- Temenos (SWX:TEMN) is a ~$7.5B market cap Swiss-listed banking software developer and services company that serves 3,000 customers globally and reported $1 billion in preliminary 2023 revenue.

- Our 4-month investigation into Temenos, involving interviews with 25 former employees, including senior leaders at the company, uncovered hallmarks of manipulated earnings and major accounting irregularities. This includes evidence of roundtripped revenue, sham partnerships, rampant pulling forward of contract renewals, backdated contracts, excessive capitalization of seemingly non-existent R&D investments, and other classic accounting red flags.

- These aggressive accounting practices seemed to be an open secret among many of the former employees we spoke with. Several indicated that CEO Andreas Andreades encourages the practices, which help gloss over significant customer product dissatisfaction and attrition.

- In October 2021, Temenos announced a strategic partnership with fintech Mbanq to “accelerate banking-as-a-service adoption across the US,” its key strategic market. According to a former Temenos executive, the deal involved Mbanq purchasing $20 million in software and services from Temenos.

- Litigation records, financial statements, and former Temenos executives evidence that Temenos secretly funded the purchase of its own software- effectively engaging in a roundtripping scheme by making an undisclosed ~$20 million investment into Mbanq around the same time as the software purchase.

- A former Temenos executive told us, “The convertible note was signed the same day, the same hour as the deal was signed for Mbanq … because they [Mbanq] couldn’t have signed it if they didn’t have the money.” They added, “If that was in the US and that was with the SEC, everyone would be out.”

- In February 2021, Temenos announced a partnership with US-based banking software company DXC Technology, which a former DXC executive told us entailed DXC buying approximately $8-10 million in software licenses from Temenos.

- While Temenos repeatedly assured shareholders that the DXC partnership was “game-changing” and would “accelerate our penetration” with large banks in North America, a former DXC executive told us the deal was “rushed through” on the last day of the year to “help Temenos make their yearly number”. They said of the deal: “This isn’t a partnership. You used us for a license sale.”

- According to the executive, the deal was subsequently terminated due to inaction on Temenos’ part, leading to an eventual ~$8 million write-off for DXC, saying “they [Temenos] left us at the altar … we gave them a bunch of money and then they literally walked away.”

- A former Temenos executive confirmed that the partnership failed, saying, “[DXC] had to write that off [their] books…” and told us the deal was “typical Temenos” and all about “selling and quick hits.”

- Throughout our research, 4 different former Temenos employees corroborated the practice of pulling forward license renewals, often at discounts, to boost short-term earnings while cannibalizing future renewal revenue. One former executive told us, “If there’s a renewal that they can pull forward, they’re going to go and be very aggressive about doing that, and that’s what happened.”

- Another executive described the effect of aggressive pull forwards by citing Temenos’ record-breaking revenue in 2019, saying, “When outside investors were looking at this, they thought ah, the licensing is growing and we’re getting new customers. The reality is the new customer sales were coming down…”

- When asked about pulling forward renewals, a former salesperson simply told us, “I just thought, you know what… there’s going to be some accounting scandal at some point…”

- A former Temenos executive told us that the company also regularly backdated contracts to shift earnings to earlier quarters, saying, “… the standard practice, which was known completely and condoned by Andreas and Max [current and former CEOs], but denied in public, was that the legal teams would give power of attorney to the sales teams to backdate a deal that had come in, you know, after the end of the quarter.”

- A former sales leader from Temenos corroborated the practice of backdating, saying, “Don’t trust any of the public information … including the analyst call, okay? … I’ve seen deals closed in January that they were pulled back to the previous quarter, okay? They do that.”

- Temenos states that it invests 20% of its revenue back into R&D, “more than twice the level” of its closest competitors. Former senior Temenos executives told us the advertised R&D spend was “non-existent” and a “mystery.”

- One former Temenos executive told us the majority of Temenos reported R&D investments were actually customer-specific implementation costs: “All you’re doing is just taking something that was custom for a customer and saying it’s R&D. It’s not. That’s the majority of it.”

- In 2022, Temenos’ R&D capitalization rate was 62% higher than peers, resulting in an estimated $86 million of already questionable R&D costs being shifted to the balance sheet. Compared with the peer average capitalization rate, Temenos’ capitalization led to an estimated 29.5% artificial boost to its 2022 pre-tax profits.

- In 2023, Temenos extended its allowable amortization period for “internally generated software development costs” from 5 years to 7 years, allowing it to recognize these capitalized costs even more slowly than before, with zero disclosure about its impact on its financials. We estimate the change will allow Temenos to artificially boost 2023 profits by up to 8.7%.

- Temenos also has almost double the Days Sales Outstanding (DSO) of its closest peers at 124 days, a classic sign of aggressive revenue recognition policies and difficulty collecting on reported revenue.

- Despite the Mbanq and DXC partnerships seemingly failing to yield new business in North America, Temenos continues to highlight the region as its key strategic market and driver of growth, projecting it will soon account for 45-50% of software licensing revenue due to Temenos’ “leadership vision” and “superior technology.”

- Our research uncovered a series of failed implementations and frustrated customers in North America. One former Temenos executive said, “Clients were falling out the bottom of the funnel, so to speak, as fast as we could fill it at the top” due to CEO Andreades refusing to look at “deficiencies in the product…”

- Another former Temenos employee said Andreades would often pitch non-existent products to prospective customers, telling us “Andreas or (former CEO) Max would be going into a meeting and they didn’t have a brochure for the feature that didn’t exist… and it had to be on their desk by the time they got to the client. For a feature that hasn’t been thought of, not run by product, not run by anybody sensible…”

- US-based Unify Financial Credit Union signed on with Temenos in September 2018. It sued Temenos for fraudulent inducement and negligent misrepresentation by December 2021, claiming that Temenos oversold its cloud capabilities and that its software was so unstable that Unify had to revert to its old system 2 months after going live.

- US-based First Fidelity Bank signed on with Temenos in December 2019. It sued Temenos for breach of contract and fraudulent misrepresentation in 2022, saying it was “fed up with Temenos’ excuses and delays.”

- US-based Grasshopper Bank went live with Temenos’ core software in 2019, only to abandon it 4 years later after numerous implementation issues. A former executive from Grasshopper told us that its entire new bank launch was put on hold “largely because of Temenos’ implementation strategy”, which they described as “excruciating”.

- US-based Varo Bank went live with Temenos’ core banking software in September 2020, and is currently highlighted as a “success story” on Temenos’ website. Former Varo employees described the implementation as a “horrible experience” that left them “forever scarred.”

- One former Varo executive told us, “Nothing was out of the box, even though everything was sold as out of the box” and that “literally nothing worked.” The executive claimed that Varo took millions in losses due to issues with the Temenos implementation.

- In 2019, Temenos formally announced “Temenos Infinity,” an attempt to diversify beyond core banking software by rolling $840 million of acquisitions into a new division focused on “digital banking” products. As recently as its 2023 Capital Markets Day presentation, Temenos has continued to tout Infinity as a successful entry into digital banking that represents an addressable market as large as core banking.

- Former Temenos executives, partners, and customers confirmed dozens of failed Infinity implementations, with one former Temenos executive calling the entire division “a huge destruction in value”, saying that “a whole Infinity team of 20 or 30 salespeople” got “canned.” A second former employee confirmed that Temenos “axed pretty much everybody in Infinity” over the last year. A third said “the top talent that supported that product [Infinity] left.”

- A former Temenos executive told us that the great majority of North American Infinity implementations simply failed, saying, “Let’s see, in 2021, we had 19 clients in North America… that were supposed to go live [on Infinity], and 2 of those 19 went live… tons of client cancellations, frustrated, angry clients.”

- We also found evidence of failed Infinity projects in the Middle East, Asia, and Australia. We spoke with a former manager from NDC Tech (now Systems Limited), one of Temenos’ implementation partners in the MENA region. They also confirmed widespread Infinity failure, saying, “… around 20+ banks in 3 years onboarded with Infinity … but honestly, out of those 20+ banks, only 2 or 3 banks were able to go live.”

- Finally, we were told by a former senior Temenos executive that CEO Andreades admitted in a closed door meeting that Infinity had failed. The executive said, “He [Andreades] literally said… we’ve gotten nowhere with Infinity in 3 years, we need to just, you know, toss it overboard [and] be done with it.”

- Many of Temenos’ most highlighted deals in Europe and Australia have been plagued with delays, cost overruns, and regulatory issues, despite Temenos’ posturing to the market that the deals have been major successes.

- In 2015, Nordea signed on for what was supposed to be a 5-year core banking transformation with Temenos, representing the largest deal in Temenos history to that point. Today, the deal is touted as a success story by Temenos.

- However, Nordea reportedly experienced cost overruns, delays, and its Chief Banking Officer resigned in May 2021 amidst reports that the bank’s core banking transformation had slowed. A former Temenos executive called the implementation “absolutely terrible” and confirmed that the Nordea transformation was still ongoing nearly 9-years after kick-off.

- In 2016, the Bank of Ireland selected Temenos to be “at the heart” of its €500 million technological transformation. The project budget reportedly tripled over 5 years, led to wide-ranging IT failures and a $139 million impairment for the bank.

- A former IT manager from the Bank of Ireland told us Temenos over-promised and under-delivered, saying Temenos’ software “couldn’t handle” the bank’s needs. The former manager said that the Temenos team was sometimes more focused on “just trying to sell more software…”

- In May 2018, Australia-based BNK Banking announced it had gone live with Temenos’ cloud banking software, but in July 2023, BNK was hit with 18 infringement notices from Australia’s banking regulator due to flaws in Temenos’ software, per a BNK spokesperson to the media.

- BNK is now leaving Temenos mid-contract according to an Australian banking consultant familiar with the company who told us, “Honestly, an Excel sheet would work better than Temenos, and that’s being gentle. It is horrendous … they have cost [BNK] what we believe to be over $100 million worth of lost opportunity.”

- An Australian banking consultant that worked on Temenos implementations summed up his view of Temenos as a “just a fantastic sales company and just a sales machine, but honestly can’t back it up with anything… the most difficult vendor I’ve ever come across. They promised us the world. It was all vaporware, basically…”

- While institutions like Baillie Gifford, Fidelity and Fundsmith, have accumulated significant positions, Temenos executives have dumped $1.1 billion in stock over the last 10 years, per Bloomberg.

- Temenos trades at a fundamental premium to its peers, representing significant downside even if one were to ignore all the findings of our report. Consensus estimates show it trades at a 76% earnings premium, a 41% EV/revenue premium, and a 59% EV/EBITDA premium.

- In its quest to seemingly do just about anything to prop up its earnings and boost its stock price, Temenos finds itself on the classic accelerating accounting treadmill. We expect it will soon run out of accounting tricks, new unwitting customers who believe its glossy sales pitches, and new investors willing to buy as executives continue to sell.

- Temenos says it “takes every step to be as open and forthcoming as possible with data” and that it will fully investigate claims of “concerns or improper conduct.” With this commitment to transparency in mind, we have included 36 questions at the end of this report.

Initial Disclosure: After extensive research, we have taken a short position in shares of Temenos AG (SWX:TEMN). This report represents our opinion, and we encourage every reader to do their own due diligence. Please see our full disclaimer at the bottom of the report.

Background & Basics: A $7.5 Billion Swiss-Listed Banking Software Developer And Services Company

Temenos AG (SIX:TEMN) is a CHF 6.6 billion (US $7.6 billion) market cap Swiss-based banking software company founded in 1993. It went public on the SIX Swiss stock exchange in June 2001. It is led by CEO and former Chairman Andreas Andreades, who initially joined the company as Chief Financial Officer in 1999.

Temenos offers a range of products and services, but is primarily focused on its legacy core banking software, called “Temenos Transact,” which serves as the back-end ‘nervous system’ of a bank, underpinning massive volumes of basic transactions such as deposits, withdrawals, transfers, and more complex functions.

Temenos’ other key offering, “Temenos Infinity,” is a newer suite of front-end, consumer-facing digital banking solutions, which it says helps financial institutions “reimagine the way that they engage with their customers.” [Pg. 1]

Most of Temenos’ primary end users are banks and financial institutions like PayPal, Nordea Bank, and Bank of Ireland.

Temenos’ website says it is the 3rd largest software company in Europe, serving 3,000 clients in 150 countries and enabling banking for over 1.2 billion people. On January 19th, Temenos reported preliminary 2023 revenue of $1 billion.

Bull Case: Sticky Core Banking Product, A Modernized Cloud-Based Offering, Industry Leading R&D And Takeover Rumors

Over 3 decades of operations, Temenos has built a “sticky” client base due to how time-consuming and complex it can be to transition between banking software providers. As a result, many banks still use legacy systems that are 2 to 3 decades old, according to Deloitte.

One way Temenos benefits from these relationships is from maintenance fees associated with its installed base of software, which amounted to $423.7 million as of the company’s preliminary 2023 report.

Beyond Temenos’ 30-year track record of sales with its legacy core banking software, it is focused on the future with its investment of 20% of revenue back into R&D. Temenos says this is “the highest rate in the industry” and double that of its closest competitors, saying its R&D investment ensures that its software “never becomes legacy.”

Temenos’ forward-looking strategy aims to transition from on-premises core banking installations to a modernized cloud-based offering, a new SaaS (Software-as-a-Service) billing model, and a relatively new suite of digital banking products that live under the “Infinity” brand.

Over the last few years, Temenos’ “partner first approach” has resulted in several key strategic partnerships that aim to push it into new markets. One such market is North America, which accounted for 37% of 2022 software licensing revenue, which Temenos aims to increase to 45-50% in the mid-term.

Temenos’ share price has declined by 35% over the last 5 years, partially due to revenue growth flatlining since 2019, a significant earnings miss in 2022 and the recent regional banking crisis.[1]

Some analysts have labeled Temenos a value play, calling the reduced share price an “unwarranted” sell-off while highlighting improving operating performance.[2]

Further, several private equity companies have been eyeing Temenos as a potential takeover target over the last couple of years, according to Bloomberg. As of December 2023, a deal is now said to be off the table, according to Swiss local media, but sustained buyout talk has supported investor interest in the stock.

Fundamentals: Temenos Trades At A Rich Premium Relative To Peers Based On Consensus Estimates

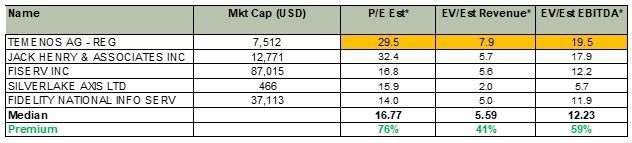

Temenos is the only company in its listed peer group with both negative revenue and EPS growth in 2022, with declines of 2% and 34% respectively.[3] After growth headwinds, Temenos will report 5% revenue growth in 2023, according to preliminary results.

Despite this, Temenos trades at a significant premium to those same peers on consensus estimates for the year ahead: a 76% premium on an earnings basis, a 59% premium on an EV/EBITDA basis, and a 41% premium on an EV/revenue basis.

Its listed peer group comprises the “big 3” core banking technology firms in the United States – Jack Henry, Fiserv, and FIS, as well as Silverlake Axis, a core banking solutions provider to many of the largest banks in Southeast Asia.

Temenos commands this valuation premium even though the “big 3” dominate the US core banking solutions market, the key pillar of Temenos’ future growth: Together, Jack Henry, Fiserv and FIS make up almost 74% of the core banking solutions market share in the US, per S&P Global market intelligence.

In 2022, Temenos’ free cash flow (FCF) declined 46%, “largely due to the EBIT decline and subscription transition as well as higher cash costs”, per Temenos’ press release during the year. It currently trades at a price/FCF multiple of 31x, even factoring the cash flow increase of 26% in 2023, per preliminary numbers.[4]

Temenos net debt stood at $722 million at the end of Q3 2023 and disclosed its leverage ratio (i.e. net debt to EBITDA) stood at 1.8x. [Pg. 18] [5]

Top Temenos Executives Have Cashed Out Over $1.1 Billion Over The Last Decade

While Temenos’ shareholders include many renowned institutional managers such as Baillie Gifford, Fundsmith and Fidelity, Temenos executives have consistently sold stock, cashing out $1.1 billion over the last decade, per Bloomberg. By contrast, Temenos executives have bought only $26 million of stock over the same period.

Part I: Hallmarks Of Heavily Manipulated Earnings—Fake Deals, Rampant Pulling Forward Of Renewals, Backdating Of Contracts And Excessive R&D Capitalization

Former Regional Leader: “Whenever A Partner Announces, Or Temenos Announce That A Partner Bought A License, All Of That is Fake, In My Opinion. It’s Borderline Accounting Fraud, In My Opinion.”

Former Senior Executive: “They Really Are The Masters Of Kind Of Manipulating The Analysts, The Market, The Press, And They Do A Lot Of These, Well I Call Them Shady Deals”

In our interviews with 25 former Temenos employees, we were told that the company regularly manipulated earnings by entering into fake deals, pulling forward contract renewals and backdating contracts, with one former executive telling us that Temenos’ leadership was acutely focused on earnings and willing to “drive the stock price” in questionable ways, adding:

“…they’re very aggressive, and quite prepared to do sort of anything just to really focus on the EPS. And the problem was that the EPS was their focus…”

The mechanics of some manipulations relate to Temenos’ unique revenue recognition policies around licensing that it divides into 3 segments of (i) term/perpetual (ii) subscription and (iii) SAAS.[6] Licensing sales make up over 44% of Temenos’ yearly revenue, per its preliminary 2023 results.

Other manipulations involve the use of partnerships to concoct revenue with almost zero substance. A former regional leader from Temenos said that fake partner deals were common practice:

“… they’re quite common. You just have to read the news. Whenever a partner announces, or Temenos announce that a partner bought a license, all of that is fake, in my opinion. It’s borderline accounting fraud, in my opinion.”

One former senior executive from Temenos told us that Temenos’ volatile share price is due to CEO Andreas Andreades being a “master” at leaking information and manipulating analysts:

“That’s why the stock, one of the reasons the stock is so volatile, is because Andreas is a master of leaking, you know, having his CFO leak this information to the press, ok, so that’ll bump the stock. He’ll do a big trade, and then it levels out or, you know, decreases. And so, they really are the masters of kind of manipulating the analysts, the market, the press, and they do a lot of these, well I call them shady deals…”

In October 2021, Temenos Announced A Strategic Partnership With Fintech Mbanq To “Accelerate BaaS [Banking-As-A-Service] Adoption Across The US”

A Former Temenos Executive Told Us Mbanq Purchased $20 Million In Software And Services From Temenos As Part Of The Deal, But That Temenos Funded The Purchase Of Its Own Software Through An Undisclosed “Investment” Into Mbanq

Former Temenos Executive: “The Convertible Note Was Signed The Same Day, The Same Hour As The Deal Was Signed For Mbanq”

The Executive Told Us, “If That Was In The US And That Was With The SEC, Everyone Would Be Out”

In October 2021, Temenos announced a partnership with Mbanq, which it said was “one of the world’s fastest growing FinTechs,” whereby the two companies would work together to deliver accelerated BaaS (Banking-as-a-Service) adoption across the US, specifically for US-based credit unions.

According to a former Temenos executive familiar with the deal, it was agreed to months earlier in June, but not announced at the time.[7] Mbanq committed to ~$20 million in software licenses and maintenance contracts from Temenos, with the stated aim of reselling the software to its US clients.

“In June of 2021, stretching for making the quarter target … they struck a deal where Mbanq bought $10 million worth of license[s] from Temenos … and with the commitment of 5 years of maintenance, so you basically got a $20 million dollar commitment from Mbanq, and for that, they can use the Temenos software for their growing customer base…”

Temenos’ press release didn’t mention anything about an investment into Mbanq, but the former Temenos executive said that, concurrent with the partnership announcement, Temenos invested in Mbanq through a convertible note, effectively funding the purchase of its own software.

“The convertible note was signed the same day, the same hour as the deal was signed for Mbanq … because they [Mbanq] couldn’t have signed it if they didn’t have the money.”

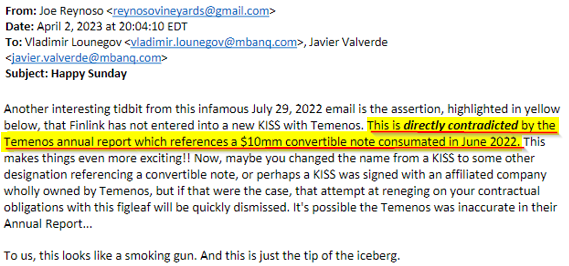

The former executive’s comments are supported by a footnote in Temenos’ 2021 semi-annual report, where it disclosed the purchase of a $19.9 million convertible note, without naming the party, in June 2021. [Pg. 186]

“In June 2021, the Group entered into an agreement to purchase a convertible note for USD 19.9 million, with an option to convert into equity subject to certain conditions.”

A separate former Temenos executive confirmed the circular nature of the Mbanq deal, calling it just one of many of Temenos’ “games” to boost quarterly earnings.

“Temenos will play games. For example, Mbanq … they’ll say, ok [Mbanq], if you sign a $10 million contract with Temenos so we can recognize in our quarterly earnings, we’ll give you $15 million to invest in your company, right. So, they do a lot of these artificial, just on the edge of, what could potentially be, yeah, just on the edge of the line…”

Temenos disclosed that it purchased two “additional” convertible notes for $10 million and $12.8 million, in June and September 2022, putting its total investment at $42.7m.[8] [Pg. 218]

When we asked the former senior executive about these additional investments, we were told that they were made to smooth things over with Mbanq, which was allegedly so frustrated with Temenos’ inaction on the initial partnership that it threatened to sue:

“With Mbanq, again, they [Temenos] sold that, and then they did nothing with it. And then Mbanq threatened to sue them, and then they [Temenos] came back and threw more money at them…”

While both former Temenos executives said that Temenos purchased the convertible notes from Mbanq, Temenos doesn’t actually name Mbanq in its filings.

However, litigation between the founders of Mbanq (formerly Finlink) corroborate that Temenos purchased at least two convertible notes from Mbanq, referencing a first “2021 Temenos KISS” and a second KISS from Temenos in June 2022. [Pg. 23-24]

In October 2022, over a year after it announced the partnership with Mbanq, Temenos for the first time disclosed an investment in Mbanq, per its Q3 company presentation. It chose not to specify the amount, the terms or even when it had invested.

In short, evidence suggests Temenos had obfuscated its funding of and license sale to Mbanq in a revenue roundtripping scheme. A former executive we spoke to was unequivocal in their assessment of the Mbanq dealings:

“If that was in the US and that was with the SEC, everyone would be out.”

A Former Temenos Executive Called The Deal A “Misrepresentation To The Market Of The Reality Of Where The Revenue Was” And Said “I Would Question Whether It Really Was A[n] Above The Board Transaction or Not”

A Second Former Temenos Executive Confirmed That Mbanq Still Isn’t Live With Temenos Software 2 Years After The Deal Was Announced

In December 2022, over a year after the initial partnership announcement with Mbanq, Temenos announced an expanded agreement and mentioned a “minority investment” in Mbanq. The former executive we spoke with said that this announcement misleadingly implied that the investment occurred around the time of the announcement:

“… I think that then they got a lot of pressure on this relationship… so last year around a bit in the fall, there was some type of press release saying, we’re now announcing that we’re investing in Mbanq. It wasn’t then. They invested in them in June 2021.”

“I think it was a misrepresentation to the market of the reality of where the revenue was… I would question whether it really was a[n] above the board transaction or not. And if you put this up for debate with a panel of software experts, I think that they would say that this is appalling. And I don’t know whether it’s in breach of any regulatory or legal business practice. They obviously looked into it and thought it’s okay, but in the US I don’t think that that would fly.”

Today, Mbanq is listed as a “Success Story” on Temenos’ website and was included as a core element of the North America strategy in Temenos’ 2022 annual report and 2023 capital markets day presentation.

A different former Temenos executive told us they were unaware of Mbanq ever going live with the software.

“… two years, coming up two years in. Two years in a month or two. They [Mbanq] still are not live with the software… I never saw any effort to get to know the software, or any drive or any urgency to deploy it, which makes you question what is happening.”

In February 2021, Temenos Announced A Partnership With DXC Technology, Involving Around $8-10 Million Of License Sales From Temenos, Per Former Executives

A Former DXC Executive Told Us The Deal Was Actually Signed On The Last Day of 2020 And Was “Rushed Through” “To Help Temenos Make Their Yearly Number”

In Absence Of A Deal, We Believe Temenos Would Have Missed The Lowest Revenue Estimate For The Quarter

On February 17, 2021, just one day prior to its annual Capital Markets Day, Temenos announced a “strategic agreement” with DXC Technology, a Virginia-based banking software company whose products are used by many top US banks, including Wells Fargo.

The partnership would allow DXC to offer Temenos’ software to its US customer base, a significant milestone for Temenos’ “partner-first strategy” in North America.

As part of the deal, Temenos sold $8-10 million worth of licenses to DXC, per a former DXC executive. A former Temenos executive also told us:

“He [a Temenos Executive] got them to sign up to buy [approximately] $10 million worth of licenses. DXC thought they were reselling those to customers when in fact the contract was structured for DXC to use and consume them internally”.

A former DXC executive told us that despite the announcement in February 2021, the deal was signed earlier, on December 31st, 2020, and was simply a ruse to boost Temenos’ yearly earnings in 2020.

“This was December 31st, we signed this contract, obviously we did that to help Temenos make their yearly number, it was rushed through… They talked a good game about it, but when January 1st hit, there was very little movement on that.”

Ostensibly thanks to this deal, Temenos met its estimates that quarter.

Without this deal, we believe Temenos would have reported results well below market estimates for Q4 2020, a major “earnings miss”. The range of revenue estimates by sell side analysts for the quarter was $273-$286 million, per Bloomberg.

Assuming $8 million was booked in Q4 2020, this would have meant that revenue for the quarter would have been ~$269 million, below even the lowest sell side estimate of $273 million.

In February 2021, Temenos’ CEO Called The DXC Deal “Game-Changing”. Temenos Said It Would “Accelerate Our Penetration” With Large Banks In North America

In November 2021 and Again In June 2022, Temenos Re-Assured Investors On Earnings Calls That Its DXC Partnership Was Progressing Well

Reality Check: A Former DXC Executive Told Us The Entire Deal Was Terminated In Early 2021, Resulting In An Estimated $8 Million Write-Off For DXC

“They [Temenos] Left Us At The Altar … We Gave Them A Bunch Of Money And Then They Literally Walked Away” – Former DXC Executive

On February 18, 2021, one day after announcing the DXC deal, Temenos’ CEO described the relationship with DXC as “game-changing” at its Capital Markets Day. [24:40] [9] Responding to questions on the same day, the CFO added “I think this opportunity could be huge”. [19:05] [10]

In November 2021, Temenos’ then-CEO provided an update on the partnership, saying it was going well:

“Then secondly, on the partnership with DXC, which continues to progress well. We are engaging with a number of DXC’s customers on core banking replacement, and this is supporting the acceleration of our Tier 1 and Tier 2 pipeline in the US, as I mentioned before.” [Pg. 3]

In June 2022, Temenos doubled down on its assurances around the DXC partnership, claiming deals were on the way:

“We continue discussion with DXC and it has not changed. We are engaged in quite a few discussions…but I do want to see, a deal with DXC in the year. There are a few that are on the way. So I’m hopeful we’ll get there.”

Stock market analysts have regularly asked Temenos for more detail on the DXC relationship, clearly trying to assess whether the company has an opportunity to win mega deals from Tier 1 banks in the US to fulfil its mid-term targets for the US region.[11]

We interviewed a former DXC executive to determine how the partnership was going. They confirmed that DXC cancelled the partnership roughly 1-1.5 years after signing due to a lack of effort on Temenos’ part to make the deal successful:

“They got their $8 million or $10 million or whatever it was, and they ran away. And [DXC] actually cancelled the contract about a year later, a year and a half maybe… This isn’t a partnership. You used us for a license sale. You got to make your quarterly number or your yearly number off us, but then you did nothing to propagate or help us move in that direction…”

“I always use the phrase they left us at the altar, right? We were going to get married together. We were going to go to the market. We gave them a bunch of money and then they literally walked away… When I left, I left in [redacted], we had not sold a single license… it was a write-off.”

A former Temenos executive described the deal as having “no strategic thought” that was just about “selling and quick hits”:

“Of course, there’s no follow through. Nobody owns that DXC relationship. Nobody created the strategy or an execution, a joint execution [to] go to market… [DXC] had to write that off [their] books. Because, you know, this is just typical Temenos, oh we got a deal, that money hit the bank, and there’s no strategic thought of, where could we push this now, right? If we just created a team, we sold with DXC… There’s no long-term thinking around how do we turn something into a strategy. It’s just about selling and quick hits.”

In short, Temenos appears to have done very little to develop the relationship with DXC, and then tried to convince investors that it was on solid footing. Temenos has never disclosed any failure of this partnership to date.

4 Former Executives Described Temenos’ “Pulling Forward” Of Contract Renewals To Boost Quarterly Earnings At The Expense Of Future Revenue and Earnings

“If There’s A Renewal That They Can Pull Forward, They’re Going To Go And Be Very Aggressive About Doing That, And That’s What Happened” – Former Temenos Executive

Former Temenos senior executives and frontline salespeople described a practice of “pulling forward” contract renewals with customers, sometimes at significant discounts. Such renewals were often at the expense of long-term deal value in order to recognize upfront revenue.[12]

One former executive noted that this practice was primarily driven by Temenos’ current and former CEOs, Andreas Andreades and Max Chuard:

“Here’s the thing, you know if Andreas and Max had actually made a call-out for a quarter, and they’ve got an earnings call coming up, and they’re missing out on $10 million dollars, they’re going to do everything they can to try and get that $10 million put it up front and if there’s a renewal that they can pull forward, they’re going to go and be very aggressive about doing that, and that’s what happened.”

The executive cited Temenos’ record 2019 revenue, which he said was largely based on pull forwards that disguised how new customer growth was slowing:

“When outside investors were looking at this, they thought ah, the licensing is growing and we’re getting new customers. The reality is the new customer sales were coming down… they basically forward mortgaged the baseline.”

According to the executive, the excessive pull forwards cannibalized future revenues.

“Revenue streams that they should have had in 2022, ‘23, ‘24 had already been spent”, the former executive told us.

The former executive’s comments are partially corroborated by Temenos’ revenue trajectory, which hit a historical high of $971.97 million in 2019, only to flatline in the years after, despite other former Temenos employees confirming that pull forwards are still prevalent at Temenos.

We spoke with a former sales leader from Temenos who spent over a decade at the company. They confirmed that Temenos pressured its sales teams to do early renewals at “too low a value.”

“If you can control it, it can be a very, very good thing to do an early renewal to tie the client closer to the company for a longer period of time. But if you give it away for a very low price, if you are too much under pressure to get to your numbers—we saw that in the Middle East and Africa for some period of time that, in my view, the software, the contracts were renewed for too low a value…”

“The company does not need to recognize it up front, all of it. They could split it up into some buckets and take it later, but the company decided to, for a long period of time at least, to recognize everything immediately.”

Another former salesperson described the focus on underpriced renewals—an incentive that wouldn’t exist if Temenos didn’t recognize significant upfront revenue under its Term and Subscription models.

“I just thought, you know what, I just don’t trust this process… there’s going to be some accounting scandal at some point…”

A former regional executive from Temenos told us that these accounting decisions are controlled at the corporate level:

“The accounting practices are completely controlled at the corporate level. They determine what gets booked and when. The regions don’t really have any say on what those final numbers could or should be. If they want to bring something forward, book early, they will.”

“Don’t Trust Any Of The Public Information”, “…They Would Do Anything To Make The Quarter”: Former Temenos Executives And Sales Leaders Told Us Backdating Contracts To Manipulate Earnings Was Common Practice

“Legal Teams Would Give Power Of Attorney To The Sales Teams To Backdate A Deal That Had Come In, You Know, After The End Of The Quarter” – Former Senior Executive

During our interviews with former Temenos executives, we were told several times that backdating contracts to boost earnings was standard practice at Temenos. One former executive from Europe explained the practice in detail.

“… the standard practice, which was known completely and condoned by Andreas and Max [current and former CEOs], but denied in public, was that the legal teams would give power of attorney to the sales teams to backdate a deal that had come in, you know, after the end of the quarter.”

“I mentioned they would do anything to make the quarter … what would happen, they were sort of playing in a plausible deniability, with the finance and the legal teams… So as soon as power of attorney contracts were given to salespeople in the field, you knew something dodgy was going on.”

A former sales leader from Temenos went as far as to say that we shouldn’t trust any public-facing information from Temenos.

“Don’t trust any of the public information… including the analyst call, okay? Its, again, I’ve never seen any business driven like that… I’ve seen deals closed in January that they were pulled back to the previous quarter, okay? They do that.”

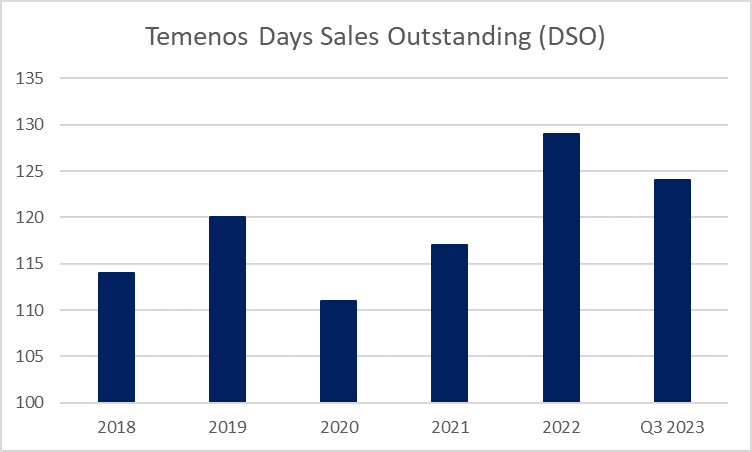

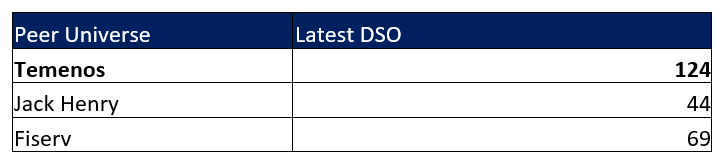

Temenos Has Almost Double The Days Sales Outstanding (DSO) Of Its Closest Peers At 124 Days, Suggesting Difficulty Collecting On Reported Revenue

Temenos’ financial metrics support the claims by former employees.

Days sales outstanding (DSO) is a well tracked financial metric that shows the average number of days it takes for a company’s credit sales to be converted into cash. A persistently high DSO can suggest that a company has aggressive revenue recognition policies.

Temenos has had a persistently high DSO, at 110+ days for the last 5 years.

The DSO count is almost double its peers like Fiserv, which reports DSO in the 60s and almost 3 times Jack Henry which reports DSO in the 40s. [13]

Temenos recently said its DSO may increase further. In the Q3 2023 analyst call, the CFO stated, “we expect DSOs to step up in Q4 with the subscription growth we are forecasting.” [Pg. 6]

Temenos Claims That It Invests 20% Of Its Revenue Back Into R&D, “More Than Twice The Level” Of Its Closest Competitors

Former Executives Told Us The R&D Spend Was “Non-Existent” And A “Mystery”

Former Executives Also Said Temenos Booked Customer Implementation Costs As R&D, Resulting In Inflated Gross Margins And Reported Earnings While Exaggerating Product Investment

“All You’re Doing Is Just Taking Something That Was Custom For A Customer And Saying It’s R&D. It’s Not. That’s The Majority Of It” – Former Temenos Executive

While Temenos claims it has industry leading R&D investment, our conversations with 4 former executives and employees indicate that it instead misclassifies customer implementation expenses as R&D, thereby boosting its reported margins and earnings through more accounting trickery.

Temenos states that it spends 20% of its revenue on R&D, or “more than twice the level” of its closest competitors. In 2022 alone, it invested a total of $279.8 million in R&D, “inclusive of overhead allocations.” [Pg. 46]

Temenos’ principal R&D centers are in India, but its primary Indian subsidiary reported just INR 6.33 billion (~$76 million USD) in total expenses in 2022, according to Indian corporate records, raising the question of where the remainder of Temenos’ annual R&D budget was spent. [Pg. 30][14]

Temenos’ website features a page dedicated to R&D, which offers some clues about what Temenos counts as R&D. Specifically, Temenos suggests that some of its client-facing work is counted as R&D, “as well as” innovations from its R&D centers.

Temenos’ R&D page also states that “all developments are made available to all clients” and its “About Us” page says that “every dollar we invest benefits all our customers.”

Both statements indicate that Temenos may be justifying categorization of customer-specific costs as general R&D.

A former Temenos senior executive claimed that custom development work for one client is not the same thing as R&D, but that these types of customer-specific costs make up the majority of Temenos’ claimed R&D spend:

“You ain’t improving the product. All you’re doing is just taking something that was custom for a customer and saying it’s R&D. It’s not. That’s the majority of it.”

We asked about Temenos’ cloud offering, and any associated R&D expenses:

“That R&D spend, they’re not really putting a whole lot of R&D spend in it. They’re just kind of developing it and putting it out to the customer base, and that’s why people are saying ‘this cloud stuff’s not ready’, ‘cause that R&D spend is non-existent.”

According to another former senior executive, the claimed 20% R&D investment was a mystery even among Temenos’ leadership, who were largely unable to probe Temenos India’s activities and expenses:

“It’s a mystery to many of us who were there as well. I have no idea what they base those [R&D] numbers on, because, you know, it is not reflected in the front office of what the client sees, at all… There’s zero interaction [with] India, Andreas completely puts, I say bubble wraps, right? He puts a bubble wrap around India. Nobody is allowed to interact, engage, criticize, suggest…”

Another former Temenos executive echoed this sentiment, saying “nobody really knew” what the R&D money was being used for:

“I’ve never seen anybody with such a lack of business honesty… Whenever they say, well we have 20% [R&D investment], nobody really knew, understood, right, what the resources were doing. And if anybody good kind of questioned… you’d get in trouble, okay? That was the story… Again, there’s a big black box in there, in India.”

Another executive echoed these comments, saying Temenos develops its products “on the client’s dime” but then capitalizes the cost as R&D instead of expenses. The executive said this go-to market strategy was driven by Temenos’ longtime former Chairman and now CEO, Andreas Andreades.

“… Andreas is all about, ‘sell your way out of everything,’ right? Not innovation, not product development, sell sell sell. Get a customer to pay for it. And then we’ll use that money to go build whatever it is they want.”

One former executive said that Temenos lives in “escalation” mode due to the company failing to invest even basic amounts into its products.

“There were some strategic investments that were needed for the products in the Americas, North America … and it wasn’t a crazy amount at all, but unless you do that, and fix certain things to make it available out of the box to every client, unless we fix it, the next sale is your next escalation… So yes, they overpromise. It’s because the product is not being completely finished…”

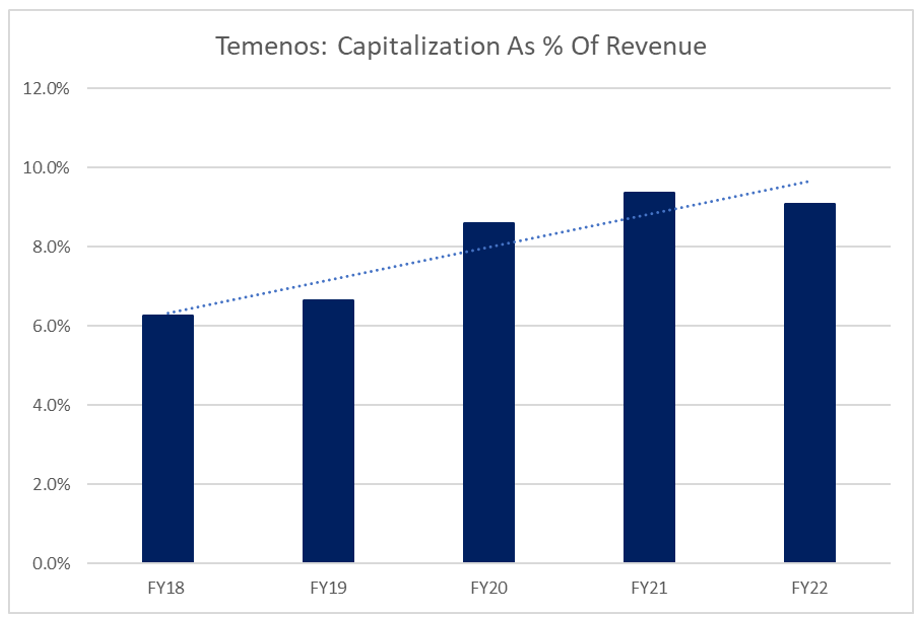

In 2022, Temenos’s R&D Capitalization Rate Was 62% Higher Than Peers, Resulting In $86 Million In Excess Claimed R&D Being Shifted To The Balance Sheet

Compared With The Peer Average, Temenos’ Excessive R&D Capitalization Led To An Estimated 29.5% Boost To Its 2022 Pre-Tax Profits

If Capitalization Was In Line With Peers, 2022 EBIT Margins Would Have Fallen From 17.2% to 13.7% Under IFRS

When companies account for R&D costs, they may “capitalize” costs by recording them as a balance sheet asset and recognizing them over a period of time.

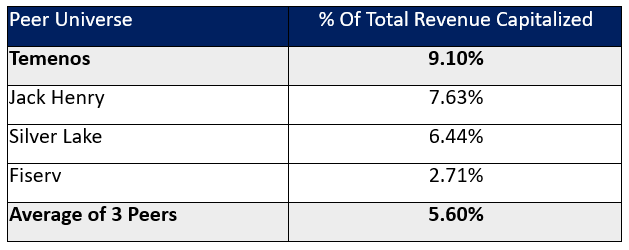

Temenos consistently capitalizes R&D costs to its balance sheet at a rate higher than its peers. In 2020, 2021 and 2022, it capitalized approximately 8.6%, 9.36% and 9.09% of its total revenue, respectively.

On average, Temenos’ capitalization rate for R&D expenditures is ~62% higher than peers.

When compared with the peer average, Temenos’ aggressive capitalization rate led to a $33.1 million or 29.5% estimated boost to pre-tax profits in 2022 alone.[15] It would have also caused reported IFRS EBIT margins to increase from 13.7% to 17.2%.[16]

While this is concerning on its own, we find it especially alarming considering that multiple former Temenos executives expressed doubts about the validity of virtually all of Temenos’ claimed R&D investments, as outlined in the previous section.

In 2023, Temenos Extended Its Allowable Amortization Period For “Internally Generated Software Development Costs” From 5 Years To 7 Years, Allowing It To Recognize Its Questionable R&D Costs Even More Slowly Than Before

If Fully Utilized, This Extended Amortization Period Would Lead To An Estimated 8.7%, One-Off Boost To Reported 2023 Profits

Capitalizing normal operating costs and amortizing those costs too slowly is a textbook mechanism for manipulating financials.

Historically, Temenos’ capitalization policies allow it to amortize certain expenses over a 3-5 year period. However, effective January 1st, 2023, Temenos extended the top end of this amortization window to 7 years, allowing it to spread out its already questionable R&D costs over an even longer time period.

If Temenos utilized this expanded amortization schedule of 7 years, its 2023 profits could have experienced an 8.7% one-off boost without any additional disclosure of the specific impact of the change to shareholders. [17]

Temenos Has Also Boosted Its Reported Free Cash Flow Through “Accrued Expense” Costs That Are 66% Higher Than The Peer Group As A % Of Cost of Sales

Temenos has repeatedly used another financing tactic to boost its reported free cash flow, which we suspect is unsustainable.

Accrued expenses, sometimes called accrued liabilities, are costs that a business incurs that have not been paid. Usually these occur due to terms with suppliers (e.g. supplier credit) or when a company has not received an invoice. Accrued expenses may involve some estimation from management, given that invoices by suppliers are received at a future date and can differ.

In Temenos’ case, these unbilled costs are 66% higher (as % of cost of sales) than its peer group, some of which are many times the size of Temenos and would normally be expected to exert more favorable terms from suppliers.

In 2022, Temenos reported free cash flow of $192.9 million. If accrued expenses were in a similar range to peers, it would mean a $42.5 million reduction in cash flow, or 22% lower than the reported number in 2022. [18]

Part II – Temenos’ North American Strategy, The Cornerstone Of Its Growth Story, Is Littered With Failed Implementations

Temenos Highlights North America As A Key Growth Driver, Projecting It Will Account For 45-50% Of Mid-Term Software Revenue Due To “Superior Technology” And “Leadership Vision”

In Part 1, we detailed how Temenos’ key partnerships with Mbanq and DXC, which were meant to support a North American expansion, appear to have faltered completely or to simply be shams

Despite these failures and misrepresentations, Temenos continues to double down on its North American growth story.

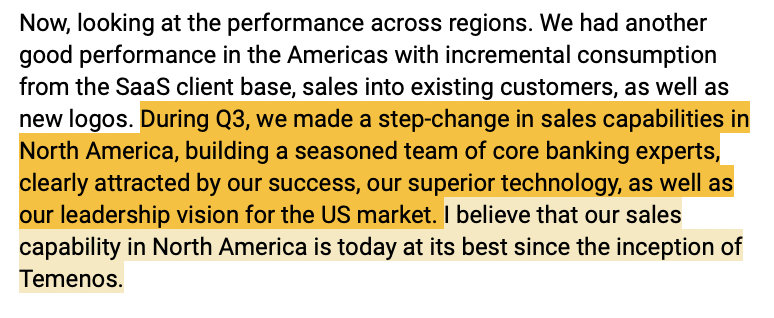

In its 2023 investor day presentation, Temenos highlighted continued momentum in North America, its key strategic market, projecting that North America would account for 45-50% of mid-term licensing revenue.

More recently, in its Q3 2023 earnings call, Temenos highlighted that it had attracted a seasoned core banking team, stepping-up its sales capabilities in North America with “superior technology” and “leadership vision.” [Pg. 5]

Despite Claims Of “Superior Technology” In North America, A Former Senior Temenos Executive Told Us “Clients Were Falling Out The Bottom Of The Funnel … As Fast As We Could Fill It At The Top” Due To “Deficiencies In The Product”

While reflecting on the North American market, a former senior Temenos executive told us that sales was the only thing Temenos excelled at in North America, but that Temenos was losing customers just as fast due to deficiencies in its products:

“It became very apparent to me and I think several other leaders, however, that you know, clients were falling out the bottom of the funnel, so to speak, as fast as we could fill it at the top of the funnel with sales and new logos…”

“… I’ll tell you that over 18 months, there were… 12 senior leaders [in the US], who left Temenos, and all of that was motivated by the fact that it became clear that as we sat in these internal executive committee meetings, it became clear that Andreas was not willing to look at the deficiencies in the product…”

Our research corroborates the former executive’s comments and shows that Temenos’ North American strategy is littered with client lawsuits and failed implementations.

A Former Executive Told Us The CEO Would Often Pitch Non-Existent Products To Prospective Customers

Former Executive: “Andreas Or Max Would Be Going Into A Meeting And They Didn’t Have A Brochure For The Feature That Didn’t Exist … And It Had To Be On Their Desk By The Time They Got To The Client. For A Feature That Hasn’t Been Thought Of, Not Run By Product, Not Run By Anybody Sensible”

Throughout our more than two dozen interviews with former Temenos employees, including senior executives, two recurring themes were (1) a lack of product investment and (2) the overselling of product capabilities.

For example, one former senior leader from Temenos told us that the company was “single-handedly” run by Andreas Andreades, who would often request brochures for new product features that hadn’t yet been developed or even discussed:

“The company is single-handedly run by Andreas and it was Max before that, where basically you sat back and waited for instructions… Andreas or Max would be going into a meeting, and they didn’t have a brochure for the feature that didn’t exist. And they wanted one and it had to be on their desk by the time they got to the client. For a feature that hasn’t been thought of, not run by product, not run by anybody sensible. But they were going in, the sales guy told him that’s what they were talking about and he wanted a brochure…”

The former employee’s comments are supported by our research into several of Temenos’ North American deals.

US-Based Unify Financial Credit Union Signed On With Temenos In September 2018

In December 2021, Unify Sued Temenos For Fraudulent Inducement And Negligent Misrepresentation, Claiming That Temenos Oversold Its Cloud Capabilities And That Its System Was So Unstable That Unify Had To Revert To Its Old System 2 Months After Going Live

In September 2018, Unify Financial, a credit union with over 260,000 members and $4.3 billion in assets, signed on with Temenos for various cloud-banking software applications. [Pg. 4]

According to Unify, it chose Temenos for its cloud-based banking applications, with Temenos’ representing that it “lived in the cloud and that it had customers that lived in the cloud.” [Pg. 3]

After two successive delays, Unify finally went live in mid-November 2020 with its cloud solutions for collections, loan origination and account origination. [Pg. 5]

Unify’s lawsuit outlined multiple issues with the Temenos software:

Unify eventually learned that Temenos didn’t have the cloud experience it claimed to have, per the same complaint:

“When multiple issues did arise, because Temenos had no prior experience, it had no explanation for what caused the problem or a solution to remedy the issue. As a result, Temenos was unable [to] facilitate UNIFY’s successful migration to the cloud.” [Pg. 4]

After being “plagued” with issues, Unify reverted to its legacy system in January 2021, followed by the above-referenced December 2021 lawsuit against Temenos. [Pg. 8]

The suit was withdrawn by Unify in March 2022, indicating that the issue may have been settled out of court.

US-Based First Fidelity Bank Signed On With Temenos In December 2019

In 2022, First Fidelity Sued Temenos For Breach Of Contract And Fraudulent Misrepresentation, Saying it Was “Fed Up With Temenos’ Excuses And Delays”

Effective December 31, 2019, First Fidelity Bank entered into an agreement with Temenos to provide new loan origination platforms for its US banking clients. [Pg. 2]

One of the key requirements of the deal was that the Temenos-built system would integrate with First Fidelity’s payment processing software, which Temenos initially said it could achieve by Q3 2020, before delaying to a “go live” date to an unspecified date in early 2021. [Pg. 4, 6]

“By the time the project plan was agreed upon in October 2020, First Fidelity had paid Temenos $571,803.23 in project and ‘support’ fees… Yet, as of October 2020, Temenos had not completed construction of any processes or software attributable to such ‘support.’” [Pg. 7]

After experiencing additional delays and unexpected costs, First Fidelity cancelled the contract with Temenos in February 2022, requesting an immediate return of $933,040. [Pg. 10]

In May 2022, First Fidelity sued to recover this amount, alleging breach of contract and fraudulent misrepresentation. [Pg. 12, 14] The bank said it had been “fed up with Temenos’ excuses and delays”. [Pg. 8] The dispute was eventually settled via a confidential agreement in October 2022.

US-Based Grasshopper Bank Went Live With Temenos’ Cloud-Based Core Software In 2019, With Temenos Highlighting The Deal As Part Of Its “Proven Track Record In Supporting US Banks Growth”

Grasshopper Executive: Grasshopper Had Numerous Implementation Issues And Abandoned Temenos Just 4 Years After Launch

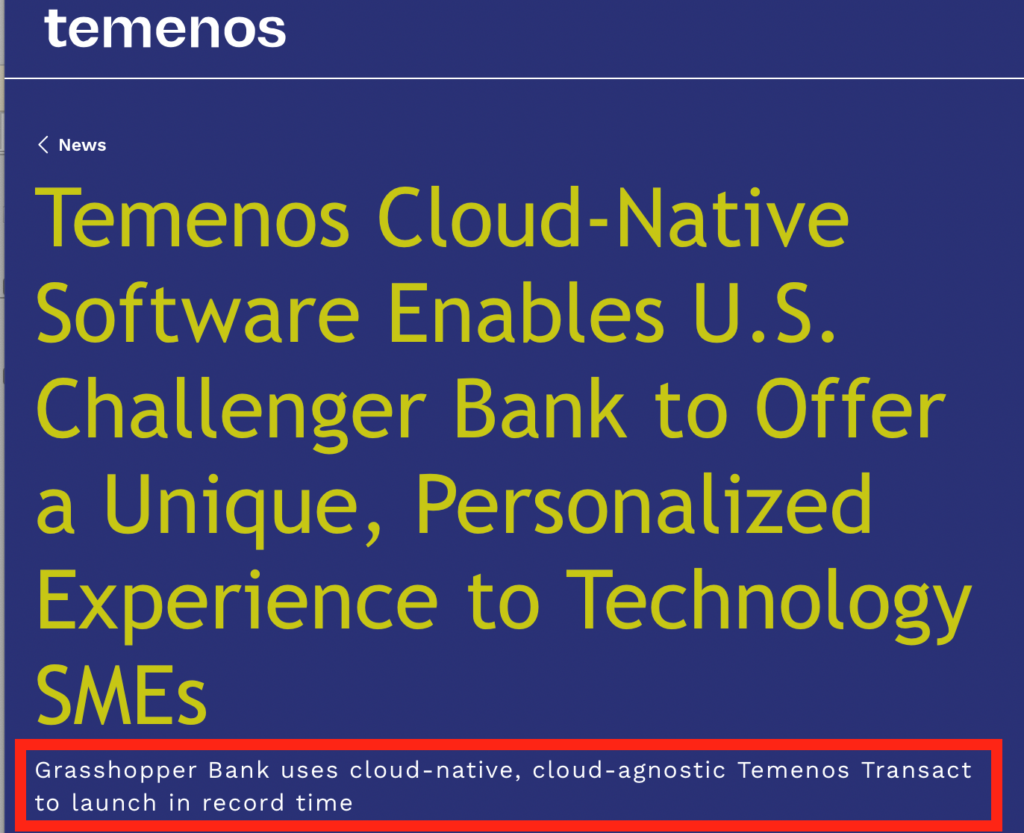

In June 2019, Temenos announced that US-based Grasshopper Bank had gone live with Temenos’ “cloud-native, cloud-agnostic digital banking platform” in what appeared to be a notable win for Temenos’ North American and SaaS focused strategy.

The press release quoted Temenos’ CEO at the time, Max Chuard:

“By running Temenos Transact on Temenos Cloud, Grasshopper will be perfectly positioned to scale as it grows alongside New York’s booming technology ecosystem.”

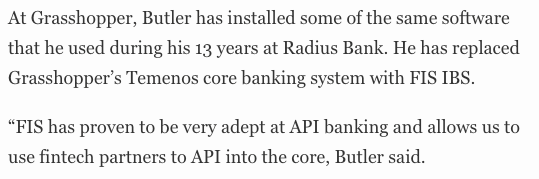

While the deal appeared successful on the outside, a 2022 Forbes article reported that Grasshopper had replaced Temenos entirely, opting instead for a system from competitor FIS:

To better understand why Temenos was abandoned, we contacted a former Grasshopper senior executive who told us Temenos’ implementation strategy was largely to blame:

“When we opened on April 1st, we actually were not ready from a system standpoint, we were six months away largely because of Temenos’ implementation strategy.”

The executive went on to describe Temenos’ failure to understand the US regulatory environment:

“The process of mapping everything was excruciating, and we knew more about the US regulations than they did… we had to constantly be teaching them.”

The executive alluded to a lack of support from Temenos, stating that many issues simply didn’t get resolved in a timely fashion:

“I think at the end of the day, the final nail in the coffin was problem resolution. There would be tickets that would be outstanding for months.”

US-Based Varo Bank Went Live With Temenos Cloud-Based Core Banking In September 2020, And Is Currently Highlighted As A “Success Story” On Temenos’ Website With Varo’s CEO Calling Temenos A “Great Partner”

Former Varo Employee: “I Think It Would Be A Stretch To Call It Successful By Any Means”

Former Varo Executive: “I Don’t Think Anyone Would Pick Temenos If We Went Back In Time. I Mean We Lost Years Of Our Lives To Temenos”

In September 2018, US FinTech company Varo Bank (then known as Varo Money) chose Temenos for cloud-based core banking, and 2 years later, Temenos announced that Varo had “gone live.”

Today, Varo is listed as a success story on Temenos’ website, which features a quote from Varo CEO Colin Walsh saying Temenos has been a “great partner” for Varo.

Varo Bank appeared to have been a notable win for Temenos’ North American cloud-solutions approach, yet a former Temenos executive told us that Varo executives were privately “very frustrated” with Temenos.

When asked about the implementation, the former Varo executive told us:

“I am very close and familiar with that experience, I think forever, forever scarred to be honest… it was incredibly painful.”

The former executive described numerous issues with the Temenos implementation.

“For us, nothing was out of the box, even though everything was sold as out of the box.”

“One of the issues was, we had to wait at least like 5 days to process an ACH transaction when it takes typically 2 to 3 days… that was terribly problematic. They couldn’t do returns properly… we took a bunch of losses against it, and I mean millions of dollars in losses against it… From a card transaction processing, same thing… we would go into, kind of the calls with Visa for the integration and it’s like nothing worked. Literally nothing worked…”

“I can say with great certainty though, that if Varo was able to replay… Temenos would not be our choice… but at this point it’s the devil we know… but I don’t think anyone would pick Temenos if we went back in time. I mean we lost years of our lives to Temenos.”

We also contacted a former Varo employee who said that Temenos “missed the mark” and couldn’t deliver what it promised, calling the implementation a “horrible experience.”

“They just missed the mark. They just, they weren’t able to deliver. And it had some impact to our customers, you know. The cost associated with downtime, [the] platform is, for whatever reason, the transactions aren’t coming through. You know, it’s just, a number of things… it’s just been, I would say, a horrible experience overall…”

The former Varo employee said that Varo is still using Temenos, but that it would be a “stretch” to call the project a success:

“Yeah, we’re still using it, but I think it would be a stretch to call it successful, by any means. I think the biggest challenge has been the fact that Temenos didn’t have any experience with US-based banking financial regulations and the requirements of that. And then the servicing of those requirements were just off the mark. [It] caused a lot of pain in both the installation and ongoing maintenance… I think they’re just inexperienced.”

The former employee said that Varo had an opportunity to extend its contract with Temenos, but chose to reduce its contract length to keep its options open:

“There was an opportunity to extend the contract … I think it might have been 7 or maybe even 10 years was a consideration for the extension, but I think they opted for a shorter horizon to transition off of Temenos, and Varo is working on looking to do that eventually.”

Based on former employee comments, Varo Bank serves as another example of Temenos over-promising and under-delivering, especially when it comes to its cloud-based offering, the linchpin of its growth story.

While Unify Financial, First Fidelity, Grasshopper Bank, and Varo Bank serve as examples of Temenos struggles with its core offering in its key strategic North American market, our research also found its digital front-end product has been a failure across regions.

Part III – Temenos Infinity: A Failed $840 Million Roll-Up Of Digital Banking Products

In 2019, Temenos Formally Announced “Temenos Infinity,” An Attempt To Diversify Beyond Core Banking Software By Rolling $840+ Million Of Acquisitions Into A Suite Of Digital Banking Products

Temenos has been selling core banking software since the 1990s. While it has recently attempted to shift this offering from on-premises installations to the cloud, core banking remains the company’s bread and butter.[19]

However, in January 2019, Temenos announced the launch of Temenos Infinity – an attempt to diversify away from the “Transact” core banking product with a series of “Digital Front End” products.

A former Temenos executive explained the Infinity strategy to us:

“The whole thought was, okay, Transact is the back office, right? It is the core of nervous center of a bank. It’s deposits. It’s loan origination. It’s payment processing. So, it’s all of that very complex, technical back-end…

So, the holy grail for all of these companies… is what if we could take the power of all of that data on the back-end in the core and use it to instruct the digital front-end experience to create this highly customized, high-touch, very personalized experience for the end user?”

Temenos’ pursuit of this “holy grail” was fueled by a series of acquisitions to expand and strengthen the Infinity product line.

- Acquisition #1 – In 2015, Temenos acquired Akcelerant for ~$53.8 million, which would later be rebranded as part of Temenos’ Infinity offering.

- Acquisition #2 – In 2018, Temenos acquired Avoka for $254 million, which it said would be “integrated with the Temenos Infinity product.”

- Acquisition #3 – In 2019, Temenos acquired Kony for $532.7 million, saying it would “further strengthen the Temenos Infinity product.”

Altogether, Temenos spent at least ~$840 million on acquisitions to diversify beyond core banking and build Temenos Infinity, which was touted as a success in Temenos’ 2021 Capital Markets Day presentation, claiming 650 customers for the new division.

Two years later, by Temenos’ 2023 Capital Markets Day presentation, it displayed a breakdown of its SAM, or Serviceable Addressable Market, with Infinity representing the single largest category.

Despite Temenos’ posturing on the success and multi-billion-dollar potential of Infinity, commentary on the new division has been notably sparse from recent investor presentations. The term “Infinity” showed up 23 times on Temenos’ 2020 Capital Markets Day presentation, but just 5 times on its 2023 Capital Markets Day presentation.

Former Temenos Executives, Partners, And Customers Confirmed Dozens Of Failed Infinity Implementations. One Former Temenos Executive Called The Entire Division A “Huge Destruction In Value”

Another Former Executive Said, “Let’s See, In 2021, We Had 19 Clients In North America… That Were Supposed To Go Live [On Infinity], And 2 Of Those 19 Went Live… Tons Of Client Cancellations, Frustrated, Angry Clients”

According To A Former Senior Executive, Temenos CEO Andreades Admitted In A Closed Door Meeting That Infinity Had Failed, “He [Andreades] Literally Said… We’ve Gotten Nowhere With Infinity In 3 Years, We Need To Just, You Know, Toss It Overboard [And] Be Done With It”

Our interviews with dozens of former Temenos executives, implementation partners, and customers paint a picture of an expensive roll-up of digital banking products that Temenos has simply failed to bring to market successfully.

When we asked a former Temenos executive about Infinity, we were told it had been abandoned:

“It always amuses me that nobody really goes back, and the analysts don’t hold Temenos accountable because there was so much talk about Infinity… they just simply couldn’t do it. The last meeting that I sat in with Andreas, he literally said…we’ve gotten nowhere with Infinity in 3 years, we need to just, you know, toss it overboard [and] be done with it.”

“So, for the past 18 months almost 24 months, if anybody went back, they would see, there’s very little talk, you don’t ever hear them talk about Infinity… all that, they’ve kind of just abandoned it.”

Another former Temenos executive told us that Temenos’ Infinity products, specifically those acquired from Kony, simply don’t work in the cloud alongside Temenos’ core software:

“They bought Kony to help get the customer base, and they just made a hash of that. So, in terms of the US market, I think they couldn’t have done it worse … it wasn’t accretive in any way, it didn’t buy the market share, it didn’t buy them a customer base, it didn’t buy them anything. It bought them a significant headache, which they still haven’t sorted out.”

“So, for instance, their front-end and back-end don’t run in the cloud together at all and won’t for the foreseeable future, and they have wasted more money in the US”

The same executive said that Infinity, specifically the Kony product suite, didn’t receive investment from Temenos after the acquisition:

“It hasn’t really received the investments since the acquisition, so, it was a great hope and they had a whole Infinity team of 20 or 30 salespeople, and that got canned… The writing was on the wall for it, and I think a huge destruction of value in terms of what they paid for it…”

One former employee told us Temenos “axed pretty much everybody in Infinity” over the last year, while another said, “the top talent that supported that product [Infinity] left.”

We asked several former executives why Infinity was struggling, and one individual with familiarity of the North American market said they were unable to implement the technology on most the deals that were sold:

“Let’s see, in 2021, we had 19 clients in North America… that were supposed to go live [on Infinity], and 2 of those 19 went live. They could not, we could not get Infinity implemented and working properly, so they’ve basically just kind of abandoned it. You know, tons of client cancellations, frustrated, angry clients…”

We also spoke with a former manager from NDC Tech (now Systems Limited), one of Temenos’ implementation partners in the Middle East & Africa, who told us that Temenos’s Infinity strategy largely failed in the region due to implementation challenges:

“Temenos acquired it [Kony], and then it spoiled it. Sorry to say that. Okay, so what happened is that NDC started selling it in the MENA [Middle East and North Africa] region … so around 20+ banks in 3 years onboarded with Infinity… but honestly, out of those 20+ banks, only 2 or 3 banks were able to go live.”

In 2022, Pakistan’s largest bank, Habib Bank, was included as a “success story” on the Temenos’ website for the core banking platform.[20] We were told by former Temenos executives and implementation partners that Habib Bank cancelled its Infinity project. Per a former manager at Temenos:

“Habib Bank cancelled Infinity because of the effort that it would have taken for us to deliver their requirements on top of Infinity. The CIO [Chief Information Officer] just decided that for that amount of mandates, he can just extend on their current solution and it’ll just cost them less,”

We have found no disclosure from Temenos about Habib’s Infinity project being cancelled.

We Found Other Failed Or Stalled Infinity Projects Including A Leading Cambodian Bank, Pakistan’s Largest Microfinance Bank And A Listed Australian Bank

During our conversations with Temenos clients they described more examples of failed Infinity deals, including 3 below:

#1 Failed Infinity Deal: Hattha Bank

Hattha Bank describes itself as a one of the leading banks in Cambodia. In 2021, Temenos announced a deal to implement Infinity for Hattha Bank and boasted it would “enable the bank to quickly launch” its products to small businesses. An executive at the bank told us despite only wanting a basic internet banking solution, Infinity was littered with bugs and a poor user interface:

“Delay…again and again. Very frustrated. And they [Temenos Infinity] have many bugs.

“The UI, the user experience, and the user interface is, is very poor, actually”.

“We decided to terminate with them, I think, in October 2022.”

#2: Failed Infinity Deal: Khushhali Microfinance Bank

Khushhali Microfinance Bank is Pakistan’s largest microfinance bank with over 195 branches, serving over 5 million customers since its founding in 2000. [1, 2] Khushhali was already a core banking (Transact) customer and then signed a deal for Temenos Infinity in October 2021, according to an update from Temenos’ implementation partner and Temenos’ Twitter handle.[21]

“Halfway through the implementation, we realized that the microservices is not compatible with the earlier versions of Transact [Temenos Core banking software], and it won’t work”, a former Temenos employee told us.”[22]

Two years later, the bank is still not live with Infinity:

“The project is on hold, you know. So the project is on hold. We don’t want to come to the market with a compromised solution,” an executive at Khushhali told us.

#3: Failed Infinity Deal: MyState Bank

MyState Bank is a challenger bank headquartered in Tasmania with over 150,000 customers. In November 2021, as part of its strategy to expand into the Australian market, it selected Temenos “Infinity”, upgrading from an old Temenos platform, per a Temenos’ announcement.

A current employee with the bank aware of the Infinity transformation project told us:

“Their UX [user experience] and core logic needed a lot of customization as their ‘Out of the box’ product is built for American clients and it wouldn’t work directly for Oceanic clients.”

“The contract was signed for the work to start last year and 3 months into it we’ve ditched their product,” they told us.

While investors were sold on Infinity being an exciting new platform with the promise of making Temenos a leader in digital banking software, the actual execution seems to have fallen apart.

To date, Temenos has not disclosed any failed Infinity launches or impairments of the $840 million of acquired assets that live under the Infinity umbrella. Instead, Temenos seems to hope that Infinity – perhaps the largest destruction of shareholder value in the company’s history – will simply fade from shareholders’ minds.

Part IV – Many Of Temenos’ Most Highlighted Deals In Europe And Australia Have Been Plagued With Delays, Cost Overruns, And Regulatory Issues

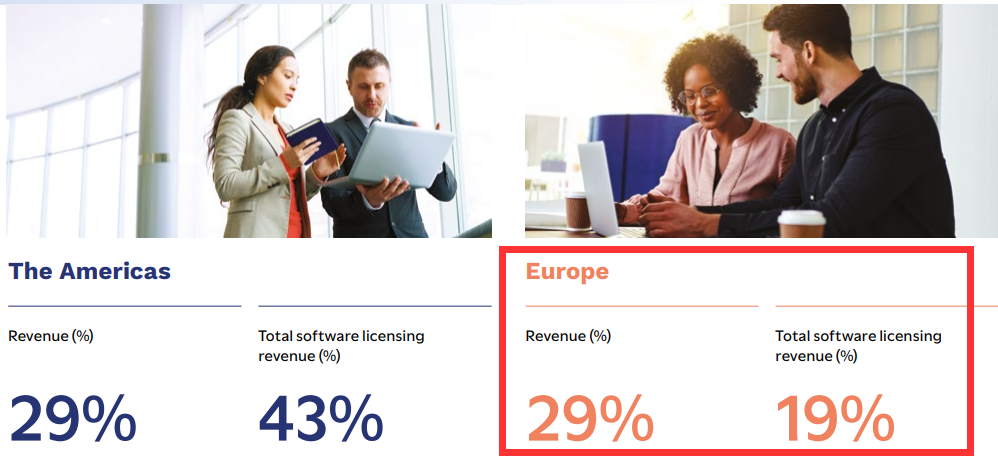

Europe has been a key growth driver and a core market for Temenos, currently accounting for 29% of total revenue, per Temenos’s 2022 annual report. [Pg. 6] Europe is where Temenos has historically won its largest deals, including Nordea and Bank of Ireland.

Australia is a smaller but still significant region for Temenos, accounting for 3.2% of total revenue in 2022, per its annual report. [Pg. 227]

Some of Temenos’ key deals in the region include Volt, Judo Bank and BNK.

Yet many of the highlighted deals in Europe and Australia, which together account for nearly a third of Temenos’ revenue, have been plagued with delays, cost overruns, regulatory issues, and outright failures.

In 2015, Nordea Signed On For A 5-Year On-Premises Core Banking Transformation With Temenos, Representing The Largest Deal In Temenos’ History

Today, The Deal Is Touted As A Success Story By Temenos

Reality: Nordea Reportedly Experienced Cost Overruns, Delays, And According To A Former Temenos Executive Who Called The Implementation “Absolutely Terrible,” Still Hasn’t Gone Live Across All Modules And Regions

In 2015, Temenos won an on-premises core banking transformation project with Nordea, one of the largest banks in the Nordic region with 9.3 million private customers, whereby Temenos software would handle loans, deposits, and transaction accounts.

As reported by Forbes at the time, the deal represented the “biggest deal Temenos has ever had”, and would take four to five years to complete:

In 2019, FinTech Futures reported that costs for the Temenos-led project seemed to be running much higher than anticipated:

“Since 2015, with the help of its main supplier Temenos which won its largest ever deal with the bank, the firm is in the process of updating its old legacy systems from the likes of Finastra and Tieto. Initially, Nordea said it would invest just over €1 billion in its technology overhaul, but it seems the costs are climbing much higher.”

According to the article, the cost overruns led Nordea to “introduce a new business plan” that included a €735 million impairment to IT charges, although it was unclear how much of the impairments were related to Nordea’s investments in Temenos software.

In May 2021, nearly 6 years after Nordea kicked off its “four to five” year transformation, its Chief Banking Officer resigned amidst industry reports that the bank’s core transformation project had slowed.

Today, Nordea is touted as a success story on Temenos’ website. A former senior executive from Temenos Europe told us that the implementation still hasn’t been completed:

“They [Nordea] were supposed to be live about 2 years ago on all product lines, and now they’re like live in one geography with like one product line, and they got there in the end on one of these things, but the journey to get there has been absolutely terrible.”

The former executives’ comments are supported by Temenos’ own disclosures from its Capital Markets Day presentation which state that as of February 2023, nearly 8 years after the Nordea deal was announced, it has only gone live with one module (deposits) in two out of its four regions. [Pg. 71]

In 2016, Bank of Ireland Selected Temenos Core Banking To Be “At The Heart” Of Its €500 Million Technological Transformation

The Project Budget Reportedly Tripled Over 5 Years, Led To Wide-Ranging IT Failures, A $139 Million Impairment For The Bank And Shook Public Confidence In The Irish Banking System

“I Mean, It Cost A Billion Euro To Make The Transition, And Even Then, It Didn’t Work” – Former Temenos Executive

In 2016, Bank of Ireland selected Temenos for a core banking transformation which Temenos’ then-CEO claimed “further demonstrates that Temenos is the established technology partner for the digitization of the financial services industry.”

The CEO of Bank of Ireland stated that Temenos had a “proven track record globally in delivering best-practice core banking systems.”

Despite the favorable outlook, the project has since been plagued with cost overruns, delays, business disruptions, and other operational challenges.

For example, the project was reportedly slated to cost €500 million, but by 2019, industry publications reported that the costs had risen to €900 million, and could go as high as €2 billion.

At the end of 2020, Bank of Ireland took a €139 million impairment on its software assets, citing the immature capabilities of its “transformation investment asset product set.” [Pg. 281]

As recently as August 2023, Bank of Ireland has experienced service disruptions and wide ranging IT failures, according to local publications.

On August 17, 2023, the Irish Times reported that Bank of Ireland’s “glitches” had shaken confidence in the Irish banking system. In one highly publicized example, a technology glitch in Bank of Ireland’s software led to free cash being available for customers, per the New York Times.

While we couldn’t confirm which of the bank’s many high profile technology issues were directly related to Temenos’ software, a former technology head at the Bank of Ireland told us that Temenos over-promised and under-delivered with respect to its core software, then known as T24, saying that it simply “couldn’t handle” the bank’s needs:

“When you started to get into trying to actually make that work right, so you know, multiple application servers at the T24 level… T24 couldn’t handle it.”

“They [Temenos] oscillated between just trying to sell more software, and, you know, tell us that, oh yeah, this has been done somewhere else before. And then when you poked at it a little bit, it was, it wasn’t quite what they had said.”

We also spoke with a former Temenos product director with knowledge of the deal, who said that the technology simply didn’t work:

“So, Bank of Ireland is, it’s kind of known in the industry. It’s quoted by, you know, by competitors, by banks and so on… I mean, it cost a billion euro to make the transition, and even then, it didn’t work.”

In 2019, 3 Nordic Banks Chose Temenos For Cloud-Based Core Banking, Only To Abandon The Project Less Than 2 Years Later, According To Industry Reporting

A Former Temenos Sales Leader Said The Deal Was “Basically Terminated” Because Temenos’s Implementation Partner “Didn’t Understand The Way Of Banking In The Nordics”

In April 2019, Temenos announced a new core banking deal with three Finnish banks – Savings Banks Group, Oma Savings Bank, and POP Bank Group.

According to Temenos, the “cloud-native” banking platform would yield “exceptional operational efficiencies” and “dramatically reduced cost of deployment,” representing what Temenos’ then-CEO called a “strategically important” deal for the region:

“This is a strategically important signing for Temenos as it highlights our continued momentum in the Nordics market, where we support flagship banks such as Nordea with their core transformation projects.”