Summary: Riot Blockchain, Inc. (RIOT)

- Riot reported yet another dubious transaction via 8-K during a market “dead zone” – Friday after the close.

- Riot is paying a $4 million upfront consulting fee to a believed undisclosed related party entity.

- Just last week we had identified the entity, Ingenium International LLC, as being highly suspicious.

- Collectively, Riot’s series of suspicious transactions are among the most brazen irregularities we have seen in a U.S. listed company.

Introduction

We genuinely thought we were done writing about Riot Blockchain (NASDAQ:RIOT) after our first article in early December. After all, what more needed to be said?

- We had called the company out for making an arguably absurd “pivot” from a medical device company to a blockchain company.

- We had identified that the company overpaid by about 6x for equipment purchased through a highly suspicious, newly-formed entity.

- We had identified that a special dividend seemed to disproportionately enrich insiders.

- We had identified that Barry Honig, an individual with a controversial past, seemingly had an influential behind-the-scenes stake in the company.

That should have been enough.

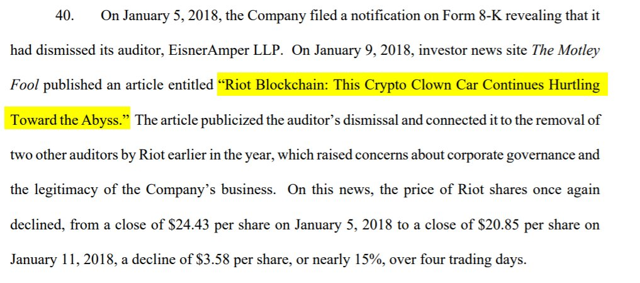

It also should have been enough when we wrote our second article on January 9th, entitled “Riot Blockchain: This Crypto Clown Car Continues Hurtling Toward The Abyss.”

After all, what else could there be?

We had reinforced our earlier research by identifying numerous issues with:

- Believed related party transactions

- Multiple auditor switches

- The company’s pattern of reporting seemingly negative news on Fridays after the market close.

Subsequent to that second article, the Wall Street Journal, the Denver Post, and CNBC corroborated and expounded on our research with exposes of their own. The stock plummeted, particularly after the CNBC piece.

Our second article even made a cameo appearance in one of Riot’s growing list of class action lawsuits (1, 2, 3)

Our rather absurd headline is now forever cemented in the records of Florida’s Southern District.

Great! Now we were done. Totally…

But then, despite all the scrutiny by us, by media outlets, by other independent bloggers and by numerous financial professionals (except for Dennis Gartman)… despite all of it, something remarkable happened.

On Friday, February 16th, after the market close, the company reported yet another 8-K detailing what we believed to be its most brazen transaction yet: The company overpaid by an estimated $18.5 million for equipment purchased from a believed undisclosed related party entity.

We have so many other things to do. There are all manner of companies we are researching that engage in questionable business practices, “creative” accounting, or other believed improprieties. We have several reports coming out in the next couple weeks that we think will be brand-new and highly impactful.

But we just couldn’t help ourselves. The transaction struck us as just too brazen. So we wrote a third article, titled “Riot Blockchain’s Brazen Disclosure Issues Continue.”

Finally! After showing what we believed to be clear, new related-party transactions… we were done?

It’s Not Over

Just prior to leaving the office on Friday we had a cynical thought:

“Gee, what wackiness might Riot report after the close today?”

We were half joking, but we went ahead and checked EDGAR anyway. Sure enough, another 8-K popped up from Riot Blockchain, having been filed yet again on a Friday after the market close.

A Consulting Agreement Unlike Any We Have Ever Seen Before

The new Friday, February 23rd 8-K described how earlier in the week (on Wednesday, February 21) Riot entered into a consulting agreement with an entity called Ingenium International, LLC (“Ingenium”). The filing stated that Ingenium would “provide consulting services related to the Company’s business for a 12 month period” in exchange for consideration of $4 million in cash. The services described included installing, deploying, and monitoring the crypto-currency miners that were recently purchased by the company.

All seemed vaguely plausible at that point, despite the fact that a supposed blockchain company might be expected to have the in-house expertise to deploy its own crypto-mining equipment without shelling out millions to outside consultants.

But putting that aside for the moment, our first sign that this consulting agreement was highly irregular were the payment terms:

In consideration of the Services to be rendered by Consultant hereunder, during the Term the Company agrees to pay to the Consultant (A) $4,000,000 (the “Cash Payment”) upon execution of this Agreement.

Given that the consulting services are supposedly meant to take place over 12 months, we find it odd (to say the least) that the $4 million is to be paid upfront upon signing.

Our second sign that the consulting agreement was highly irregular was that we had already reported that Ingenium appeared to be a suspicious and apparently related party entity of Riot on literally the same day that Riot signed the agreement with them.

In our article from February 21st under the header “A Variety of Other Entities Raise Additional Questions” we named Ingenium as one of two entities that appeared to be an undisclosed related party of the company. We didn’t know at the time whether or what business the entity had transacted with the company. The key link we identified, however, was that the same individuals listed on corporate records for Ingenium matched the names of individuals listed on corporate records for Kairos Global Technology Inc, a subsidiary Riot.

As we wrote in the same section of the article:

Our overall concern with these potentially related entities center around whether shareholder funds could be misused via investments that pass through them.

At the time (i.e., 5 days ago) we even took the time to email Riot’s investor relations and ask whether the company or any of its affiliates or related parties engaged in transactions with Ingenium International, LLC or any of the other believed related party entities. We didn’t hear back.

Just for sport, we emailed investor relations again and asked again whether Ingenium is a related party. We also asked, “Why did you opt to pay the entire $4 million consideration upon execution of the consulting agreement rather than pay over the term of the agreement or upon completion of the actual services the consultant is hired to perform?” We have not heard back as of this writing. Should we hear back from the company we will update this article with its responses accordingly.

Needless to say, we still maintain our original concerns about Riot’s transactions with seemingly related entities.

Director Resignation

The same 8-K reported that Eric So, who was originally appointed director in October 2017, had resigned from the board. In his place, an individual named Remo Mancini was appointed to a variety of important board positions:

“The Audit Committee (Chairman), Nominating and Governance Committee and Compensation Committee of the Board of Directors. Mr. Mancini was also appointed to serve as Lead Independent Director of the Board of Directors.”

Mancini is the owner and President of Sandstone Strategies, which according to his LinkedIn profile is “a Professional Directorship Corporation facilitating Remo Mancini’s service on Boards of Directors.”

Conclusion

We have seen a lot of ridiculous things in our day, but we believe Riot has engaged in some of the most brazen activity we have seen in a U.S. listed equity.

Disclosure: I am/we are short RIOT.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Use of Hindenburg Research’s research is at your own risk. In no event should Hindenburg Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Hindenburg Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in all stocks (and/or options of the stock) covered herein, and therefore stands to realize significant gains in the event that the price of any stock covered herein declines. Following publication of any report or letter, we intend to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation, conclusions, or opinions. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Hindenburg Research is not registered as an investment advisor in the United States or have similar registration in any other jurisdiction. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Hindenburg Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Hindenburg Research does not undertake to update or supplement this report or any of the information contained herein. Hindenburg Research and the terms, logos and marks included on this report are proprietary materials. Copyright in the pages and in the screens of this report, and in the information and material therein, is proprietary material owned by Hindenburg Research unless otherwise indicated. Unless otherwise noted, all information provided in this report is subject to copyright and trademark laws. Logos and marks contained in links to third party sites belong to their respective owners. All users may not reproduce, modify, copy, alter in any way, distribute, sell, resell, transmit, transfer, license, assign or publish such information.