(NASDAQ:KNDI)

- Today we reveal what we believe to be a brazen scheme by China-based, NASDAQ-listed Kandi Technologies Group to falsify revenue using fake sales to undisclosed affiliates.

- Our investigation included extensive on-the-ground inspection at Kandi’s factories and customer locations in China, interviews with over a dozen former employees and business partners, and review of numerous litigation documents and international public records.

- We unmasked Kandi’s “unnamed” top customers and found that almost 64% of Kandi’s last twelve months (LTM) sales have been to undisclosed related parties.

- The company’s largest customer, representing ~55% of last twelve months (LTM) sales, shares a phone number with a Kandi subsidiary, and shared an executive with Kandi.

- We visited the “customer”. It is based in a tiny building right next to Kandi’s factory with a sign indicating that it’s a Kandi company. The same building housed another entity used by Kandi as part of a separate fake sales scheme to collect illegitimate subsidies from the Chinese government, for which it was fined and sanctioned.

- Kandi’s second largest customer, representing ~9% of LTM sales, was once wholly owned by the company. Its website still integrates the Kandi logo with the customer name. Export records show that 91% of the U.S. exports by the “customer” went to undisclosed related party entities based out of Kandi’s U.S. headquarters and warehouses.

- To support this, we have photographic evidence of one such Kandi “customer’s” inventory sitting in Kandi’s own warehouse.

- Kandi’s financials corroborate our concerns. The company has consistently booked revenue it cannot collect, a classic hallmark of fake revenue. Its Days Sales Outstanding (DSO) a common measure of revenue collection, was 278 days in the previous quarter, about 5.6x worse than its closest auto peer.

- Kandi’s top financial ranks have been a revolving door; another key sign of accounting irregularities. The company has had 3 auditors in the past 5 years, and 4 Chief Financial Officers in the past 4 years.

- Kandi’s current auditor, Marcum, was just handed a 3-year ban from auditing Chinese companies by the Public Company Accounting Oversight Board (PCAOB). Rather than firing the auditor, Kandi just reported its intention to renew the engagement.

- Kandi’s latest issues are part of a long-running pattern, rather than an isolated incident. The architects of Kandi’s original go-public transaction were charged with fraud by the SEC in 2014 for, among other things, engaging in a scheme with Kandi’s (still) Chairman/CEO to artificially inflate its stock price.

- In 2016, Kandi’s long-serving prior auditor was ejected from the industry by the PCAOB specifically for failure to catch obvious signs of fraud at Kandi, including misappropriation by company management and undisclosed related party transactions.

- Kandi’s latest pitch to investors is focused on an imminent U.S. launch. We show that Kandi has been “launching” in the U.S. for 12 years. Its first U.S. vehicles were imported illegally and seized by customs. A former distribution partner said every single car that eventually made it into the country broke.

- Kandi has a reputation in China for poor quality vehicles and failing to honor service warranties. The company has reported no domestic EV sales for years outside of its minority stake in a joint venture. We expect its U.S. efforts will continue to sputter.

- We also review Kandi’s partnership with a Chinese rideshare company, which it has repeatedly claimed could lead to up to 300,000 EV sales. We show that the rideshare partner’s app is mostly vaporware; it has almost no users and isn’t even ranked among China’s top 50 rideshare apps.

- Lastly, we address the company’s much-touted battery swap program, which is preliminary and hopelessly behind peers, including Kandi’s own partner Geely. Without a meaningful number of cars on the road Kandi’s battery swap efforts simply don’t make sense.

- Kandi raised $160 million from U.S. investors this month alone. All told, we think Kandi has engaged in a major fake revenue scheme, hyping its story to U.S. investors, in order to take advantage of regulatory gaps enabling China-based companies to siphon cash from U.S. capital markets with impunity.

Initial Disclosure: After extensive research, we have taken a short position in shares of Kandi Technologies. This report represents our opinion, and we encourage every reader to do their own due diligence. Please see our full disclaimer at the bottom of the report.

Introduction: Electric Vehicle Euphoria

Many investors have come to the realization that electric vehicles are the future of the auto industry. In rational times, such investors might express this view by picking companies that are best-of-breed; the likely industry winners.

But this is 2020, so instead, a psychotic flood of speculative capital has lifted all companies in the sector, regardless of quality.

Readers of this piece are likely familiar with our views on Nikola, the electric vehicle brainchild of Trevor Milton, a man who has forever enshrined “gravity” in the list of zero-emission energy sources (perhaps the company’s only genuine innovation to date).[1]

Many investors avoided Nikola due to its speculative status as a pre-revenue newcomer. Some of these investors may have instead found Kandi, seeing it as a revenue generating EV manufacturer with a long history.

Background: Basics on the Business

Before we dive into the specifics, let’s review the basics.

Kandi went public in the U.S. in mid-2007 via reverse merger onto the Over the Counter (“OTC”) market. It then uplisted and has traded on the NASDAQ since March 2008. [Pg. 14] The company has been run since its inception as a public company by Xiaoming Hu (胡晓明) who serves as Chairman, CEO & President. [Pg. 33]

Historically, the company manufactured and sold ATVs, go-karts, and electric vehicles. Currently, Kandi’s main focus is electric cars and related parts.

Kandi has announced several initiatives that are key to its business case (which we will review thoroughly):

- The “U.S. Launch” of Kandi’s small, low-cost electric cars;

- China’s domestic rideshare market, which Kandi hopes to significantly participate in; and

- The company’s battery swap technology, which it has indicated will be spun off and taken public in Shanghai

The company’s market cap has expanded to over $1 billion as of this writing, trading ~$13.62 per share, more than 6x its 52-week lows. The company has raised $160 million from U.S. public market investors this month alone. [1,2]

Part I: Kandi’s Extensive History of Fraud Allegations

Investors in Kandi seem largely unaware of the company’s history of credible fraud allegations during its tenure as a public company.

2014: The Architects of Kandi’s Reverse Merger Deal to Go Public Were Charged With Fraud by the SEC For, Among Other Things, Engaging in A Scheme With Kandi’s Chairman/CEO To Artificially Inflate Its Stock Price

According to an SEC complaint, Kandi was taken public on the OTC by a group of individuals that engaged in multiple market manipulation schemes. [Pg. 3]

The architects of the scheme were charged with fraud by the SEC in 2014.

The complaint included allegations that the individuals had engaged in a fraudulent scheme to inflate the price and volume of Kandi. [Pg. 43] According to SEC prosecutors, the scheme was concocted with the help of Kandi’s CEO:

The individuals settled the charges in December 2019. Despite the Chairman/CEO of Kandi being identified as playing a critical role in a conspiracy to manipulate his own stock, neither he nor the company were ever charged by the SEC.

2016: Kandi’s Long-Serving Auditor Had Its Registration Revoked by the Public Company Accounting Oversight Board (“PCAOB”) Specifically for Failing to Catch Obvious Signs of Fraud at Kandi

Kandi’s auditor for most of its publicly traded existence was Albert Wong & Co. (“AWC”), a small auditor based in Hong Kong. AWC served as Kandi’s auditor from mid-2009 until its dismissal in April 2016.

A month after its dismissal, in May 2016, the PCAOB issued an order revoking AWC’s registration, fining it $10,000 and barring its principals from associating with any registered public accounting firm due to its failure to catch obvious signs of fraud at Kandi.

The order focused on AWC’s audit failures relating to Kandi, mentioning the company by name 151 times.

The PCAOB found, among other failures, that AWC failed to implement procedures designed to provide reasonable assurance of detecting material fraud or illegal acts. [Pg. 4]

The PCAOB Report Went Into Detail About Obvious Signs of Theft by Kandi’s Chairman/CEO And Undisclosed Related Party Transactions

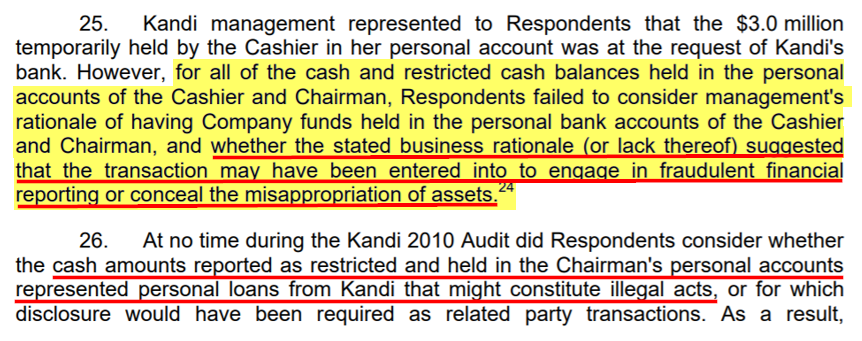

The PCAOB found that AWC failed to take issue with Kandi’s Chairman and at least one Kandi finance employee (referred to as “Cashier”) reporting cash held in their personal accounts as belonging to the business. The auditors simply included the cash held in personal accounts in the company’s reported cash balance.

The effect of this was likely a reporting of an inflated cash balance while direct evidence of misappropriation was ignored. Per the report:

The PCAOB report referred to Kandi’s responses as “evasive” [Pg. 12] and repeatedly called into question the reliability of its representations and integrity. [Pgs. 8-9, 13]

The PCAOB Report Went into Further Detail About Obvious Undisclosed Related Party Transactions At Kandi, Including Those Relating to Kandi USA

The report also suggested that management made adjustments to disguise recognition of related party revenue:

“Respondents failed to assess the risk of fraud related to these last-minute adjustments to reflect the Kandi USA revenue as being from Dingji, including whether these adjustments were motivated by management’s desire to conceal Kandi’s transactions with Kandi USA in order to avoid related party disclosures.” [Pgs. 12-13]

Note that elsewhere in this report, we have detailed specific and obvious signs that Kandi is still engaging in extensive undisclosed-related party transactions through its U.S. operations.

Despite the PCAOB barring AWC and its principals from auditing public companies for failing to identify clear signs of fraud at Kandi, domestic regulators have not brought any enforcement action against Kandi.

2016: The Chinese Government Announced That Kandi Had Been Involved in a Scheme Through its Joint Venture to Obtain Illegitimate EV Subsidies Through the Use of Sham Sales to Related Parties

In 2013, the Chinese government announced large subsidies to producers of electric vehicles. That same year, Kandi and Chinese EV manufacturer Geely established a joint venture to produce electric vehicles.

According to Chinese media, the joint venture generated subsidies through a scheme involving buying and selling to/from related parties.

The gist of the scheme was as follows: China provided subsidies to both to producers and purchasers of electric vehicles. Kandi gained one subsidy through its manufacturing joint venture with Geely, then sold the cars to a related party entity that purported to be in the rental/car sharing business, collecting the other.

The scheme worked because Kandi’s cars were so cheap. The cost to build the vehicles was actually less than the subsidies, so Kandi just needed to build as many cheap cars as possible to cash in on the government money.

In 2016-2017, media reported on the results of a Chinese government investigation which found that Kandi and its JV partner (among others) had thousands of idled vehicles and was involved in fraudulently obtaining state subsidies.

As a result, Kandi’s JV partner was fined and Kandi was forced to write off $3.3 million in subsidies.

In 2019, media stumbled across a car lot where thousands of Kandi cars were apparently sitting unused and had been deteriorating for years, believed to be part of the same scheme.

2017: Kandi Restated Its Financials to Account for Previously Undisclosed Related-Party Deals and Promised to Mend its Ways

On March 7, 2017, the company acknowledged in an SEC filing that in response to questions from the SEC’s Division of Corporate Finance, it needed to restate its historical financials to “separately identify certain related party accounts” and make “corrections to the classification of notes receivable and notes payable in the Company’s statements of cash flow”.

The filing stated that investors should not rely on its financial reporting “or any earnings releases or other communications” from 2014-2016.

The same filing disclosed that Kandi’s accounting may have material weaknesses and that the PCAOB revoked the registration of its prior auditor due to deficiencies.

Part II: We Think Most of Kandi’s Sales Are Fabricated

Kandi was not charged by regulators for any undisclosed self-dealing, despite extensive historical evidence suggesting a pervasive pattern.

Part of the issue, we think, is that U.S. regulators have limited access to audit and regulatory information from China, leaving them hamstrung in their overseas enforcement efforts.

In 2017, the company promised to do better going forward, but given the lack of regulatory oversight and consequences: why would it?

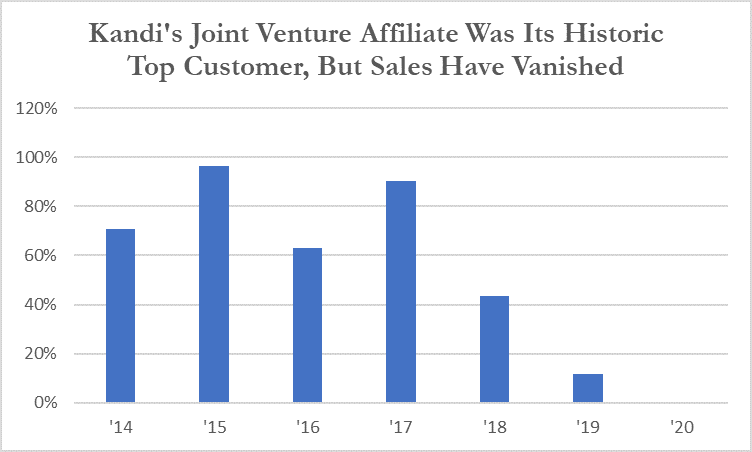

Background: Kandi’s Top “Customer” From 2014-2017, Representing 63%-97% of its Sales, Was its Joint Venture Partner

But Following the Subsidy Scandal, Sales to the JV Partner Evaporated

Since 2014, Kandi’s reported EV sales had been driven by its joint venture with domestic auto manufacturer Geely.[2] [Pg. 11] But Kandi’s sales to its JV partner declined sharply by the end of 2018 following revelations of a Chinese subsidy scandal and subsequent subsidy policy adjustments.

Through its overgenerous subsidies, the Chinese government inadvertently acted as a dedicated “buyer” of Kandi’s cars (many of which ended up just rusting in a parking lot, as shown above). Without the subsidy scheme run through its joint venture entity, Kandi needed legitimate buyers for its products.

In Q1 2019, Kandi acknowledged on its quarterly investor call that it didn’t sell any EV products due to a “transitional period”. Kandi’s financials show that its proportion of sales to its joint venture rapidly declined and have essentially vanished in 2020.

This is corroborated by Chinese media sources, which reported that the company sold zero vehicles domestically in 2019 and early 2020. [1,2,3]

Kandi’s joint venture with Geely was originally 50/50, but Geely bought most of Kandi’s stake in 2019, leaving Kandi with 22%. The entity is now focused on manufacturing an electric SUV called the Maple 30X. Given Kandi’s lack of reported revenues from the affiliate, it is unclear what current role, if any, Kandi plays in its manufacturing.

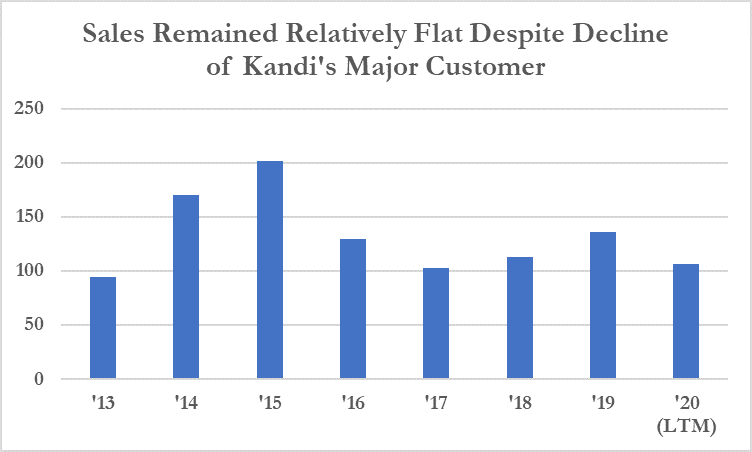

Despite the Virtual Elimination of Kandi’s Major Customer, Kandi’s Revenue Somehow Remained Stable…With the Help of Two Unnamed Mystery Customers

Usually sales drop when a firm suddenly loses its business from a customer comprising 63%-97% of sales.

Incredibly, that has not been the case with Kandi. Its sales actually rose slightly following the 2018 decline of its top customer, then leveled off.

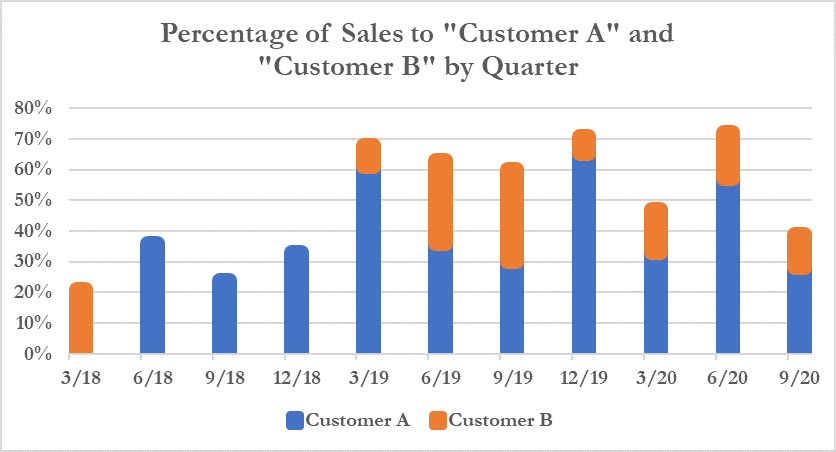

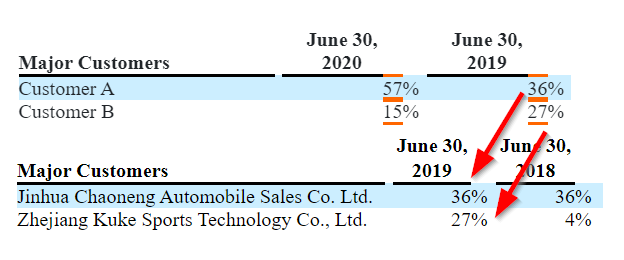

Kandi Redacts the Names of its New Top “Customers” Which Have Accounted for Almost 64% of Last Twelve Months (LTM) Sales

Two unnamed customers have played a big role in plugging up the sales “hole” left behind by the decline of Kandi’s JV. Kandi redacts the name of these key customers on its financials, referring to them as “Customer A” and “Customer B”.

We Have Identified the Names of Kandi’s Top Customers

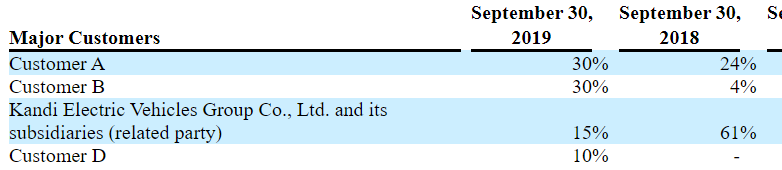

Prior to September 2019, Kandi disclosed the names of its top customers. Here is an example from June 2019:

As of September 2019, the company began redacting the names of its top customers, except for the name of its related party joint venture partner:

The remaining customers, according to Kandi’s disclosures, are sales to unrelated party customers.

We were able to identify Kandi’s top customers by connecting the dots between the percentage of sales associated with each customer in the prior periods when the names were unredacted.

For example, customer concentration disclosures from June 2020 referenced the customer concentration numbers from the prior year (when the names were unredacted). [Pg. 10, Pg. 17]

Once unmasked, we examined the customer relationships more closely and found alarmingly close ties to Kandi.

Kandi’s New Top Customer, Accounting for 55% of LTM Sales, Shares a Phone Number with a Kandi Subsidiary

According to Chinese corporate records available through corporate records service QCC, key customer Jinhua Chaoneng Automobile Sales (金华市超能汽车销售有限公司) shares its phone number with a 100% Kandi-owned subsidiary.

Here is Jinhua’s corporate record, with its phone number highlighted, including an indication that it shares the number with three other entities:

The second name on the list of shared numbers is Zhejiang Kangdi Intelligent Power Exchange Technology Co., Ltd. (浙江康迪智能换电科技有限公司), which is 100% owned by Kandi.

We called the number to see which (if any) company the phone number belonged to. This was the conversation (which we recorded):

HER: Hello

US: Hello. Are you Jinhua Chaoneng?

HER: No

US: What company are you?

HER: Who are you?

US: I’m looking for Jinhua Chaoneng and had this number

HER: They moved away many years ago

US: Oh, then are you Kandi?

HER: Who are you?

US: I’m looking for these companies. I want to check if this phone number belongs to Chaoneng or Kandi or who?

(HANGS UP)

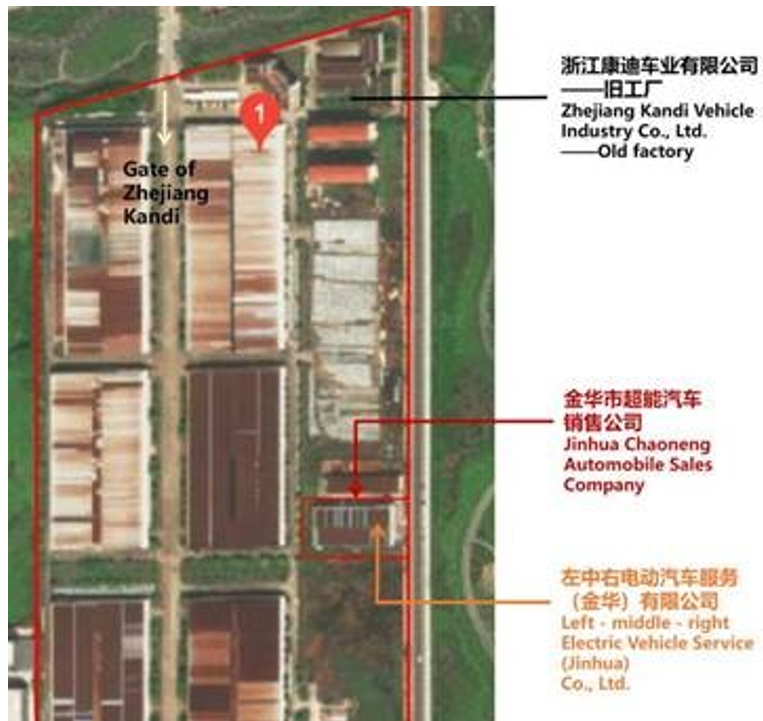

We Visited the Address of the Customer and Found Them Based in a Small Building Adjacent to a Kandi Factory

The “Customer” Had Kandi’s Name in Its Signage, Indicating That it is Part of Kandi

The addresses of the 2 companies are also almost identical, per the same corporate records. Both are based at plots “G-01-03 and G-02-01” in an industrial park in Jinhua City, per QCC records.

First, we viewed the customer address using Baidu maps. It shows a Kandi factory:

Then, we sent an investigator to the industrial park several months ago in order to confirm ourselves:

We asked the security guard working the Kandi gate about Chaoneng (the customer) and he had never heard of them.

However, we found a small building adjacent to the factory with a sign that named the purported customer as “Jinhua Kandi Electric Vehicle Chaoneng”.

The “Customer” Address Matched the Address of the Key Undisclosed Related Party Entity Involved Kandi’s Earlier Fake Sales/Subsidy Scheme

As noted above, the Chinese government had previously sanctioned Kandi and its JV partner over a scheme to collect illegitimate government subsidy payments through fake EV sales.

The entity used to generate the fake sales in that scheme was named “Left Middle Right, Co. Ltd” (浙江左中右电动汽车服务有限公司), and is based out of the exact same small building as Kandi’s new top “customer”.

Here is an overhead view of the Kandi factory and its purported customer/subsidy scheme entities.

Kandi appears to simply be recycling its old fake sales playbook (except this time the target is U.S. investors rather than the Chinese government.)

Kandi’s New Top Customer Shared an Executive with Kandi, Further Evidencing Close Ties Between the Two Companies

Further evidencing a long connection, a 2010 article detailed how an individual named Hu Yiheng, a Kandi employee, held a senior position at Kandi acting as “办主任” or “Office Director”.

Hu YiHeng[3] is the name of Chaoneng’s legal representative since June 17, 2013 and is also a 30% shareholder of Chaoneng, per corporate records through QCC.com:

In short, Kandi’s largest “customer” is (a) based at a Kandi factory; (b) shares a phone number with a Kandi subsidiary; (c) integrates Kandi into its own signage; (d) is based in the same building as another entity involved in a fake sale scheme for Kandi; and (e) shares or shared a key executive with Kandi.

We do not think sales to this entity are legitimate.

Kandi’s Second Largest Customer, Named “Kuke”, Accounts for 9% of LTM Sales. It Was Previously Wholly Owned by Kandi And Still Has an Unusually Tight Relationship

Kandi’s 2nd largest customer is Zhejiang Kuke Sports Technology Co., Ltd. (浙江酷客运动科技有限公司) (“Kuke”). The customer accounted for 11% of last quarter’s sales and 9% of Kandi’s LTM sales.

In an obvious link between the two entities, we found that Kandi previously owned Kuke up until 2008, right around the time of Kandi’s IPO, when it was sold to 2 private individuals.

In fact, corporate records on QCC.com still refer to the company as being a part of Kandi:

Kuke’s website still shows close ties to Kandi. The homepage features a large image of Kandi’s factory, and the company’s logo integrates Kandi with its corporate name. The site also features the brand name “Jasscol”, which is a registered trademark owned by Kandi. [Pg. 5]

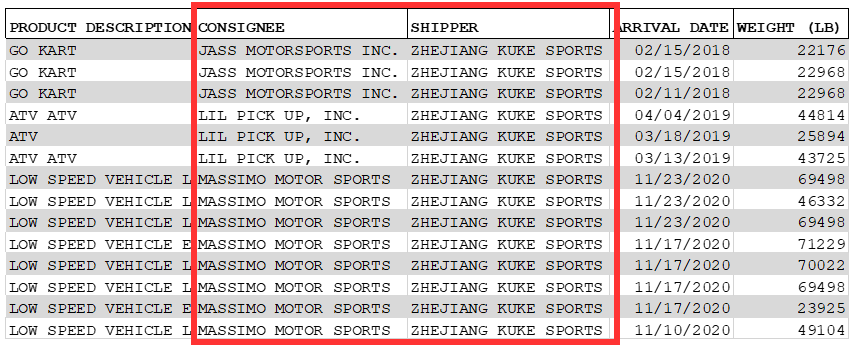

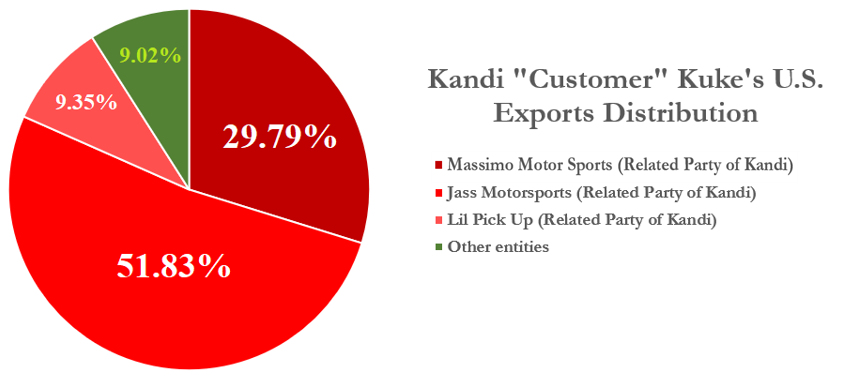

Export Records Show ~91% Of Kuke’s U.S. Exports Have Gone to Three Entities Based Out of Kandi America’s Addresses

In Other Words, Kuke is “Buying” From Kandi Then Selling Right Back to Obvious Undisclosed Related Parties of Kandi

Kuke’s website indicates that exports to North America comprise the vast majority of its business.

We reviewed export records through data aggregator Import Genius. Using the earliest records available, dating back to October 2017, we found that over 90.9% of Kuke’s exports to the U.S. by weight went to three entities:

(1) Massimo Motor Sports LLC

(2) Lil Pick Up Inc.; and

(3) Jass Motorsports Inc.

Here is a sample of the records, showing Kuke shipping to Massimo, Lil Pick Up, and Jass:

As we will show momentarily, state corporate records and litigation documents reveal that Massimo, Jass and Lil Pick Up are based out of addresses associated with Kandi America, making them clear related parties.

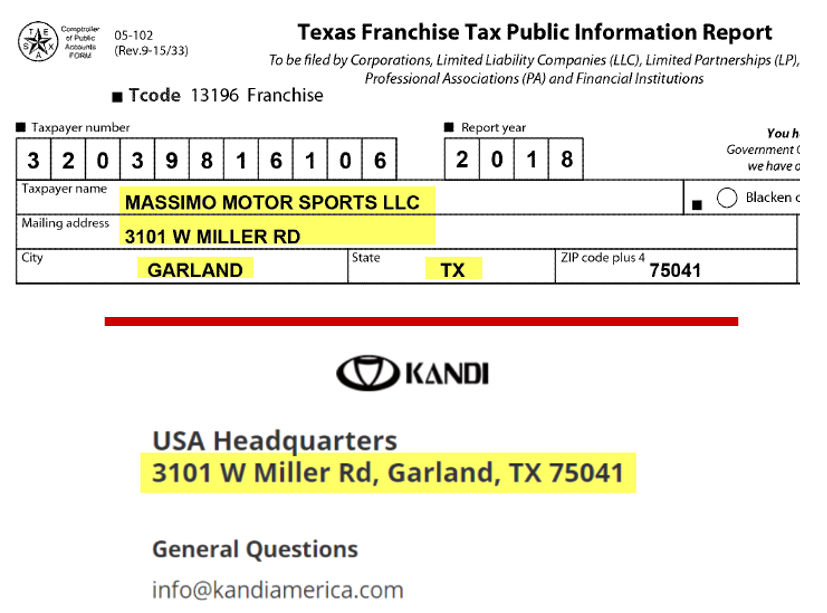

30% of Kuke’s Historical Exports Were to Massimo Motor Sports LLC, An Entity Based Out of Kandi America’s Headquarters and Owned by the Founder and Manager of Kandi America

Massimo Motor Sports is based out of Kandi’s U.S. headquarters in Texas and is owned by David (Jianxun) Shan, a founder and current manager of Kandi’s U.S. subsidiary.

Here are Massimo’s corporate records showing the address matching Kandi’s U.S. headquarters:

After Buying Kandi Product’s Through Kandi’s “Customer”, Massimo Motor Sports Then Sells Products Right Back to Kandi.

Massimo, An Undisclosed Related-Party Entity of Kandi America, Is Therefore Both a Top Customer and a Top Supplier Of/To Kandi.

We View This as a Brazen, Clear Circular Sales (i.e. Fake Revenue) Scheme

Once Massimo receives product from Kandi’s key “customer” Kuke, who does it sell its products to? Evidence shows that one of Massimo’s key customers… is Kandi.

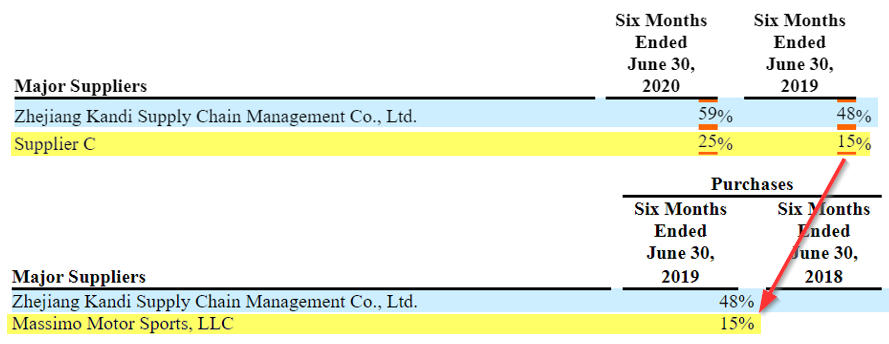

Kandi began redacting the names of its suppliers in late 2019. Using the same trick we used to unredact its customer names, we see that Massimo has been Kandi’s “Supplier C”, representing 25% of Kandi’s purchases in the first six months of 2020, and 15% in the same 2019 period.

To recap, Kandi sells to top “customer” Kuke à which then exports to Massimo (based out of Kandi’s U.S. headquarters) à then Massimo sells products right back to Kandi.

52% of Kuke’s Historical Exports Were to Jass Motorsports Inc., An Entity That Shared an Executive With Kandi and Was Based Out of the Exact Same Address As a Branch of Kandi USA

Moving right along, Kandi’s “customer” Kuke also exports to an entity called Jass Motorsports.

Jass Motorsports’ incorporation documents list a Rancho Cucamonga, California address that matches the address previously listed for a branch of Kandi USA. Both entities shared an executive officer as well.

9% of Kuke’s Historical Exports Went to Lil Pick Up, Inc., An Entity That Also Leases Warehouse Space at Kandi America’s Headquarters

We Have Photographic Evidence Showing Lil Pick Up Inventory Sitting in Kandi America’s Warehouse, Covered with a Tarp

Export records show that Kuke also regularly exports to Lil Pick Up, a company run by Renfeng Wang, who appears to share a business relationship with Kandi America Founder & Manager David Shan. [1,2,3]

Recent litigation records revealed that Lil Pick Up, LLC rents space at 3101 West Miller Road in Garland Texas, the headquarters for Kandi America. [Pg. 8]

The records even include a picture of Lil Pick Up inventory sitting in the warehouse covered with a tarp, dated from July of this year.

Kandi Has Consistently Booked Revenue That it Can’t Collect, A Classic Sign of Fake Revenue.

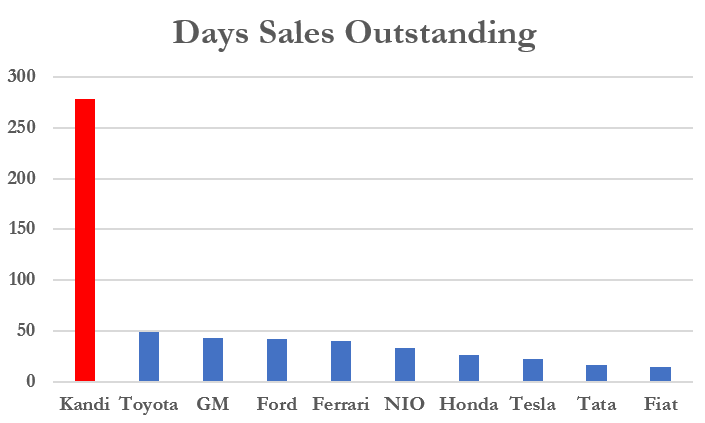

Kandi Had 278 Days of Sales Outstanding—5.6x Higher Than its Closest Competitor.

Kandi’s financial statements support our findings.

When most companies sell a product, they eventually collect the revenue and convert it into cash. This is especially true in the auto industry where cars are usually financed or paid for on the spot, before they are driven off the lots at dealerships.

Kandi seems to sell plenty of product, but then appears to have an incredibly difficult time collecting and converting it into cash.

The key measure of revenue collection is days sales outstanding (“DSO”), which measures the average days it takes to convert accounts receivable into cash. Kandi’s DSO in the previous June quarter was 278 days, 5.6x its closest auto manufacturing competitor, making it an outrageous outlier.

The company has attempted to justify its revenue collection failure by stating that its credit terms are “typically 180 to 360 days after delivery.” [Pg. 27] This doesn’t add up—very few industries allow customers to pay a year after they’ve received a product, and as seen above, automobiles clearly aren’t one of them.

In Kandi’s most recent September quarter, its trade receivables balance declined, but a new category of unusual receivable that has ballooned in its place. Kandi recorded a ~$51 million “loan to third party” as an “other receivable” in the most recent quarter, up from $13.7 million in the prior quarter.

This mystery loan did not seem to exist a year ago.

Most businesses generating $106 million in LTM revenue don’t suddenly loan $51 million to unnamed third parties without explanation. Once again, these major balance sheet irregularities are hallmarks of fake revenue. When factoring in the new mystery receivable, Kandi’s DSO in its most recent quarter is a whopping 429 days.

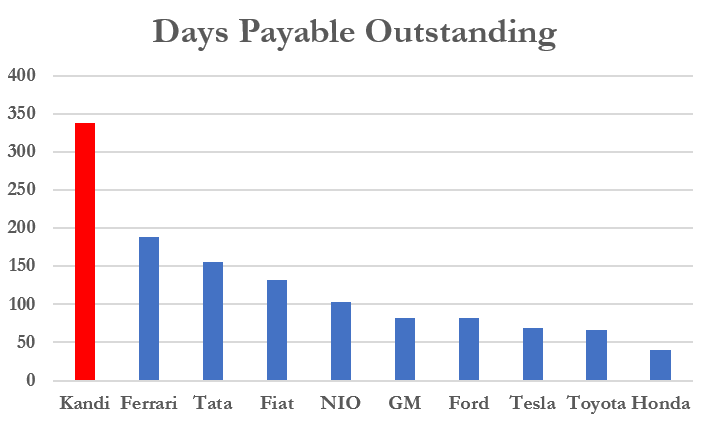

Kandi’s Payables Are Similarly Outrageously High at 338 Days Outstanding—1.8x Its Closest Competitor.

Are Suppliers Awarding Kandi the Most Generous Payment Terms in the Industry—Or Are Circular Sales Resulting in Fake Payables Along with Fake Receivables?

Typically, large, established market participants can demand better terms for amounts owed to suppliers due to their size and financial strength. Kandi is a fraction of the size of its larger auto peers and is generally a cash burning enterprise.

Despite this, Kandi’s financials indicate that its payment terms with suppliers are the most generous in the industry. Its Days Payables Outstanding (“DPO”) in the prior June quarter was 338 days, almost a full year.

That is 1.8x its closest auto manufacturing competitor, again making Kandi a clear outlier within its industry.

Why might this be the case? Another hallmark of fake revenue is when companies have large unexplained payables alongside large unexplained receivables.

Companies engaging in circular sales schemes may sell and later repurchase its own product, such as appears to be the case with Kandi and its relationship with Massimo, which we have shown above to be both an undisclosed related-party customer AND supplier of Kandi’s products.

The result of all this is the generation of fake revenue, fake earnings, and fake receivables/payables from/to the undisclosed related entities.

Some readers might be wondering—isn’t this all the sort of thing auditors are supposed to catch?

Kandi Has Had 3 Auditors in the Past 5 Years and Has Regularly Reported Weaknesses in Its Financial Controls

Frequent changes with a company’s auditor are another red flag for accounting issues.

Kandi has taken this red flag to another level. As described above, Kandi’s long-serving auditor Albert Wong & Co. was ejected from the industry following its well documented failures to catch clear signs of fraud at Kandi. The firm was dismissed as Kandi’s auditor in April 2016 and was replaced by BDO.

2016: In BDO’s first year as Kandi’s auditor, it identified 5 entire categories of material accounting weaknesses. These included material weaknesses in its disclosure of related party transactions. [Pg. 45]

2017: Kandi reported that it had instituted a plan to “remediate” the material weaknesses in its internal controls over financial reporting. [Pg. F-3] BDO’s audit opinion for the year said that the weaknesses had “not yet been fully remediated” as of the end of 2017. [Pg. F-3]

2018: BDO issued a clean audit opinion, [Pg. F-3] but then was subsequently replaced in October 2019 after BDO and the company “mutually elected not to continue the engagement”. BDO was replaced with Marcum Bernstein & Pinchuk, marking Kandi’s 3rd auditor in under 5 years.

So, how are things going with Marcum so far?

Two Months Ago, Kandi’s Current Auditor Marcum Was Handed a 3 Year Ban From Auditing Chinese Companies by the Public Company Accounting Oversight Board Due To Violating Audit Standards

Kandi’s current choice of auditor comes as no surprise. Marcum had already been disciplined and sanctioned by the PCAOB in 2019 violating rules on independence:

The 2019 order sanctioned Marcum in connection with its “China Best Ideas Investment Conference”, where it “endeavored to create a perception that the China Conference was an event featuring companies—some of which were Marcum issuer audit clients—that were high-quality investment opportunities”.

In September 2020, Marcum was handed a three year ban on auditing Chinese companies as a result of violating PCAOB rules and auditing standards.

Upon seeing this news, a reputable company would have likely fired Marcum immediately so as to disassociate from its soiled reputation. But on November 17th, six weeks after the PCAOB prohibition announcement, Kandi filed proxy documents seeking to reappoint Marcum as its auditor for the year.

It Hasn’t Just Been Auditors That Have Been A Revolving Door: Kandi Has Had 4 CFOs Over the Past 4 Years, Another Major Red Flag

Kandi’s Chairman/CEO has maintained his position since inception, but the company’s top accounting rank has seen extensive turnover.

2016: In November, Kandi’s CFO Wang Chen resigned and was replaced with Mei Bing.

2019: In January, Mei Bing resigned as CFO for “personal reasons” and was replaced with interim CFO Zhu Xiaoying.

2020: In May, Kandi appointed Jehn Ming (Alan) Lim as CFO, who is currently serving in the role, after Zhu Xiaoying was said to have “completed her responsibilities” as interim CFO.

Kandi’s New CFO: Prior Work History Included Working at (i) An Accounting Firm Ejected by the PCAOB and (ii) an Affiliate of Kandi’s Current Auditor

Of the two recent firms Kandi’s newly-appointed CFO worked at, one had its registration revoked by the PCAOB and the other is affiliated with Kandi’s auditor.

According to his biography in SEC filings, Kandi’s CFO worked at accounting firm Stonefield Josephson from 2006 to 2008. The firm later merged with Marcum, Kandi’s new auditor through its Chinese joint venture.

Lim later served at Kabani & Company from 2008 to 2012, per his biography in SEC filings. (He left this out of his LinkedIn profile for understandable reasons.)

Kabani had its registration revoked after PCAOB inspectors found a “wide-spread and resource-intensive effort” to alter documents in audit files in order to pass inspection in 2008:

Part III: Kandi Has Been “Launching” in the U.S. for 12 Years. We Expect its Efforts Will Continue to Sputter

Investors of late have been drawn to Kandi’s much-touted “U.S. launch”. The pitch by Kandi is that it aims to provide a low-cost electric vehicle that is attractive to value-oriented U.S. consumers.

Typically, companies expand to new markets after they have developed a strong presence in their domestic markets. Not the case with Kandi. The company operates in China, the largest EV market in the world, yet Kandi has reported a grand total of zero domestic Chinese EV automobile sales since the end of 2018. [Pg. 24, Pg. 32, Pg. 28, Pg. 22]

We spoke with several former employees of Kandi America to learn what is going on. We were told that the latest “launch” is nothing new. For years, the company has failed to deliver the number of cars and failed to sign up the number of dealerships necessary to succeed. Several referred to Kandi’s U.S. efforts as “smoke and mirrors” and openly speculated that it could be a strategy to lift its stock price.

Kandi “Launched” in the U.S. in 2008. Its First Batch of Cars Were Seized by U.S. Customs After Being Imported Illegally. The Launch Failed

New investors in Kandi may not realize that the company has attempted to launch in the U.S. multiple times over the past 12 years. Each attempt has sputtered.

Kandi began seeking to expand its presence to the U.S. as early as 2006. [Pg. 4] By late 2008/early 2009, the company introduced the “Coco” to the U.S. market, a golf cart-like vehicle that could reach maximum speeds of about 25 mph, but was intended for street use.

One major problem emerged: the initial vehicles had been imported illegally. Customs officials identified that Kandi and its distributor had misclassified the vehicles as ATVs. The EPA intervened, fined Kandi $40,000, and ordered the company to destroy or export the vehicles back out of the country.

The company eventually sorted out the problem and, in 2008, a smattering of U.S. dealerships attempted to sell the car, as shown in this example video:

Federal and state tax credits made the car as cheap as $865 for Oklahoma residents. (Joe Exotic from the popular Netflix series Tiger King, an Oklahoma resident, purchased a Coco.) But the company eventually stopped reporting sales of the Coco after 2012 and the car quietly disappeared from the market.

We Asked Kandi’s 2008 U.S. Distribution Partner About the Vehicles: “They Didn’t Run, Every Single One Broke”

To learn what happened with the company’s original U.S. launch, we spoke with a founding partner of Kandi’s U.S. importer and distributor for its 2008 Coco release.:

“We brought in our first 200 vehicles and had nothing but problems. They didn’t run, every single one broke…The prototype was excellent but when they started shipping these vehicles nothing but problems. Engines weren’t working, batteries were burning up.”

“I had three big distributors that took in the first allotment of cars. I had them set up to buy 2,000 vehicles in the first year from Kandi. We had the documentation but from what I understood they forged it, they faked it……Customs got them and said if you don’t get these cars out of the US then you’re going to be fined and they will be destroyed.”

We asked how many of Kandi’s cars had issues when they finally made it into the country:

“Every single one…I’m a salesman and I was running round the country like a mechanic. I was flying all around the country trying to fix these things and it just got to the point ‘I’m out, I can’t do this anymore… I left because I the whole process was horrible, too secretive, a lot of side deals I didn’t know about. I said you guys handle it, I’m out.”

Kandi Tried to Launch U.S. Operations Again in 2018, But Plans Were Delayed

After the failure of the “Coco”, Kandi planned another U.S. launch in 2018.

Kandi bought a U.S. company in early 2018 known for sales of ATVs and recreational vehicles, then renamed it Kandi America. In June 2018, Kandi formally announced its expansion into the U.S. market, starting with 3 prototype vehicles. (A Model K22 and 2 Model EX3s.)

In August, Kandi held a launch event to showcase its cars to dealers in the hopes of developing a distribution network. We spoke with a former employee who worked for the company at the time, who told us:

“They had a press release at a hotel in Frisco and they set up the cars in a nice display room and Chamber of Commerce folks from Garland came and there was all this big to-do. And I thought great it’s going to happen. But from that point, no cars and no nothing. Nothing ever showed up and nothing ever happened”.

We asked if any dealers signed up:

“No not to my knowledge. To my knowledge we never had anybody to invest and go forward with that. And luckily so, because they still wouldn’t have any vehicles to sell.”

On a conference call at the time, Kandi’s Chairman/CEO had alluded to U.S. sales kicking off near the end of 2018, but that didn’t pan out.

Kandi Tried a U.S. Launch Again in 2019, But Those Plans Were Again Delayed

In January 2019, Kandi’s Chairman/CEO told Bloomberg in an interview that the company planned to ship cars to the U.S. that year.

In February 2019, Kandi announced the National Highway Traffic Safety Administration (“NHTSA”) had “approved” its two electric vehicle models, claiming:

“The NHTSA approval is an assurance that Kandi’s two EV models conform to NHTSA standards and are registered in the U.S.”

The stock soared over 40% on news of the government approval. Yet, despite the claims, we found that the NHTSA doesn’t actually approve cars. Instead, manufacturers self-certify. Per the NHTSA spokesperson we contacted (emphasis added):

“By Federal law all vehicles sold in the U.S. must be certified by the manufacturer as meeting all applicable Federal Motor Vehicle Safety Standards (FMVSS). NHTSA does not certify vehicles prior to sale – doing so is the manufacturer’s responsibility..”

In either case, investors likely expected the news would lead to an imminent U.S. sales ramp. That didn’t happen.

Kandi’s Latest 2020 U.S. Launch Efforts Appear to Be Delayed

Former Kandi America Employee: “If You Never Produce the Product Then It’s Just Smoke And Mirrors…”.

In July 2020, Kandi once again announced the “formal launch” of its vehicles in the U.S., and held a virtual launch event in August to re-introduce the cars.

So far, several reviewers have tested the cars, and several dozen vehicles are sitting in the company’s Texas lot. The company received EPA certification for its vehicles this month, clearing the path to potentially sell vehicles.

Kandi targeted deliveries by year-end, but the company now expects to begin deliveries in early 2021, according to a recent reviewer that spoke with the company.

The company seems to be struggling to find dealer distributors. A November 23, 2020, Barron’s article identified only one authorized Kandi EV dealer, a Denver pharmacist who approached the company about purchasing an EV and then decided he wanted to invest $30,000 to open his own dealership.

We spoke with a former employee this month who keeps in touch with Kandi. They described how the company has continuously struggled to bring in enough cars and to find dealers to sell them:

“I was talking to a gentleman there (at Kandi America) the other day and he said ‘still trying to get the cars here’…what’s crazy is we’re almost in 2021 and I was there in 2017, waiting and waiting and we’re still waiting and still in exact same holding pattern…

“…if you never produce the product then it’s just smoke and mirrors as far as I’m concerned.”

Kandi’s Chairman/CEO Expressed Uncertainty on Its U.S. Launch “The U.S. Market Is Not Familiar with Our Products”

Kandi is Recognized in China However, and Has a Reputation for Poor Quality

Kandi’s own Chairman/CEO didn’t seem to have much confidence in the reception of its cars in the U.S. market, expressing uncertainty in a recent Barron’s interview:

“We are not very certain about it,” he says. “The U.S. market is not familiar with our products.”

Domestically in China, Kandi is somewhat known, but not for the right reasons.

Multiple Chinese media outlets reported that historical customers had batteries fail after mere days, while other customers complained that the company refused to honor warranties after various product failures. [1,2,3,4]

Two Years Ago, Angry Kandi Customers Held a Protest at Kandi’s Headquarters, Complaining About Shoddy Vehicles and the Company’s Failure to Honor Its Service Warranties

A December 2018 news article reported that more than 10 buyers of Kandi’s EVs held a protest at its headquarters in Hangzhou because Kandi refused to provide after-sales service, despite having warranties.

Protesters brought banners to Kandi’s headquarters, which read:

“The quality of Kandi EVs is severely below standard, Kandi cheated the government for subsidies and defrauded customers; we want our rights exerted, the manufacturer [Kandi] needs to take responsibility for after-sales service”.

We believe this may be one reason why the company has reported no domestic auto sales in China in the past several years.

Despite the Lack of Vehicle Sales to U.S. Customers, Kandi Appears to Be Booking Sales of Its U.S. Vehicles Through an Undisclosed Related Party Anyway

Oddly, the company appears to be booking sales from its auto exports to the U.S. despite acknowledging that sales to U.S. customers have not yet begun. [Pg. 16]

Kandi has reported $878,000 in EV Product (i.e. vehicle) sales since Q4 2018, all of which have been exports from the company’s Hainan factory, per Kandi’s SEC filings. [Pg. 24, Pg. 32, Pg. 28, Pg. 22]

The company has not announced entering any new markets aside from the U.S., so we can presume that all of the export sales are to the U.S. So how is the company booking years of revenue from sales that haven’t happened?

Normally, companies that manufacture products will ship the products to its foreign subsidiary then sell the products to end users. Not the case with Kandi apparently.

We checked import records through ImportGenius and found that Kandi’s Hainan factory has been shipping cars to Massimo Motor Sports LLC. This same entity turned up in the section above about Kandi’s undisclosed related-party customer relationships.

As a reminder, Massimo Motor Sports is based out of the Kandi USA headquarters in Texas and is owned by David (Jianxun) Shan, a founder and current manager of Kandi’s U.S. subsidiary.

In sum, Kandi appears to be booking illegitimate U.S. sales to an undisclosed related party before formal U.S. customer sales have even begun.

Part IV: Kandi’s Rideshare and Battery Swap Initiatives

In addition to Kandi’s much-anticipated U.S. launch, the company has repeatedly touted plans to (a) sell up to 300,000 vehicles domestically through a rideshare partner; and (b) roll out domestic quick battery swap stations to make EV charging fast and efficient.

Investors have viewed both endeavors with excitement, but a quick review shows both ventures are either devoid of substance or hopelessly behind competitors.

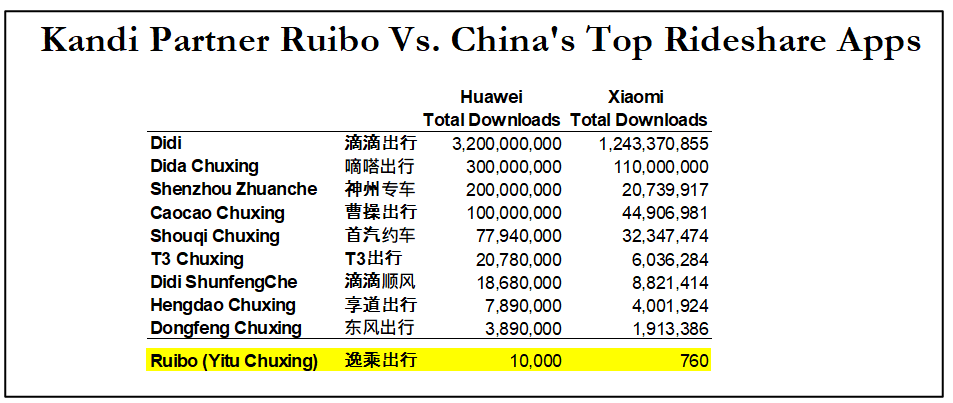

Kandi’s Rideshare Partner Ruibo Has Virtually No Presence in a Market Already Dominated by Didi And Other Rideshare Apps

In January 2019, Kandi announced an agreement to join forces with rideshare company Ruibo to deliver 300,000 cars to the Chinese rideshare market in 5 years.

The company has repeatedly indicated that it may deliver hundreds of thousands of EVs to the venture in the coming years, an exciting prospect for investors. (1,2,3,4)

Progress has been slow. Kandi formally established the rideshare joint venture with Ruibo in October of this year.

China’s rideshare market is huge, but much like the U.S., it is controlled by top players. In the U.S., the market is dominated by Uber and Lyft. In China, ~90% of the market by revenue is dominated by Didi, (1,2) with the next closest competitor commanding only about 4%.

Kandi has chosen to partner with Ruibo, a company that doesn’t even appear on lists of the top 77 or top 50 rideshare apps in China.

On China’s most popular app stores like Huawei and Xiaomi we see that Ruibo’s downloads barely even register.[4]

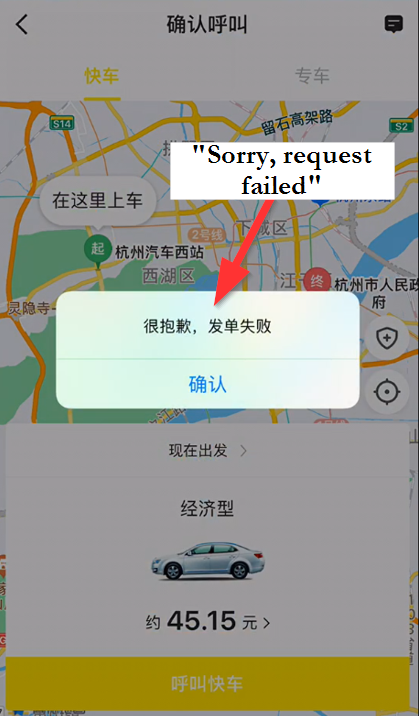

We had a local consultant test Ruibo in major cities Beijing, Hangzhou, Jinhua and Xiamen. The app failed to find a driver each time. Here is a video of our investigator attempting (and failing) to hail a ride in Hangzhou, where Ruibo is headquartered, during normal daytime hours.

We reached out to customer service for help. The rep suggested we try to hail a ride through a separate app called Gaode Maps, which is an aggregator of multiple platforms (i.e. Didi, Ruibo, and other rideshare apps). In other words, they suggested we use a competitor.

We followed up by asking if the platform had really been launched yet and received no reply.

On Kandi’s most recent Q3 2020 investor call, CFO Alan Lim was asked about the 300,000 rideshare vehicle estimate and essentially walked the claim back, referring to the number as really just a conceptual goal:

“(It) is rather an idea of the program but not entirely or necessarily means that there will for sure put 300,000 EVs to the market. So how many EVs will be supplied to the market at the end of the program? We are not 100% sure. But the so-called 300,000 is sort of like a slogan or an idea.”

We conclude that Ruibo is mostly vaporware, with slim to no shot at competing in China’s intensely competitive rideshare market.

Kandi’s Battery Swap Program Is Well Behind Competitors Such As Nio, BJEV, And Even Its Own Partner Geely

China’s domestic electric vehicle industry has heavily invested in battery swap stations in order to minimize charging wait times. Major EV manufacturers that dwarf Kandi in size and scale are well along the path.

Manufacturer NIO, for example, has already completed its one millionth battery swap and had – at the end of last year – swap stations in 51 cities, including Beijing, Shanghai and Guangzhou.

Manufacturer BJEV has also secured a broad footprint with 160 stations across the nation. Alibaba backed Xpeng Motors launched a battery leasing service in September 2020. Kandi’s partner Geely also has a competing service, having launched its first battery swap station in October 2020 with plans to expand aggressively.

Kandi has thrust itself into this competitive part of the market as well. In January 2018, Kandi acquired battery swap technology company Jinhua An Kao (“An Kao”) for approximately $4 million in cash and ~2.96 million shares (valued at $20.7 million at the time). Currently the company has one pilot charging station.

Kandi Lacks Enough Vehicles on the Road for a Battery Swap Program to Make Sense

As detailed above, Kandi has reported no domestic sales of EVs in the past several years outside of its minority stake in an affiliate entity with Geely.

The company is manufacturing model K23s in its Hainan facility for inventory, though until recently it lacked a sales certificate to be able to sell the cars itself, according to former employees we interviewed.

Despite a lack of cars on the road needing battery swaps, Kandi announced on November 2, 2020, that it aims to list its battery swap subsidiary on Shanghai’s STAR Exchange and it has already engaged CITIC to help it IPO. We do not envision this being a successful endeavor.

We Have 25 Questions for Kandi’s Management

Through the course of our research we contacted the company asking several questions about its financials and product initiatives. We received no response, so here are the questions that we think investors deserve the answers to:

- SEC prosecutors alleged in a complaint that Kandi’s Chairman/CEO participated in a scheme to inflate the price of its stock, along with several individuals that took Kandi public as part of its original reverse-merger IPO. How do you respond to these allegations?

- Kandi’s long-serving auditor, Albert Wong & Co., was ejected from the industry by the Public Company Accounting Oversight Board (“PCAOB”) over its failure to detect clear evidence of misappropriation by senior management of Kandi, along with undisclosed related-party transactions. Has management ever responded to these allegations? If not, how do you respond now?

- In 2019, Chinese media located a car lot with thousands of Kandi vehicles apparently sitting unused and deteriorating. Were these cars manufactured as part of the well-publicized subsidy scheme? What is your explanation?

- Kandi has reported no sales to its JV/affiliate with Geely in recent quarters. What role does Kandi have, if any, in the manufacturing and sales of the Maple 30x?

- Despite the evaporation of revenue through the JV with Geely, Kandi’s revenue remained relatively flat due to the dramatic increase of sales to “Customer A” and “Customer B” (i.e. Jinhua Chaoneng Automobile Sales Co. Ltd. and Zhejiang Kuke Sports Technology Co., Ltd.) What products are you selling to these entities, and how do you explain the sudden uptick in sales to them?

- Why does Kandi’s top customer (Chaoneng) representing 55% of LTM sales, share a phone number with your subsidiary? Why is it based at the same address as your own factory, and with signage indicating it is a Kandi company?

- Kandi’s second largest customer (Kuke) represented almost 9% of LTM sales. But export records show that ~91% of Kuke’s U.S. exports go directly to entities based at Kandi’s U.S. warehouse locations. How do you explain this?

- One of Kuke’s export entities, Massimo Motor Sports, is owned by David (Jianxun) Shan, founder and manager of Kandi’s U.S. subsidiary. How do you explain Kandi’s product sales to this obviously undisclosed related party entity?

- Kandi’s filings show that Massimo sells product right back to Kandi; it has been reported as supplier of up to 25% of Kandi’s goods in recent periods. How do you explain these apparently circular sales?

- Why is Kandi’s Days Sales Outstanding (DSO) 5x-6x higher than peers? Will you name the counterparties to these uncollected receivables?

- In its most recent quarter, Kandi reported a “loan to third party” of ~$51 million as an “other receivable.” This is a massive loan, yet Kandi has not disclosed the borrower, despite its obligations to disclose material loans. Who is the borrower?

- Why is Kandi’s Days Payable Outstanding (DPO) almost 2x higher than your closest peer, and over 3x higher than the median? What are the names of Kandi’s top suppliers?

- Kandi has had 3 auditors in the past 5 years. Why the revolving door?

- Kandi has had 4 CFOs in the past 4 years. Why the revolving door?

- Kandi’s current auditor, Marcum, was recently handed a 3-year ban from auditing Chinese companies from the PCAOB. Will Kandi continue to attempt to reappoint Marcum as its auditor, as indicated by your recent proxy filing, or will the company choose a credible auditor?

- We spoke with a former distribution partner that worked on the company’s 2008 U.S. launch. They said the prototype vehicles worked well, but every single customer vehicle broke down. How can consumers be sure that quality has improved?

- Why has Kandi not reported any domestic sales outside of the Geely JV in the past several years? A former employee we spoke with said Kandi did not even have a sales license up until late this year. What happened? What is standing in the way of restarting domestic EV sales?

- How is it possible that Kandi has booked EV Product sales to the U.S. for several years when EV Product sales to U.S. consumers haven’t even begun, per the company’s own admissions?

- An auto reviewer recently reported that the company now aims for a Q1 2021 launch in the U.S. Are sales to U.S. customers delayed once again?

- Export records show that Kandi has shipped its Hainan EV Products not to Kandi, but to undisclosed related party Massimo Motor Sports. Has Kandi been recording the shipments of EV products to this entity as sales?

- David (Jianxun) Shan is founder and manager of your U.S. subsidiary. Shan controls an entity called Miller Creek Holdings which owns the Kandi America headquarters. Kandi leases the facility from Miller Creek, yet does not record the lease payments as related-party transactions. Why not, given the company’s obligations to disclose all related party transactions?

- How do you expect to sell 300,000 vehicles through your relationship with rideshare app Ruibo when Ruibo has virtually no users in a market already dominated by Didi (along with dozens of other competitors)?

- How do you expect your battery swap program to generate any interest when Kandi has virtually no vehicles on the road in China to swap batteries into?

- From 2014-2018, Kandi reported that ~75%-83.5% of EV Parts sales consisted of battery packs. The company stopped reporting the percentage. What percentage of EV Parts sales from 2019 and onward were battery packs?

- Litigation records show that Kandi previously purchased batteries from Jiangsu Tianpeng Battery Co., Ltd (江苏天鹏电源有限公司), and the company recently announced a deal with CBAK Energy for its batteries. Does Kandi manufacture its own battery cells, modules, and packs, or does it simply resell them from others?

Conclusion: How Does A Company Like Kandi Keep Getting Away With It?

Many investors assume that auditors and regulators protect investors from fraud. Such trusting, well-meaning investors might wonder: How does a company like Kandi trade on a premier U.S. exchange without any regulatory consequence when:

- Kandi was brought public by a promoter charged with fraud by the SEC over allegations of conspiring with the (still) Chairman/CEO to manipulate its stock price.

- Kandi was fined by the EPA for illegally importing its very first shipment of vehicles into the country.

- Kandi’s long-serving auditor was ejected from the industry over its failure to catch obvious signs of extensive fraud at the company, and its latest auditor has been banned from auditing Chinese companies by the PCAOB.

- Kandi was sanctioned by the Chinese regulators (but not U.S. regulators) for a scheme to generate false sales through undisclosed related party transactions in order to collect illegitimate subsidies.

- Kandi admitted that its financials were false due to a failure to recognize related party transactions, and had to restate 3 years of financials.

- Kandi displays obvious hallmarks of fake revenue including a key “unrelated” customer based at its own address sharing its own phone number, having massive uncollected sales, and serial CFO/auditor turnover.

In the end, many Kandi investors won’t read this report, or will simply dismiss our findings outright because we are betting against the company.

The company will likely issue some sort of press release declaring everything we say false and misleading, as they always do, while ignoring all or the vast majority of the questions we’ve raised. They may throw in a legal threat and a token share buyback/insider purchase for good measure.

Some investors will believe management blindly—after all, these are executives at a large, public company trading on the well-respected NASDAQ exchange.

Such investors won’t realize that virtually all of this report was constructed from public records, and they can simply click through the hyperlinks we’ve provided to recreate most of our thesis in about an hour.

If regulators do decide to pursue a case, they will likely be stonewalled by the Chinese government, and may just throw their hands up in the end—because what’s the point of running a challenging international investigation just to win a default judgement that can’t be collected from overseas defendants anyway?

If a regulatory action does occur, it often takes 3-5 years, because 5 years is typically the statute of limitations for cases of fraud, and regulators like to investigate near the deadline before making a decision on whether to prosecute.

In the interim, many investors will view the lack of a regulatory enforcement as a vindication of the company. And a company like Kandi only needs to fool some of the people all of the time. The company has raised $160 million from U.S. capital markets in November 2020 alone, and we have no doubt it will attempt to perpetually sell stock.

And for us, we’ll keep calling it out as we see it. Best of luck to all.

Disclosure: We are short shares of Kandi Technologies (NASDAQ:KNDI)

Legal Disclaimer

Use of Hindenburg Research’s research is at your own risk. In no event should Hindenburg Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Hindenburg Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in all stocks (and/or options of the stock) covered herein, and therefore stands to realize significant gains in the event that the price of any stock covered herein declines. Following publication of any report or letter, we intend to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial recommendation, conclusions, or opinions. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Hindenburg Research is not registered as an investment advisor in the United States or have similar registration in any other jurisdiction. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Hindenburg Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Hindenburg Research does not undertake to update or supplement this report or any of the information contained herein.

[1] We are still very much short Nikola. For readers inclined to maintain social distance during the pandemic we recommend visiting Nikola’s under construction “factory” which, after 4 months, appears to still be a large, empty plot of land in the middle of the Arizona desert.

[2] Unlike Kandi’s other sales, these were fully disclosed as being related party sales, whereby Kandi would contribute EV parts to the venture, and the JV would complete assembly of the vehicles.

[3] Hu YiHeng shares a surname with the Chairman/CEO of Kandi, but we were unable to determine whether there is also a familial relationship.

[4] Note that these metrics include all downloads on every device through the history of the app, explaining how the download metrics (for Didi specifically) have managed to dwarf the population of China over time.

94 thoughts on “Kandi: How This China-Based NASDAQ-Listed Company Used Fake Sales, EV Hype to Nab $160 Million From U.S. Investors”

Comments are closed.

Your analysis is valuable but also, similar to KNDI’s practices, deceptive. The timing, viciousness, picking the rhetoric that makes your story viable and most importantly your intent are murky. You should have been present at their quarterly call and raised these concerns. I would trust the company more because they are looking for a positive future into entering the US Market, while you’re looking negatively into shorting the stock in order to making couple bucks.

Please enlighten the rest of us here – What is the “timing” you are referring to? Just which part of this report is “vicious”? Since when does laying out a comprehensive fraud report equate with “picking the rhetoric”? Thus, do you care to provide additional insight, since you obviously seem to be a devoted Kandi investor? You remind me of the Nikola flock who were ready to fight the truth to their dying breath.

The reason why its a silly report is that it doesn’t show any information that is valuable, it takes information and makes judgment calls without knowing what is going on. Kandi has to import cars to sell them. They have US subsidiary companies they do this through, since Kandi has a shell of operations in North America. It is not a surprise to see Massimo Motor Sports as a sales brand to import with, this is a company they are partnering with to get a Kandi footprint.

Basically, the report seems to be a lot of hyperbole and lots of judgments based on 25% truths. Sure, they are importing the cars under these brands. The “viciousness” is with regards to the huge judgments the author is making, without their real knowledge of what these transactions are about. I’ve imported goods, sometimes it has to go through a number of names before the product is in North America. This is normal business, yet the author is stating something shady is going on, without evidence.

I see this as a slimey line of work. But somebody has to do it. As long as what you report is true and just, I cant find an argument against it. I have been financially hit by sick players doing this over trivial claims reported at strategic times and blown way out of proportion. But when its truely crook exposures. I consider it a service. So keep doing what you do in a thorough and documented way and I will continue to be a fan. Thank you for this.

With benefit of hindsight, this report does not stand the test of time. PRC subsidy regulations allowed Kandi’s battery swap business model and the Chinese gov’t paid all of Kandi’s qualifying subsidies after the investigation (of ALL EV operators) was completed. SUBSEQUENTLY Kandi’s EV entity was granted a rare and valuable manufacturing license. SUBSEQUENTLY to that, China’s leading investment bank, CITIC, after more than a month of due diligence, agreed to underwrite Kandi’s IPO listing of its Smart Battery Exchange subsidiary on the STAR Technology Exchange. (Pending) And most recently the gov’t controlled China Agricultural Bank provided a $76 million line of credit to operators in the Ruiheng car share cooperative with Jingpeng. This is a new carshare initiative in tier 4/5 cities of rural China where Didi does not operate. This is a lot of third-party credibility being conferred on Kandi subsequent to the events in this report.

Throughout the events in this report, Kandi had a 50/50 JV with China’s largest private carmaker, Geely. Many of the claims in this report are actually against the JV, which means they are charges against Geely which was the financial manager of the JV under the agreement between the two parties. Kandi handled day-to-day operations and Geely’s auditor produced the financials which were the majority of Kandi’s financial reporting at that time. While the JV is currently owned 78% by Geely and 22% by Kandi, the close relationship between the two companies continues, and the JV, now renamed FengSheng, is expected to be an important component of Geely Technology Group, its ‘city car’ flagship involving QBEX and ride sharing (autonomous) in the future. Geely offers further credibility to Kandi’s standing in China.

As for financials, related party transactions, which were always footnoted, are now classified as separate revenue items on the face of the P&L. Those highlighted in this report are not included since they are not related party transactions. Re the audit firm, Kandi specifically chose Marcum because they were PCAOB compliant. They had left Wong to use BDO because it was more credible to the US market and regulators, and only left BDO because they were not PCAOB compliant. No good deed goes unpunished, as they say…

The SEC investigated all these related party matters five years ago and in a rare move issued a ‘no action’ letter when they were satisfied that Kandi’s financial statements fairly reflected its financial positions WITHOUT RESTATEMENTS. The short-sellers have never accepted the SEC’s findings and continue to make the same claims herein that were cleared five years ago by the SEC. In addition, private lawsuits regarding the same financials have not been successful in US courts. Kandi’s financials have been so thoroughly investigated and cleared that the motivation to continue to make such claims must be for the shock value of the headline since the SEC and US courts have determined there to be no fraud, false statements or any need to restate.

Also note that KNDI has an option with Geely allowing KNDI to acquire a larger percentage of FengSheng (their JV with Geely) in exchange for Geely taking a position in KNDI. At this writing the two parties are still negotiating this possible future transaction which expires on 3/31/21.

Kandi also has a cooperation agreement with State Grid, China’s state-owned electric system, for possible future affiliations in the area of battery exchange and recycling. Expansion of this business line is the basis for the announced IPO, along with new contracts for small EV motors being used in hoverboards and self-balancing scooters being sold in the US and elsewhere.

It remains to be seen whether Kandi can successfully market small EVs in the US, but they intend to try to be the lowest cost option for Americans who want to drive EVs. Kandi’s off-road vehicle business continues to grow. This legacy business has carried Kandi though the long subsidy shutdown and should be able to expand beyond only the US market in the future.

Hindenburg is entitled to its opinions, but regurgitating claims that have long since been investigated, adjudicated, and determined to be unfounded just for the shock value to profit from the drop is what we are dealing with once again, all these years later.

Seriously? Did you even read the analysis?

As someone who understands how imports can be, and the names imports sometimes trade hands to get here, I am fully aware of the holes in this analysis Zimbabwe.

I’m not promoting Kandi cars, I want to see them and see what they look like after delivery. This piece is basically just anti-China, not anything to do with the cars. We’re aware that Kandi has had some very cheap, low quality products in the past (some of the models they bash are over a decade in age), I’d like to see the new crop of cars and see how they can compete with the vastly overpriced North American makers like Tesla.

This report, frankly, doesn’t show much. It lists a lot of trade records and then draws conclusions based on some basic facts that are kind of outlandish. Companies “sell” products to themselves all the time.

Hindenburg research, is just trying to pass “fake news”, for the purposes of manipulation. They are just shorting the stock. To those who don’t know, shorting is the opposite of conventional buying. In shorting, you need the price of the stock to go down. So a “shorting firm”, spreads fake news. The truth is, Kandi has cars sitting in Dallas Tx. Readying for delivery. The US DOT just recently passed these cars on the safety testing. Many states have already granted or recognized these cars for there EV rebates. That’s an additional rebate added to the 7.5k Fed. Rebate. They, Kandi, has two versions of each model. One slow 25mph, and the other, a high way speed version. The slower version has NEV before the “k” in each model. So, if you’re interested in traveling at high way speeds. Make shore you order the correct variant of the preferred model.

That’s an additional rebate added to the 7.5k Fed. Rebate. They, Kandi, has two versions of each model. One slow 25mph, and the other, a high way speed version. The slower version has NEV before the “k” in each model. So, if you’re interested in traveling at high way speeds. Make shore you order the correct variant of the preferred m

Love all the investigative reporting to help investors steer clear away from these fake publicities and hyped sales numbers. Your research is truly invaluable. Keep it the great work!

Thank you for keeping the investing community well informed on this Chinese scam. I am shorting Kandi via a PUT option and hope their ”candy” turns sour to them. These people should be delisted immediately from our markets.

Again, Manuel, where is the evidence? All we’re seeing are import sheets with vehicles brought in, largely during November, just before deliveries to customers occurs. Imports commonly go through several names or companies before it ends up in the hands of a customer, that isn’t a scam. Furthermore, reporting about a completely unrelated product that flopped years ago where cars sit in Chinese junkyards isn’t proof of the current situation. Its basically throwing mud. I’m not interested in propping Kandi up, they will fall or fail on their own accord, but this reporting is mostly junk. It is just a bunch of import sheets showing some cars being shipped, and being imported through various brand names. That isn’t a scam, and just because its Chinese doesn’t make it bad. I’ll be waiting for the actual cars to arrive, see what reviewers get out of them, and we will see what they are made of when it actually gets into the hands of customers.

So, basically, Yugo-meets-Nikola! Great, comprehensive research yet again, kudos. You are earning every penny on your shorts.

Many thanks! I thought a Kandi Coco was much newer and appeared to be ideal. I was waiting for that “new” Kandi model to reach the U.S.; but now I read that it is a 2008 model, and see hundreds of them rusting away in a Chinese field- What A Shock!!! I planned to spend lots of money for a Coco. Now- no way! Thanks for saving me a bundle of cash.

I’m a long term shareholder in Kandi (and in Tesla) and you have some interesting points, but most of it is just ridiculous FUD. But I have learn how US capitalism working and you are on top of it.

1. What happened in 2008 has nothing with to do with today.

2. You have obviously not look into the deal between Kandi and SC Autosports.

3. Also you should look more on the Kandi – Geely deal.

Kandi has a long history of pump/dump-attacks from short-sellers, so your “investigation” is nothing new.

But I thank you for helping us putting Kandi on the map.

It is positive long term and also give us shareholders a short term buying opportunity.

pictures are from Baidu, Hindenburg never went to Kandi site. How did they trace former employees, where is the telephone recording ? a lot of allegations no real proof, only interested in lowering stock to make money, timing very suspicious. Hindenburg hiding their location

Iit’s normal Wall Street Capitalism.

Shortsellers Enrichment Committe (SEC) never care about shareholders, so Hindenburg can do it again and again.

These rascals! Love these reports, keep them coming. Shows how much corruption and greed is out there.

So.. you took a short on Kandy before publishing this?

Is that legal? I mean… How could it be legal?

I think 80% information in the report was already explained by Kndi before with SEC files. For example, Daily sales outstanding issue was explained in one SEC file mainly due to kandi normally do not sell directly to customers and they rely on their partner who again rely on chinese government subsidy payment sometime have long delay. Kandi extend the accounts Receivable Policy range 210 to maximal 720 days.

I guess HINDERBURG already covered their short position as checked current Kndi short volume dropped now to historical low.

I assumed HINDERBURG gained good profit this time. But have you thinked about retail investor, why you dont ask questions in quarterly finance meeting.

I checked some KNDI America K27 review video, for that low price and the reviewed quality and performance e.g. 6K USD, the car is good choose for some people, e.g. students, or working class or some middle class.

At least Kndi mission is positive, sell affordable EV to help the environment and less rich people while HINDENBURG mission is gain profit while very often hurt retail investors.

very nice article because you are hero