Summary: (NASDAQ:HFFG)

- HF Foods Group (“HF”) is the third SPAC merger orchestrated by Atlantic Acquisition, the sponsor of 2 other infamous public company debacles. First, Wins Finance, whose shares rocketed on allegedly manipulating its FTSE/Russell index qualification criteria, then plunged once ejected from the indices. Second, iFresh, which is down ~95% since its merger amidst a slew of related-party transactions that have sucked shareholder cash out of the business. We think HF Foods is a combination of the worst parts of both Wins and iFresh.

- HF’s massive $509 million merger with food distributor B&R appears to be a blatant undisclosed related-party transaction. The company claimed that the deal was negotiated at “arm’s length”, but we found multiple documents showing that both HF and B&R were part of the same Chinese investment group for years prior to the acquisition.

- HF has transacted with at least 43 separate related-party entities in 2019 alone. Several are based out of the company’s own headquarters and appear to have no operations. We visited others across the country and found red flags suggesting that these related parties are being used by insiders to extract cash from the business.

- We discovered that the company’s trucking subsidiary, ostensibly set up to transport food products, appears to have also used shareholder cash to purchase an undisclosed fleet of exotic supercars including Ferraris, Porsches, and a Bentley. We found photos of the Chairman’s teenage son bragging on Instagram about them being his vehicles.

- HF also directed over $2 million of shareholder cash to business entities owned by the Chairman’s teenage son, including one that bought another fleet of 7 Ferraris with vanity plates such as “FUCKAH0E”, “RUSINGLE”, “IPULL”, “DIKTAT0R”, and “IMHUMBLE”. (And yes, we have photos.)

- We think HF’s auditor has been asleep at the wheel. It was recently subpoenaed by the SEC for its work on iFresh (another Atlantic Acquisition SPAC mentioned above), and was lambasted in its recent Public Company Accounting Oversight Board (PCAOB) inspection report for a multitude of audit failures.

- The B&R merger more than doubled HF’s share count. However, FTSE/Russell mistakenly included almost all of these shares as part of the company’s free float, which sent HFFG’s price and volume soaring on Friday’s index rebalancing. We think this mistake may be reversed.

- We believe HF and its insiders are masking the true number of shares held by its affiliates. Once made clear to FTSE/Russell, we expect the recent forced index buying in HF will reverse and become forced selling.

- We see 90%+ downside for HF’s shares based on outrageously priced fundamentals, insider deals that appear to be hollowing out the company, and potential forced selling by FTSE/Russell.

Initial Disclosure: After extensive research, we have taken a short position in shares of HFFG. This report represents our opinion, and we encourage every reader to do their own due diligence. Please see our full disclaimer at the bottom of the report.

Basics on the Company

On Friday, a relatively unfollowed company called HF Foods Group Inc (NASDAQ:HFFG) (“HF” or “HF Foods”) surged almost 40% mid-day on no news. The stock traded over 1.8 million shares of volume on the day, more than 30 times its 60-day average volume. Investors who track the company might have wondered: “What on earth was that?”

We have been working on this report for months and had predicted that Friday would be the specific day when HFFG’s shares would surge. In fact, we specifically waited until after Friday’s surge before releasing our report. In our report, we provide a thorough explanation for this movement and why we believe it could help contribute to shares plunging well below recent levels.

HF Foods is one of the largest food distributors to Chinese restaurants in the United States. The company supplies over 10,000 Asian restaurants across 21 states, and has two segments: (1) sales to independent restaurants and (2) sales to wholesalers. [Pg. 3]

The company was founded in 1997 by a husband and wife team, Zhou Min Ni (who is currently Chairman/Co-CEO) and his wife, Chan Sin Wong (who formerly served as President and Director).

HF Foods went public via SPAC on August 23, 2018. The stock has since been volatile, particularly around Russell index rebalancing periods (more on this later).

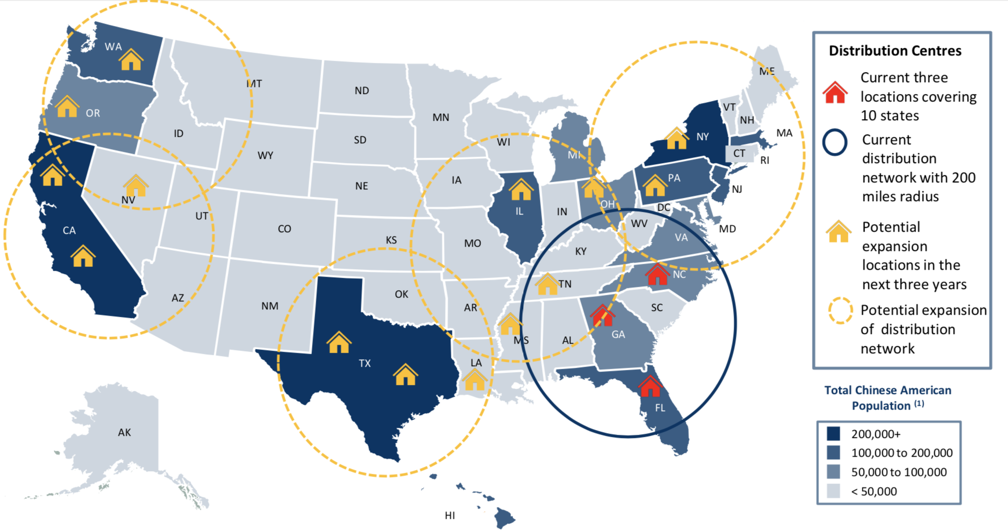

In November 2019, HF Foods merged with B&R Global Holdings, a large West Coast-based Chinese food distributor, in a $509 million two-part deal. The acquisition provided HF Foods more scale, taking its annual revenue from over $300 million in 2019 [Pg. 30] to a combined $828 million. At present, the company discloses ownership of 14 distribution centers located across the East and West Coasts and a fleet of over 340 refrigerated vehicles. [Pg. 3]

Introduction: Dozens of Related-Party Transactions, Failure to Disclose Its $509 Million Mega-Merger was a Related-Party Deal, an Undisclosed Fleet of Supercars and Major Red Flags Around Its SPAC Sponsor and Auditor

Our research on HF, spanning several months, leads us to believe that the company’s insiders are looting the place. We found that the massive $509 million merger with B&R appears to be an undisclosed related-party transaction. Additionally, our report raises red flags relating to transactions with more than 40 additional related-party entities, the company’s apparent use of shareholder cash to purchase a fleet of exotic supercars, the track record of the company’s SPAC sponsor, and regulatory questions about the company’s auditor, who was recently subpoenaed by the SEC and lambasted by the Public Company Accounting Oversight Board (PCAOB).

Background: HFFG Has 60%-80% Fundamental Downside Before We Even Examine Its Most Alarming Issues

HF currently trades at a market cap of roughly $642 million[1] and a total enterprise value of $765 million.[2]

The company’s revenue growth appears to be stagnating while recent profitability has declined precipitously. Its 2019 pro-forma combined revenue was $828 million, representing year-over-year growth of only 1.2% relative to its 2018 pro-forma revenue of $818 million [Pg. 34]. This includes its recent acquisition of B&R. Over the same period, pro-forma net income plunged 64%, declining to $5.6 million in 2019 from $15.7 million in 2018. [Pg. 34]

We expect net income to further decline given (a) plunging margins, which we explain further below and (b) the slowdown caused by COVID-19, which has hurt all restaurants, but has disproportionately affected Chinese and Asian restaurants. [1,2,3]

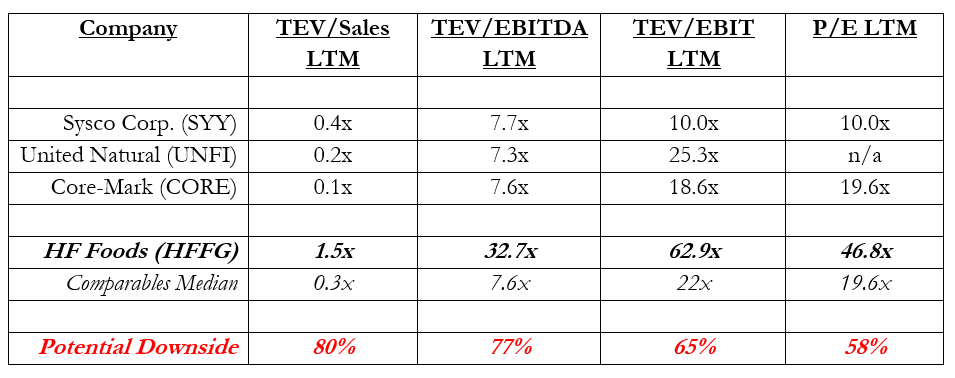

We compared the company to Sysco, United Natural Foods and Core-Mark, three of its closest peers, and found that HF is egregiously overvalued relative to its peer group across key metrics:

When comparing HF’s key financial metrics to peers we see fundamental downside alone of between 58% and 80%.

When we combine our fundamental analysis with what we believe to be other red flags outlined below, we see 90%+ downside from these levels and believe the company to be completely uninvestable.

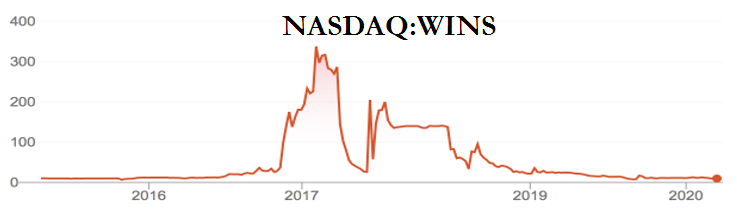

The Sponsor of HF Foods’ Go-Public Transaction Sponsored Two Other Public Company Debacles That Crumbled After, Respectively, (a) Undertaking Numerous Related-Party Transactions, and (b) Allegedly Gaming its FTSE/Russell Index Inclusion Criteria.

We Think HF is Following a Similar Playbook, Which Will Result in The Same Outcome

We think HF Foods is (a) being hollowed out through related-party transactions designed to enrich insiders while (b) gaming its FTSE/Russell index inclusion criteria to drive irregular passive index buying into its stock. These practices are very similar to what ultimately devastated shares of Wins Finance and iFresh, the two above-mentioned companies also sponsored by the backers of HF Foods’ SPAC merger.

The HF Foods go-public SPAC deal was sponsored by Atlantic Acquisition Management, whose two prior SPAC transactions resulted in infamous drubbings for shareholders:

1. Wins Finance Holdings (NASDAQ:WINS). This China-based lending services company reverse-merged with an Atlantic Acquisition SPAC in October 2015, subsequently soaring over 4,500% to a market cap of $9 billion in a move largely driven by passive index buying from the FTSE/Russell indices.

At the time, multiple reporters (1,2,3,4,5) noted the irregular trading, including this example:

Wins fraudulently claimed to own a U.S. office in order to qualify for FTSE/Russell index inclusion, according to a lawsuit filed in 2017 (Wins settled the complaint in 2018). The stock spiked on the inclusion, but FTSE/Russell ultimately removed WINS from its indices. Its shares were halted for 6 months and then crashed spectacularly.

The company is currently late to file its annual report due to an $83 million dollar loan issued to an opaque Chinese entity that the company is no longer certain it can collect.

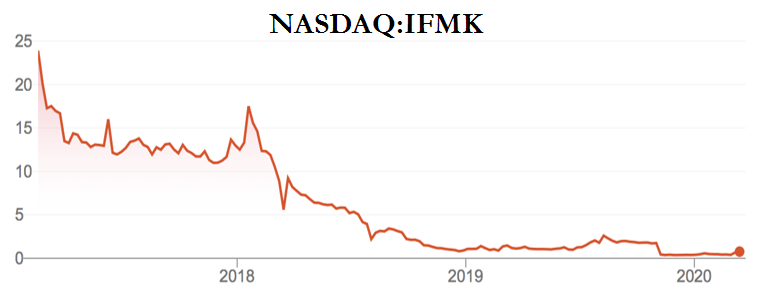

2. iFresh Holdings (NASDAQ:IFMK). This Asian/Chinese food distribution and grocery company was laden with related-party transactions, including acquisitions [Pg. 12], since its go-public SPAC transaction in February 2017. [Pg. 109] At present, in addition to defaulting on its credit agreement [Pg. 44] and having been subject to an IRS tax lien [Pg. 43], the company’s balance sheet remains significantly indebted to related parties. [Pg. 1]

The company is currently fighting a NASDAQ delisting. As of just weeks ago, iFresh announced that both it and its auditor, Friedman LLC, are being subpoenaed by the SEC. Friedman LLC is also the auditor for HF Foods. iFresh has traded down ~95% since going public.

HF Foods’ Massive $509 Million Merger with B&R Appears To Be Just One of Dozens of Suspicious Related-Party Transactions

Our review of HF Foods uncovered a staggering number of related-party transactions, both disclosed and undisclosed, that we believe are suspicious.

These transactions include HF’s $509 million merger with B&R, which we believe is a clear and massive undisclosed related-party transaction. We also found other undisclosed dealings, including a loan to an undisclosed related entity and a fleet of Ferraris and exotic luxury supercars owned by an HF Foods subsidiary.

In addition to undisclosed related-party transactions, the company has also conducted dozens of irregular disclosed related-party transactions.

In total, the company transacted with 43 related-party entities in 2019 alone. [Pg 104–105, Pg. 109] In 2019, HF Foods reported over $40 million in purchases and $19.3 million in sales to related-party entities. [Pg. 67]

Our investigation uncovers related entities with (a) minimal or no online presence, (b) no signage or apparent operations at their respective registered addresses and (c) entities held out as separate companies to investors that appear to actually be operating as part of HF.

We believe insiders are using these dozens of related-party transactions to suck cash out of the business, eventually leaving shareholders with a hollow, debt-laden company.

Undisclosed Related-Party Transactions: HF Group Had Clear Ties to B&R Before Consummating its $509 Million “Arm’s-Length” Deal, Yet None of It Was Disclosed to Shareholders

In June 2019, HF Foods announced it would be merging with B&R Global Holdings, a West Coast food distribution company. The merger was a 2-part transaction valued at a massive $509 million. It included HF Foods issuing 30.7 million shares to former B&R shareholders, more than doubling the company’s outstanding share count and adding ~$101 million in debt to the balance sheet.

According to deal documents, the acquisition process started when HF’s CEO phoned B&R’s CEO in October 2018. [Pg. 27] The deal documents describe the transaction as being negotiated “at arm’s-length”. [Pg. 60]

Contrary to those representations, we found longstanding formal ties between HF Foods and B&R:

- HF and B&R were both under the umbrella of the same investment group, the American International Rongjin Investment Group,[3] according to an announcement by the Chinese Ministry of Commerce in 2012.[4]

- In 2012, an affiliate of the above-named entity also affirmed that HF and B&R are part of the same investment holding group.

- A May 2018 interview with the President of Fujian Rongjin Group (福建榕金集团有限公司), Zhang Yi Tuan (张贻团) also affirmed the relationship. According to the interview, the American International Rongjin Investment Group’s distribution business operates in the U.S. and includes both HF and B&R. According to the interview, the group uses B&R as its official American headquarters and works with HF Foods and others to jointly distribute food in the U.S.

Instead of being “at arm’s length”, these entities look to have been closely affiliated through the same investment group for at least 8 years, which we believe clearly makes them related-parties.

These intricate pre-existing connections represent a major conflict of interest, yet none of this was disclosed to investors prior to, or after, the merger.

Undisclosed Insider Enrichment: An HF Subsidiary Owns a Fleet of Ferraris and Exotic Luxury Supercars, Paid for By Shareholders.

The CEO’s Son Bragged About Them Being His Cars on Instagram

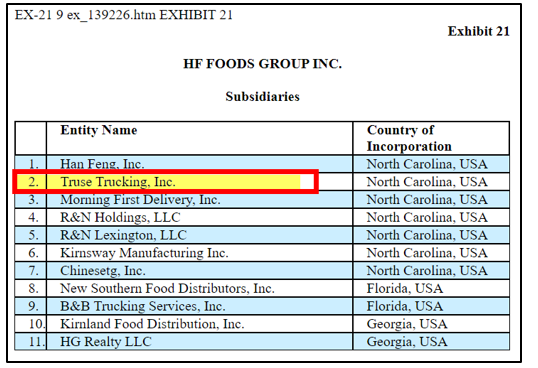

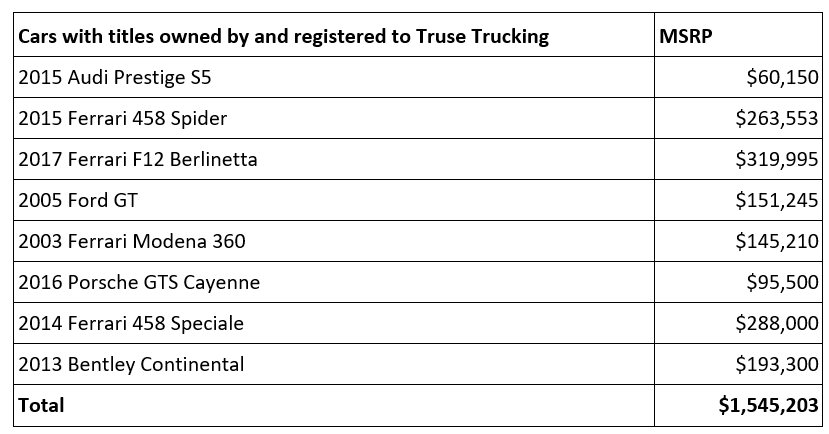

In another series of highly irregular transactions, we examined the assets of Truse Trucking, a company subsidiary:

We performed a background check on Truse, which detailed its vehicle assets. As expected, Truse owns numerous refrigeration trucks that we presume are used to deliver raw and refrigerated food products to the company’s customers. [Example 1, Example 2]

In addition to the fleet of trucks, however, our background check showed that Truse owns an undisclosed fleet of exotic luxury supercars, including Ferraris, a Bentley, a Porsche, and other high-end vehicles with vanity plates such as “RIDEIT69”, “MAKNBBYZ”, “UPGIRL” and “H0P0NIT”.

These, we presume, are not used to deliver raw and refrigerated food products to the company’s customers.

For example, a 2013 Bentley Continental, with an MSRP of $193,000, the license plate “99Pr0BZ” and previous license plate “BENTOVER”, is titled and registered to Truse.

We could think of no business justification for just about any public company purchasing Ferraris or Bentleys with shareholder money. The HF Chairman/CEO’s son puts these vehicles to apparent personal use, bragging openly about his “stable” of cars on his public Instagram account (we expect he’ll soon discover privacy settings). Here he showcases the “BENTOVER” Bentley, captioned with a #fuckahoe hashtag:

A Ferrari, with an MSRP of $319,995 and the license plate “WANTMY” is also registered to Truse Trucking, according to our background check.

We matched this Ferrari and the “WANTMY” license plate to the Chairman/CEO’s son’s Instagram account:

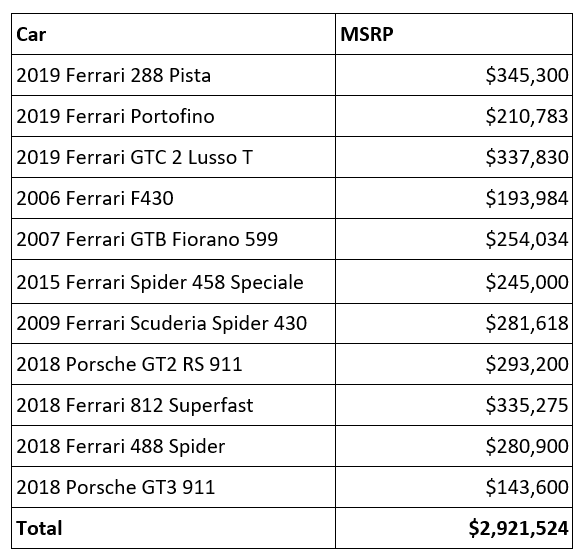

In total, we found 8 luxury supercars valued at a ~$1.5 million MSRP registered to and owned by Truse Trucking:

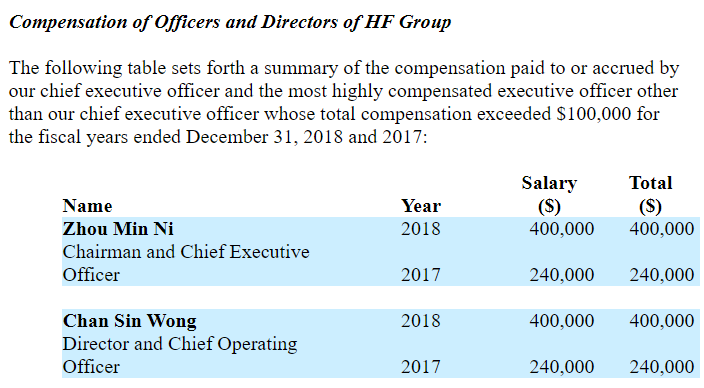

Nowhere do we see any of these cars disclosed as compensation. The Chairman/CEO’s executive salary supposedly consisted of $400,000 in cash [Pg. 98]:

We find these high-end exotic vehicles to be an outrageous use of shareholder capital, especially given the severe deterioration of the company’s profitability.

HF’s Disclosed Related-Party Transactions: Doing Business with At Least 43 Different Related-Party Entities

We also think HF’s insiders are drawing cash from the business through its disclosed related-party transactions.

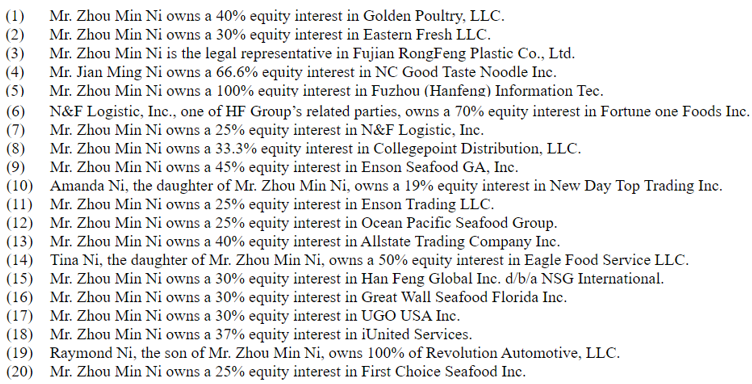

HF reported transacting with a staggering 43 different related-party entities in 2019 alone, including over $40 million in purchases and $19.3 million in sales from and to the entities [Pg. 67] [Pg. 104, Pg. 109]. Many are owned all, or in part, by the Chairman/CEO and his immediate family, as shown from the table below that lists 20 of these entities:

Major Discrepancy: Customers Are Told Some of These Entities Are Part of HF Foods, Yet Shareholders are Told The Entities Are Separate (Which Allows Insiders to Extract Cash)

When HF Foods went public, its merger documents [Pg 8] and investor presentation [Pg. 20] claimed that the company owned and operated three distribution centers. It also advertised an “expansion plan” to extend its business beyond the American Southeast:

However, well before HF Foods went public, its customer-facing subsidiary “Han Feng Inc.” already claimed to operate 20 distribution centers (see below):

This same website’s Chinese-language portal has a more detailed map, showing that HF Foods had already been operating distribution centers where the company told investors it planned to expand:

Many of the distribution centers on the Chinese-language website match the names of entities HF now claims are separate entities that insiders own equity stakes in (Fortune One Foods, N&F Logistic, Allstate Trading).

So, which is it? As we detail later, our on-site investigations of several entities showed signs that they operate as part of Han Feng. In some cases, employees on-site confirmed it for us (which we have recorded).

We believe insiders have retained this network of entities, which were not consolidated into HF Foods, in order to extract cash from HF and its shareholders.

HF’s Disclosed Related-Party Transactions: Wholesale Margins to These Entities Collapsed Immediately After the IPO. Cash Seems to Be Slipping Out the Back Door

HF reported a ~33% collapse in its wholesale gross margins in the quarter after it went public, by related-parties that presumably benefitted from the margin compression.

The company acknowledges that the margin decline was due to related-party sales, but tried to explain it away by citing volume discounts:

“The decrease in margins resulted form (sic) increased sales to related parties relative to total wholesale revenue in 2018 as compared to 2017. The wholesale price for related parties is generally lower than third party customers due to the larger quantities purchased by related parties.” [Pg. 30]

This explanation is puzzling. Sales only grew ~3% year over year for the comparable 2019/2018 9-month period, so there was no surge in volume. Furthermore, the company disclosed that related parties constituted 92% of wholesale segment sales in 2017 [Pg. 30], making it impossible for related business to have meaningfully increased. [Pg. 32]

Our investigation of these related-party entities uncovers a different explanation for why the company’s sudden wholesale margins have collapsed: insiders appear to be looting the place.

We investigated several of these entities in detail, including on-the-ground field research on both the East and West Coast. All told, we believe these related-party transactions are largely shams designed to extract cash from the business.

$4 Million Of Shareholder Cash Was Used for Purchases and Advances to Revolution Industry, An Entity Based Out of HF Foods’ Headquarters, Owned 100% By The Chairman/CEO’s Son, That Was Formed 1 Month Prior to the IPO Deal, With No Visible Signs of an Actual Business

HF Foods discloses transacting ~$3.3 million in purchases from, and directing over $700 thousand in advances to Revolution Industry. [Pg. 106, Pg. 21] Revolution Industry is 100% owned by the Chairman/CEO’s son and claims to do business in “food processing” and “distribution” according to its North Carolina corporate filings.

We find it suspicious that HF Foods directed ~$4 million in business to the Chairman’s son, who was likely a senior in high school at the time, according to social media posts.

Note that HF’s SPAC sponsor announced the deal to take HF public in March 2018. Revolution Industry was formed just one month earlier, according to North Carolina corporate records.

We found no signs that Revolution Industry is an actual business—no website, no social media profile, and no evidence of it having customers.

Even more suspicious, North Carolina corporate records show that the entity is registered to the same address as HF Foods’ headquarters: 6001 West Market Street, Greensboro North Carolina:

As shown below, this entity’s address matches the address of HF Foods’ headquarters:

What kind of food could HF be distributing to an entity based out of its own address? We think the only thing being distributed is money to insiders.

$483,000 in Loans to Revolution Automotive, Another Related-Party Entity Owned 100% by the Chairman/CEO’s Son to Buy Yet More Ferraris

License Plates of the Vehicles, Apparently Paid for With Shareholder Cash: “FUCKAH0E”, “69PRBLMZ”, “RUSINGLE”, “IPULL”, “DIKTAT0R”, “IMHUMBLE”

HF Foods also extended $483,000 in loans to the similarly named “Revolution Automotive” (not to be confused with the above-mentioned “Revolution Industries”). These loans were distributed around the time of the March 2018 take-public deal announcement. [Pg. 107]

Revolution Automotive is also 100% owned by the Chairman/CEO’s son, according to HF Foods’ filings [Pg. 65], and is also registered to the address of HF Foods’ headquarters, according to the North Carolina Secretary of State. Once again, we couldn’t find any business operations by “Revolution Automotive”.

The only discernible assets held by Revolution Automotive are titles to 9 Ferraris, according to our background check:

The Chairman’s son boasts about this armada of Ferraris, each apparently purchased with investor cash, on his Instagram:

While the tags appeared on our title / registration background check, some have likely been revoked due to North Carolina DMV’s poor taste rules. We noticed that several of these sports cars seemed to cycle through different distasteful license plate names every couple of years.

As to the loan balance owed to shareholders, the Chairman/CEO recently paid it off personally with shares of illiquid HF stock. [8-K, Pg. i]. This, in our view, allowed him to draw cash out of the business in exchange for nearly worthless paper.

Over $1 Million Of Shareholder Cash Has Gone to UGO USA Inc., Another Related-Party Entity Registered to HF Foods’ Headquarters with Few Signs of Operations

HF Foods has made almost $1 million of purchases over the past 2 years from UGO USA, Inc, another related-party entity based out of HF’s headquarters. According to company filings, HF’s Chairman/CEO owns a 30% equity interest in UGO. [Pg. 105] Jin Yan Ni, who we believe may be a relative to the Chairman (based on matching surnames), set up and manages this entity according to North Carolina corporate records.

UGO claims to be in the “wholesale” business. We see the address once again matches HF Foods’ headquarters:

We found little evidence that UGO is an actual operating business, though it appears it had taken steps to become one in the past. In 2016, the entity filed a trademark application for “on-line retail store services featuring Asian snacks, Asian beauty products, Asian health supplements, Asian home appliances, and Asian restaurant supplies.” We were unable to locate any online store or online presence.

We also found that the company imported a total of 3,000 pounds of coconut chips in two shipments between 2016 and 2017, according to ImportGenius. These records show that the 2 shipments were imported from Thailand and directed to 99 New Hook Road in Bayonne, New Jersey, which happens to be the address of another HF Food related-party called Eastern Fresh [Pg. 107] (which we detail further below):

We called the number listed on UGO’s LLC form to learn more about the business, but no one picked up.

$11.6+ Million of Shareholder Cash Went to Eastern Fresh, An Entity HF Foods Claims is a Separate Business. Signage at the Facility Has HF’s Logo, Indicating Otherwise

Since 2017, HF has directed $11.6 million into Eastern Fresh LLC, a company that HF’s Chairman/CEO owns a 30% equity interest in. [Pg. 104] Eastern Fresh appears to be registered as “Eastern Fresh NJ LLC”, a distributor based in New Jersey.

Despite HF filings claiming that Eastern Fresh is not a subsidiary (but rather a separate related-party), its signage appears to bear the logo of HF’s customer-facing subsidiary, Han Feng, Inc. [Pg. 16]

Here is Han Feng’s logo from its website:

And here is Eastern Fresh’s sign, clearly showing the Han Feng logo:

Here is a closer look. It even says “Han Feng” underneath the logo:

Similarly, Eastern Fresh identifies with Han Feng inside its facilities, according to photos found on its Facebook page:

Again, HF appears to be presenting a unified face to customers, while separating these entities from investors. This is consistent with what we would expect if these entities are being used to funnel out shareholder cash.

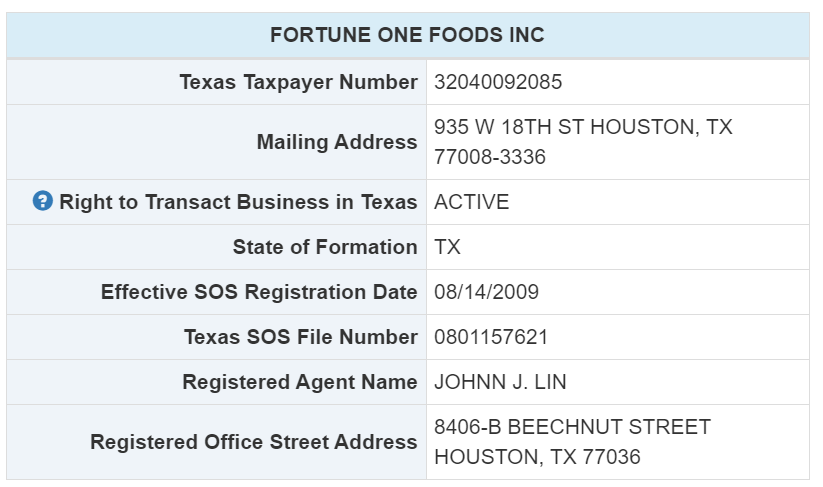

$1.8 Million in Shareholder Cash Went to Related-Party Fortune One Foods. Once Again, HF Foods’ Filings Describe it as a Separate Entity. But Fortune One Describes Itself as Being a Part of HF Foods

HF’s Chairman/CEO indirectly owns a 17.5% equity interest in Fortune One Foods Inc. [Pg. 104] HF has made about $1.8 million in purchases from the entity, according to company filings. [Pg. 104] Although filings claim that Fortune One is not an HF subsidiary, but instead a separate related-party entity, Fortune One appears to brand itself as if it were part of HF.

We were unable to find any website for this entity. Fortune One does have a Facebook page, however, which describes it as a distributor under Han Feng (i.e., HF), and points to the HF website:

We decided to investigate Fortune One by visiting its registered address found on its Texas corporate records.

Here is the matching address at 935 W 18th Street from our visit:

During our March visit, we observed a fleet of vehicles that appear to be used for delivering food, a loading bay and a warehouse – all things we would expect from a distribution business.

There was no signage indicating “Fortune One” on the inside or the outside of the facility, as far as we could tell (the neighboring business was called “Jake’s”):

However, several trucks did bear a Fortune One logo:

We sent an email to Fortune One in March to inquire as to whether it transacts with any customers other than HF Foods and why it cites HF Foods’ website as its own. We have not received a response as of this writing.

We also called the number listed on its Facebook page and asked a representative point blank if it was an independent business or if it was part of Han Feng. His reply (which we have recorded) was: “Yeah we are a part of Han Feng.” He also confirmed to us that Fortune One has its own fleet of trucks.

All told, we find it alarming that Fortune One describes itself as being a part of HF Foods, whereas HF Foods does not include it as a subsidiary. Instead, it reports it as a separate related-party entity, allowing insiders to personally profit from transactions with it.

NC Noodle, A Related-Party Owned By HF’s Previous CFO, Made ~$4.2 Million In Sales To HF, But Our On-The-Ground Research Showed Its Premises To Be Largely Vacant

HF states that the company’s recently departed CFO owns a 66% equity interest in NC Noodle. [Pg. 105] Based on HF’s disclosures, we estimate that NC Noodle sold ~$4.2 million to HF in 2019 alone, yet we found no customer-facing business presence online.

We paid a visit to the company’s principal business address during normal working hours to try and speak with management and get an understanding of the business. Given the volume of product sold to HF during the year, we expected a sprawling operation.

Instead, we discovered what our investigator described as a “completely vacant” building except for 3 employees handling a pallet of product in an otherwise empty-looking back warehouse (see below):

Our investigator asked the employees about the business but was unable to learn anything due to a language barrier, so he left.

NC Noodle is headquartered less than 10 miles away from HF Foods’ warehouse in North Carolina.

We suspect this is little more than an insider-owned entity that sells product to nearby HF. We have serious doubts about whether this “middle man” provides value to anyone but HF insiders.

HF’s Chairman Has Effectively Sold Almost 10% Of His Shares by Purchasing ~$12 Million in Loans Made by HF And Paying Them Back With His Own Illiquid Stock

In another series of incestuous and alarming related-party transactions, HF’s Chairman/CEO bought cash loans issued by HF to related and non-related parties and paid these loans back using shares of his illiquid HF stock.

The Chairman/CEO’s transactions include purchasing loans originated by HF Foods to his son’s “business”, Revolution Automotive, along with other related parties.

According to company filings, on September 30, 2019, the Chairman/CEO delivered 1,203,803 shares to the company to purchase ~$12 million in loans issued by HF (8-K) to the 4 different entities listed below:

According to the 8-K:

“Under the terms of the Loan Sale Agreement, Mr. Ni has acquired the Related-Party Loans without warranty or recourse and has assumed all risks of non-collection”

We think this shuffling of assets is nothing more than a way for the company’s Chairman/CEO to unload his otherwise illiquid and overvalued stock, while extracting cash from the company through related-party loans.

HF’s Auditor, Recently Subpoenaed By The SEC, Has a History Of Reportedly Failing To Obtain Sufficient Evidence To Support its Audit Opinions

We are not surprised that HF’s auditor, Friedman LLC, has not uncovered the many issues outlined in this report.

As noted earlier, iFresh, another company backed by HF’s SPAC sponsor, is also audited by Friedman. Similar to HF, iFresh has a history of numerous related-party transactions dating back to its own go-public transaction. On March 6th 2020, iFresh announced that it, along with its auditor, had received a subpoena from the SEC relating to its work on the company:

In addition to current regulatory issues, Friedman’s recent inspection by the Public Company Accounting Oversight Board (PCAOB) found material issues. The PCAOB 2018 inspection report suggested that Friedman had failed to perform its basic function as an auditor: providing reasonable judgment as to whether financial statements are free of material misstatement, whether by error or fraud. The PCAOB report is scathing:

“Certain deficiencies identified were of such significance that it appeared to the inspection team that the Firm, at the time it issued its audit report, had not obtained sufficient appropriate audit evidence to support its opinion that the financial statements were presented fairly…”

“In other words, in these audits, the auditor issued an opinion without satisfying its fundamental obligation to obtain reasonable assurance about whether the financial statements were free of material misstatement and/or the issuer maintained effective ICFR.”

The PCAOB report further identified weaknesses with Friedman’s audits of 3 unnamed issuers, including (a) failures to test the controls and valuation of revenue, (b) failure to test controls over inventories and (c) “the failure to perform sufficient procedures to test the existence of investments”.

What Happened with Friday’s FTSE/Russell Forced Index Buying And Why We Think It Will Prompt Subsequent Forced Selling of HFFG Shares

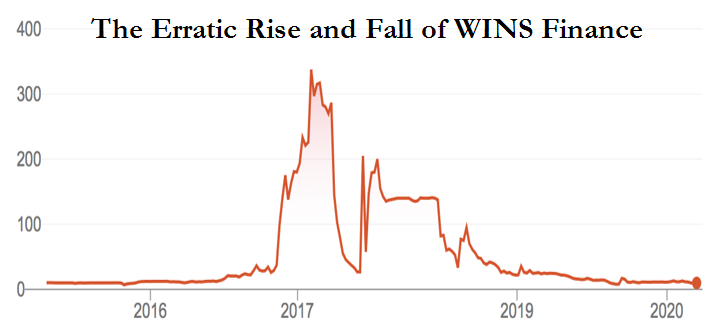

As noted earlier, the sponsor of HF’s SPAC transaction, Atlantic Acquisition, has a history of sending socks soaring due to the alleged manipulation of company inclusion criteria for the FTSE/Russell indices. The 4,500% spike in Atlantic-backed Wins Finance still serves as the classic example of a passive index forced-buying bonanza (followed by a passive index forced-selling bonanza), a process that played out several times over the history of Wins:

Similar to Wins, we have seen irregular spikes and troughs in HF’s shares precisely around rebalance dates.

Beyond HF’s mid-day ~40% spike on massive index buying volume last Friday, a similar scenario unfolded in June 2019 around the FTSE/Russell index reconstitution. The week leading up to the rebalance coincided with a price spike of ~65%, followed by a ~48% crash the following week, all despite an apparent absence of news. As seen below, the company has had regular price and volume spikes around these reconstitutions.

For context, when index funds buy stocks, they weight the purchases according to a company’s free float (essentially the number of shares freely traded). In other words, the more freely traded shares, the more shares the passive indices will buy.

So what happened during Friday’s index rebalancing that led to a surge in HFFG’s price and volume?

FTSE/Russell had calculated HFFG’s free float to be 21.8 million shares (per its subscription-only service). This calculation was just flat out wrong. The freely tradable shares were 6.2 million per HF’s own recent March filing. [Pg. 25]

The source of the mistake appears to have been the accidental addition of shares from the B&R transaction, which closed in November. As with every such merger, shares issued to the acquirees are restricted for at least 6 months, according to SEC Rule 144. FTSE/Russell apparently missed this and added the shares to its free float calculation anyway. We think FTSE/Russell should reverse this decision, which would lead to a forced selling of the shares purchased.

Beyond the above, which appears to largely be a FTSE/Russell error, sometimes companies are able to juke the index rebalancing process to ensure that the actual free float is tighter than it appears. We think this may also be taking place.

For example, as shown earlier, to the extent that shares are held by family members or affiliates (potentially through dozens of related-party entities), this can serve to constrain the true free float. Given the sheer consistency of the index rebalancing irregularities around HF (and Wins, backed by the same sponsor), we believe this to be likely. To the extent Russell takes action, forced sales by passive investors could add severe selling pressure to HF’s shares.

Conclusion: We Believe HFFG’s Shares Have 90%+ Downside

In Latin, res ipsa loquitur means, “the matter speaks for itself”.

We think the evidence compiled regarding HF’s troubling related-party transactions, its flagrant misuse of shareholder cash, its potential gaming of the FTSE/Russell index criteria and the track record of its auditor and SPAC sponsor speaks for itself.

Besides the troubling issues presented by our report, we believe HFFG faces 58% to 80% downside based on fundamentals alone.

Given the totality of our findings – and what the resultant investor, analyst, and regulatory responses to these findings could be– we believe HFFG faces 90%+ downside and is ultimately uninvestable.

Disclosure: We are short shares of HFFG

[1] Based on current shares outstanding of 52,145,096, per the recent 10-K

[2] Includes net debt as of June 30th from the B&R merger of 22,888,079 (34,959,731-12,071,652) [Pg. 24] plus $101 million in debt from the subsequent real estate acquisition

[3] Note that Rongcheng is the Chinese translated name of B&R and Hefeng is the Chinese translated name of HF Foods

[4] California entity records from 2006, show Zhang Yi Tuan as the initial agent for the B&R entity, which further corroborates the connection.

Legal Disclaimer

Use of Hindenburg Research’s research is at your own risk. In no event should Hindenburg Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Hindenburg Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in all stocks (and/or options of the stock) covered herein, and therefore stands to realize significant gains in the event that the price of any stock covered herein declines. Following publication of any report or letter, we intend to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation, conclusions, or opinions. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Hindenburg Research is not registered as an investment advisor in the United States or have similar registration in any other jurisdiction. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Hindenburg Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Hindenburg Research does not undertake to update or supplement this report or any of the information contained herein.

5 thoughts on “HF Foods: 90%+ Downside on Massive Undisclosed Related-Party Transactions, Shareholder Cash Spent on Exotic Supercars & Outrageous Fundamental Valuation”

Comments are closed.

great research !!

Fantastic work guys.