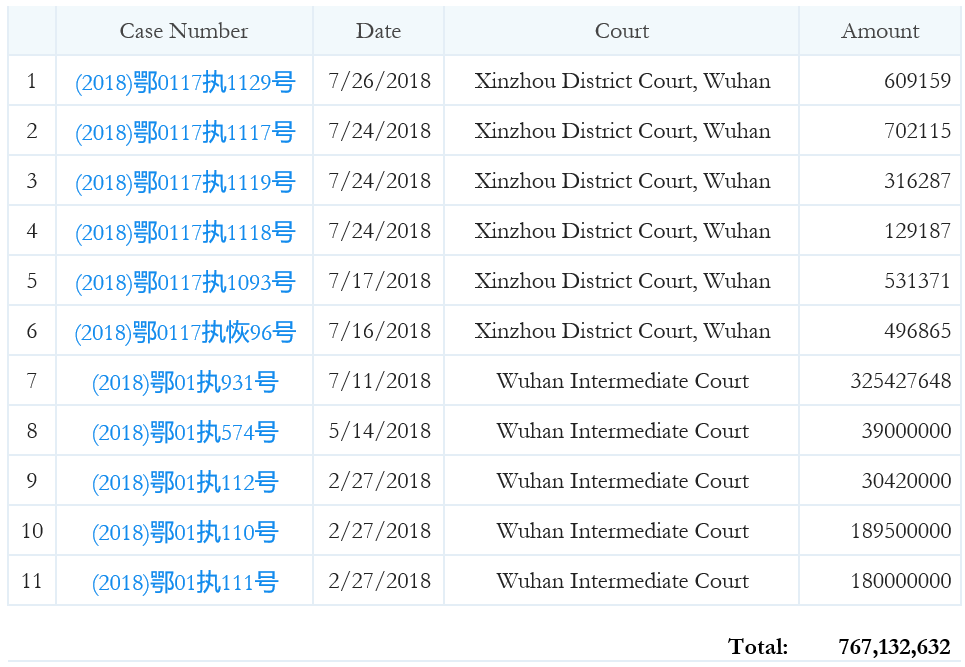

In addition to the above mentioned China Construction Bank litigation, in 2018 (February 27, 2018 to July 27, 2018), Wuhan Newport was subjected to at least 11 final judgements totaling RMB 767,132,632:

As Wuhan Newport cannot repay its legal obligation under these judgements, it has been added to the local list of dishonest judgement debtors. This means that in the event that Wuhan Newport (the operating subsidiary of YRIV) receives any investment money from its investors, it’s already earmarked to fulfill its outstanding debt.

Barron’s recently reported on some of the company’s litigation issues and asked the company why they were not disclosed to investors. The company’s rationale was that those issues would disappear once it closed the asset swap deal with Wuhan Port:

“Asked about these cases, Yangtze told Barron’s that its SEC filings don’t mention the bank’s court award because Yangtze’s proposed asset swap will unburden it of the Newport unit. ‘[I]f the sale is successful,’ the company said in an email responding to our questions, ‘the Purchaser will be responsible for repaying the loan to the bank.’”

“…Yangtze’s planned exchange of businesses will cure all these headaches, director Coleman said in an interview. ‘All the liabilities associated with the old project, bank loans and what not, transfer completely over to the new owners,’ he told Barron’s. ‘Any and all of these issues are then gone.’”

The latest S-3 registration statement filed by the company, shows that the contemplated business exchange referenced by the company in the Barron’s article has been terminated.

Yet, despite the termination of the company’s “excuse” for not disclosing its ongoing material legal proceedings, the company claims in the very same filing that they are not involved in any material litigation:

“We are currently not involved in any litigation that we believe could have a materially adverse effect on our financial condition or results of operations.”

In its most recent 10-Q, without the asset swap deal, the quarter reflected YRIV’s third quarter business operations. The company continues to claim that YRIV does not have any litigation and, of course, YRIV did not disclose the RMB 767 million (USD 110 million) in outstanding judgements against its main operating subsidiary, Wuhan Newport.

We think that the above is the most obvious 10b-5 Securities Exchange Act violation since “Funding secured”, and we believe that it could result in a halt of YRIV shares at any time.

Money from YRIV’s Capital Raises Has Been Used to Pay the Chairman/Controlling Shareholder Rather Than Advance Company’s Projects

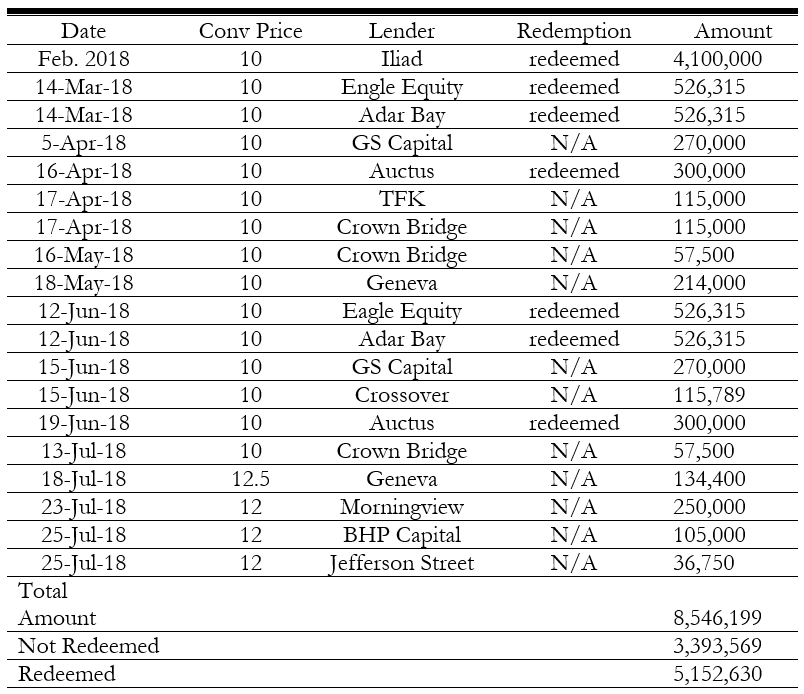

The company had 19 convertible note issuances this year alone, according to its latest quarterly filing. (pgs. F-15-F-16)

As we stated before, as YRIV’s operating entity, Wuhan Newport, has been labeled as a dishonest judgement debtor, and money that goes to Wuhan Newport will be used to fulfill its outstanding legal judgements. Therefore, we believe it is impossible for Wuhan Newport to come up with cash to continue its logistics center project.

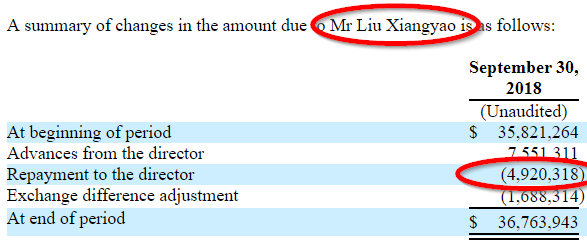

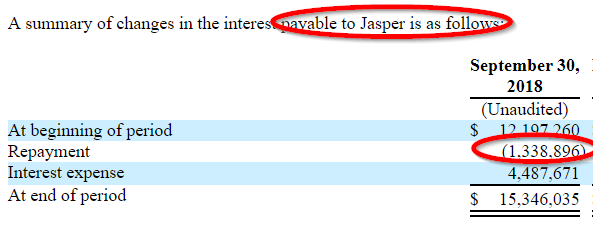

So where does all the new cash go? YRIV has consistently reported large liability balances “due to related parties” on its financial statements. These in turn seem to accrue large interest rates which simply get added to the “advances” over time. When capital is raised, cash is then used to pay back the supposed related-party “advances”, rather than being employed to further the company’s projects.

In the September 2018 quarter alone, the CEO and controlling shareholder, Liu Xiangyao, was “repaid” $6.2 million dollars both directly and through an entity he controls called Jasper Lake Holdings (“Jasper”):

In the June 2018 quarter, the CEO was “repaid” $1.3 million, along with another $3 million in the March 2018 quarter. Based on the disclosure, the total amount of those 19 convertible notes amounted to $8.5 million, of which $3.39 million is outstanding while $5.15 million has been redeemed. We can therefore infer that raised cash from these convertible notes went to the Chairman, not to the business operations of YRIV.

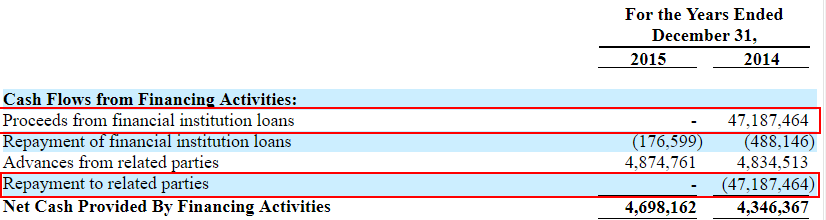

These supposed repayments are not new for YRIV. In fact, financials presented as part of YRIV’s reverse merger show that the company took out a $47.2 million construction loan from China Construction Bank in the year ending December 2014 (pg. F-16).

The company turned around and paid out all of it as a “repayment to related parties” (pg. F-6).

Based on these observations, we believe that YRIV is largely a shell which exists to raise more capital for the personal use of its controlling shareholder and chairman.

Conclusion: We Think Yangtze River Port & Logistics Is Worth Nothing

Over the last decade, numerous China-based companies have been ousted from U.S. markets. Generally, the most egregious cases occur when companies funnel wealth and value from shareholders to insiders. Since the implosion of the U.S. listed China-based space between 2010 and 2014, we didn’t think we would ever come across such obvious cases again.

To anyone who thinks the China Hustle has ended:

- We encourage you to consult an official map, which clearly shows that the Chunfeng Village is only 610,000 square meters in size despite the company claiming to lease 1.2 million square meters of land from them.

- We encourage you to review the readily available filings from Chinese courts showing the litany of judgements against the company that are undisclosed in their SEC filings.

- We encourage you to simply visit the apparently empty cluster of buildings it claims to be of great value.

Best of luck to all

Disclosure: We are short YRIV.

Full Disclaimer: Use of Hindenburg Research’s research is at your own risk. In no event should Hindenburg Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Hindenburg Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in all stocks (and/or options of the stock) covered herein, and therefore stands to realize significant gains in the event that the price of any stock covered herein declines. Following publication of any report or letter, we intend to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation, conclusions, or opinions. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Hindenburg Research is not registered as an investment advisor in the United States or have similar registration in any other jurisdiction. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Hindenburg Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Hindenburg Research does not undertake to update or supplement this report or any of the information contained herein. Hindenburg Research and the terms, logos and marks included on this report are proprietary materials. Copyright in the pages and in the screens of this report, and in the information and material therein, is proprietary material owned by Hindenburg Research unless otherwise indicated. Unless otherwise noted, all information provided in this report is subject to copyright and trademark laws. Logos and marks contained in links to third party sites belong to their respective owners. All users may not reproduce, modify, copy, alter in any way, distribute, sell, resell, transmit, transfer, license, assign or publish such information.

26 thoughts on “Yangtze River Port & Logistics: Total Zero. On-the-Ground Research Shows Assets Appear to be Largely Fabricated”

Comments are closed.

Actually no matter if someone doesn’t be aware of then its up to other viewers

that they will help, so here it occurs.

Wow! After all I got a website from where I be able to actually

obtain useful data concerning my study and knowledge.

Generally I do not learn post onn blogs, however

I wish to say that this write-up very forced me to

take a look at and do it! Your writing style has been surprised

me. Thanks, quite nice post.

Great job! $11 to $1 in 3 months.

Great job? These people are vultures….

Doubt you’ll win the lawsuit though. You can’t say stuff that isn’t true and expect nothing to happen to you……

Curious about this company? I see cranes in background of the building pic, what being constructed in back of that bldg ?

We shall find out the truth soon…. #YRIVBULL

How much will you settle out of court for on this one?

Since you are shorts, of course this is manipulated rather than someone without a position. This article is therefore written in your best interest. Also just the title shows manipulation. “Is worth NOTHING”. If you know anything about shell companies, they are worth something. They are shells looking for public companies to reverse merge and trade on NASDAQ at a premium cost of millions of dollars which is cheaper than having to not reverse merge. These shell companies can be worth 40-80mil. But of course you deny these facts with one sided arguments.

Actually when someone doesn’t know then its up to other people that they will

assist, so here it occurs.