We have been aware that Indian securities regulator SEBI has been grappling with how they are going to respond to us, a U.S.- based research firm with no presence or operations in India, after we presented overwhelming evidence in January 2023 of why we believed Indian conglomerate Adani Group was operating “the largest con in corporate history”.

We had anticipated fierce opposition to our report before we ever published it, regardless of how comprehensive and truthful our body of evidence was.

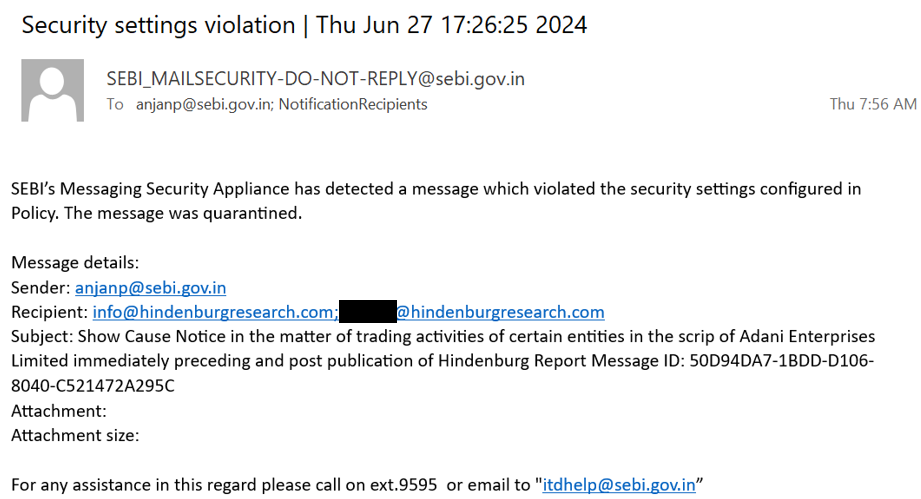

On the morning of June 27, 2024, our firm received a bizarre email, ostensibly from SEBI, alerting us that SEBI had flagged its own message to us that we never received as an apparent security risk, and that the regulator had “quarantined” it for its own safety.

This, at first, struck us as a possible targeted phishing attempt. It was only later that day that we received another email, again ostensibly from SEBI, with a ‘Show Cause’ notice, a letter from the regulator outlining suspected violations of Indian regulations.

Today we are sharing the entirety of this notice, frankly because we think it is nonsense, concocted to serve a pre-ordained purpose: an attempt to silence and intimidate those who expose corruption and fraud perpetrated by the most powerful individuals in India.

Background: Basics On Our 106-Page Adani Report’s Findings And The 40+ Independent Media Investigations That Corroborated And Expounded On Our Work

To This Day Adani Hasn’t Directly Addressed The Findings From Our Research Or From Dozens of Media Investigations, Instead Offering Deflections And Blanket Denials

For context, our original report was 106-pages, with 32,000 words, and included 720 citations, collectively detailing evidence that Adani “engaged in a brazen stock manipulation and accounting fraud scheme over the course of decades.”

The report provided evidence of a vast network of offshore shell entities controlled by Gautam Adani’s brother, Vinod Adani, and close associates. We detailed how billions were surreptitiously moved through these entities, into and out of Adani public and private entities, often without related-party disclosures.

We also detailed how a network of opaque offshore fund operators surreptitiously helped Adani evade minimum shareholder listing rules, citing numerous public documents and interviews to substantiate the allegations.

Shortly after our report, in August 2023, “Big-4” auditor Deloitte resigned from its role as statutory auditor for Adani Ports, citing undisclosed related-party transactions flagged in our report as the basis for a qualified opinion that accompanied its resignation.

Following our initial Adani report, at least 40 independent media investigations corroborated or expounded on our findings, presenting evidence of widespread fraud by Adani against shareholders and Indian taxpayers, as detailed later.

To this day, Adani has still failed to address the allegations in our report, instead providing a response that ignored every key issue we raised and has offered blanket denials of subsequent media allegations.

One might think that a securities regulator would be interested in meaningfully pursuing the parties that ran a secret offshore shell empire engaging in billions of dollars of undisclosed related party transactions through public companies while propping up its stocks through undisclosed share ownership via a network of sham investment entities.

Instead, SEBI seems more interested in pursuing those who expose such practices. This stance is broadly in line with the actions of other elements of Indian government which have sought to arrest 4 journalists for writing critical articles about Adani and expelled members of parliament who were critical of Adani.

Background On SEBI’s Apparent Show Cause Notice

Our understanding from discussions with sources in the Indian market is that SEBI’s surreptitious aid of Adani commenced almost immediately post-publication of our January 2023 report.

Following our report, we were told that SEBI pressured brokers behind-the-scenes to close short positions in Adani under the threat of expensive, perpetual investigations, effectively creating buying pressure and setting a ‘floor’ for Adani’s stocks at a critical time.

When pressed by the public and the Supreme Court to investigate the issues, SEBI appeared to flounder. Initially, it seemed to agree with several key findings from our report. For example, per the Supreme Court case records:

“The entire concern expressed by SEBI (and this precedes the publication of the Hindenburg Report) is that SEBI is unable to satisfy itself that the contributors of the funds to the FPIs are not linked to Adani.”

Later, SEBI claimed to be unable to investigate further. Court documents showed that SEBI had conveniently “drawn a blank” and that further enquiry could be a “journey without a destination,” underscoring its inability or unwillingness to investigate serious allegations against Adani.

The media has reported that SEBI is likely to impose mere token, technical violations on the Adani Group despite the breadth and magnitude of the allegations. In late June 2024, Adani CFO Jugeshinder Singh described some regulator notices aimed toward the group as “trivial,” apparently writing off the prospect of their severity even before the process was concluded.

This confidence may be derived in part through Adani’s relationship with SEBI. Gautam Adani met the SEBI Chairperson Madhabi Buch twice in 2022, becoming “the first high profile businessman” to do so, per The Hindu Business Line.

One of those meetings was to discuss Adani’s $10.5 billion acquisition of cement companies ACC and Ambuja, where, according to Reuters, SEBI had specifically been examining the offshore special purpose vehicles used to fund the transaction, which were later revealed to be linked to Vinod Adani.

The second meeting, reportedly in October 2022 disclosed “no specific agenda” per an earlier Right To Information (“RTI”) request.

Looking to learn more about SEBI’s process, we are in the process of filing an RTI seeking the names of SEBI employees that worked on both the Adani matter and the Hindenburg matter, along with basic details on meetings and calls between SEBI and Adani and its various representatives. We will await SEBI’s response on whether it will provide basic transparency on its investigations.

The Details Of SEBI’s Show Cause Notice

The initial sections of SEBI’s 46-page Show Cause Notice to us outlined background on the Hindenburg report’s publication and an explanation of our relationship with an investor that expressed a short position in Adani.

Much of the notice seemed designed to imply that our legal and disclosed investment stance was something secret or insidious, or to advance novel legal arguments claiming jurisdiction over us. Note that we are a U.S.-based research firm with zero Indian entities, employees, consultants or operations.

Some of these arguments seemed circular. For example, the regulator claimed that the disclaimers in our report were misleading because we were “indirectly participating in the Indian securities market,” and, therefore, were short Adani. [Pg. 30] This wasn’t a mystery—virtually everyone on earth knew we were short Adani because we prominently and repeatedly disclosed it.

While SEBI seemingly tied itself in knots to claim jurisdiction over us, its notice conspicuously failed to name the party that has an actual tie to India: Kotak Bank, one of India’s largest banks and brokerage firms founded by Uday Kotak, which created and oversaw the offshore fund structure used by our investor partner to bet against Adani. Instead it simply named the K-India Opportunities fund and masked the “Kotak” name with the acronym “KMIL”.[2]

Uday Kotak, founder of the bank, personally led SEBI’s 2017 Committee on Corporate Governance. We suspect SEBI’s lack of mention of Kotak or any other Kotak board member may be meant to protect yet another powerful Indian businessman from the prospect of scrutiny, a role SEBI seems to embrace.

SEBI’s “Show Cause Notice”: After 1.5 Years Of Investigation, SEBI Identified Zero Factual Inaccuracies With Our Adani Research

Instead, The Regulator Took Issue With Things Like:

i. Our Use Of The Word “Scandal” When Describing Multiple Prior Instances of Adani Promoters Being Charged With Fraud By Indian Regulators; And

ii. Our Quoting Of An Individual That Alleged SEBI Is Corrupt And Works “Hand In Glove” With Conglomerates Like Adani To Help It Skirt Regulations

Buried all the way down on page 24 of the 46-page notice, SEBI finally touched on the substance of our research, where it made the nebulous allegation that our report “contained certain misrepresentations/inaccurate statements” meant to “mislead readers.”

Such alleged misleading statements are generally the crux of any fraudulent “scheme”, thus these findings would be crucial for a case advanced by any credible regulator.

After 1.5 years of investigation, and undoubtedly countless hours and personnel examining every letter of our 106-page report, SEBI then detailed the supposed inaccurate statements it found:

1. Our report detailed how a Directorate of Revenue Intelligence (DRI) investigation found Adani had engaged in circular trading of diamonds, earning INR 6.8 billion (U.S. $151 million) in illicit export credits. We then described how CESTAT, the tribunal that handles appeals, dismissed the findings, effectively ignoring the earlier DRI conclusions.

SEBI did not allege any aspect of our description was false. Rather, it argued that CESTAT looked at the earlier case and alleged that we “sensationalized or distorted certain facts” by using the word “scandal” to describe the prior alleged INR 6.8 billion scheme by Adani that resulted in a 239-page order from the Commissioner of Customs detailing evidence of fraud, an INR 250 million (U.S. $4.6 million) fine, and extensive subsequent legal proceedings.

Again, they took exception with the fact that we called this a “scandal.”

SEBI also argued that we “cherry-picked facts” by omitting that the Supreme Court later declined to take up the case on appeal, a completely irrelevant piece of information that in no way alters any aspect of our findings.

2. Our report pointed out a 2007 SEBI ruling alleging that promoters of Adani worked with Ketan Parekh, perhaps India’s most notorious stock market manipulator, to manipulate shares in Adani.

Our report explained how Adani Group entities initially received bans for their roles, but these were later reduced to token fines.

Once again, SEBI did not allege any aspect of this was false. Rather, SEBI claimed that it was a misrepresentation to call the reduction in punishment “leniency.” Note that the Cambridge dictionary definition of “leniency” is “treatment in which someone is punished or judged less strongly or severely than would be expected.”

3. An apparently offended SEBI also claimed our report was not false, but rather “reckless” for quoting a banned broker with specific experience dealing with SEBI who detailed how the regulator was fully aware that firms like Adani used complex offshore entities to flout rules on minimum public shareholder ownership, and that the regulator participated in the schemes due to bribes.

SEBI called the source “unreliable” as a banned broker. Note that the sole reason SEBI is aware that the broker was banned is because we volunteered this information up front, writing in our report that the broker was banned in order to give readers the transparency and context needed to make their own judgements on the statements.

Then, with a fairly breathtaking lack of self-awareness, SEBI claimed that “such statements affect market integrity by shaking the trust of investors in the regulatory framework.”

We can’t help but wonder if protecting perpetrators of fraud while attacking those who expose it shakes the trust of investors in the regulatory framework far more than our accurate and fully-contextualized quoting of a source.

4. The remaining issues highlighted by SEBI had nothing to do with the content of our research and were instead focused on technical elements of our disclaimer. For example, SEBI took issue with our disclaimer that fairly described how we were short Adani—through a deal with an investor partner who was indirectly short Adani derivatives through a non-Indian, offshore fund structure.

5. Finally, in an apparent misreading of our report’s disclaimer, SEBI said that we were falsely “claiming objectivity” when we wrote that information in the report is “presented ‘as is,’ without warranty of any kind, whether express or implied…”

Far from “claiming objectivity,” the very disclaimer language cited by SEBI was explicitly a lack of a claim—stating that we made no assurances to quality or other features of the information. In fact, we disclosed a short position in the very first line of our report and prominently again at the end in big bold letters so readers could weigh the potential for bias given that we stood to benefit from a decline in Adani shares. We then encouraged every reader to do their own research.

In brief: As far as alleged “inaccuracies” with our research, that was all SEBI came up with: nothing. We encourage readers to review the notice for themselves and draw their own conclusions.

Since Our Initial Report, At Least 40 Independent Media Investigations Have Corroborated And Expounded On Our Findings Or Have Uncovered New Issues Of Suspected Fraud Or Malfeasance At Adani

That our research stood the test of SEBI’s investigation shouldn’t be a surprise.

While many have tried to wrap our research into a narrative on “Adani vs. Hindenburg,” the reality is that the case moved beyond our initial work long ago. It has now become Adani versus a mountain of evidence, now corroborated and expounded on by dozens of independent media investigations and subsequent events that have supported our findings.

Here is a rundown of many of them:

1. January 29, 2023 – NewsDrum reported that Gautam Adani had failed to disclose his interest in a media channel, India TV, where he appeared for an exclusive interview on January 7, 2023, ahead of the FPO (Follow on Public Offer) in Adani Enterprises. This corroborated a note in our report highlighting an entity connected to Adani (Milestone Tradelinks) that had quietly taken a key stake in India TV.

2. February 1, 2023 – Forbes reported evidence indicating that Adani Group may have funneled its own money via opaque offshore funds to buy into its own follow-on public offering (FPO). This furthered our findings on many of the suspect Mauritius shareholders and corroborated concerns we raised in our reply to Adani, stating “the anchor list of Adani Enterprises investors contains a host of suspect Mauritius funds.”

3. February 2, 2023 – A Guardian article added to our concerns around Elara Capital,learning that one of the directors, a former UK Prime Minister’s brother, Jo Johnson, resigned from the firm. In his resignation, he stated “I now recognise that this is a role that requires greater domain expertise in specialised areas of financial regulation than I anticipated.”

4. February 8, 2023 – A Financial Times article corroborated our assertion that Adani’s leverage posed risks of margin calls, stating that Adani “faced margin call on $1.1bn loan,” per its sources.

5. February 9, 2023 – The Financial Times reported that the MSCI index reduced the index weightings of Adani Group stocks saying “certain investors” in Adani Group “should no longer be designated as free float pursuant to our methodology,” corroborating our findings on offshore stock parking by Adani.

6. February 9, 2023 – Bloomberg released a column raising new questions about suspected Adani offshore stock parking and money laundering entities, validating and corroborating concerns raised in our report.

7. February 13, 2023 – A Wire India article found that Gudami International, an entity owned by a close associate of Vinod Adani, Chang Chung Ling, was mentioned in two ED (Enforcement Directorate) chargesheets in 2014 and 2017 in the AgustaWestland scam (one of India’s largest corruption scandals).

8. February 13, 2023 – AMorning Context article elaborated on reasons why investors were concerned with the transaction we flagged between a Vinod Adani entity (Emerging Markets Investment DMCC) and an Adani Power Subsidiary. “A transaction like this would get flagged,” said a domestic mutual fund head. “This is a governance issue and would not be justified. We would exit a stock like that.”

9. February 14, 2023 – The Financial Times reported that “Gautam Adani has promised to improve oversight of the private family companies that control his business empire,” seemingly in response to issues we had raised about the “network of offshore entities used to facilitate fraud.”

10. February 15, 2023 – A Live Mint article corroborated and expounded on our findings of questionable related-party loans being made by Adani group companies, flagging suspect inter-corporate deposits backed by private Adani entities.

11. February 17, 2023 – A Forbes article evidenced hidden Adani promoter pledges, a key point in our report. Forbes provided new evidence showing that a private Vinod Adani-controlled Singaporean entity pledged Adani promoter stakes for ~$240m in loans from a Russian bank with zero disclosure of these pledges to Indian exchanges.

12. February 19, 2023 – A Fortune article headlined “ESG markets shudder as Adani Group credit arrangements suggest inadvertent financing of heavy polluters,” corroborating our findings regarding Adani Group governance issues and ESG concerns around the financing of the Carmichael Coal Mine in Australia.

13. February 20, 2023 – A disinformation report by the Signpost found that the Adani Group almost certainly manipulated its own Wikipedia entries to puff up its entries with non-neutral ‘PR’ additions.

14. February 22, 2023 – A Bloomberg article corroborated the key role played by Vinod Adani in the business, necessitating disclosure as a related party. The article evidenced that Vinod Adani regularly worked out of the same address as an Adani subsidiary and acted on the Group’s behalf, showing his close involvement in business operations.

15. February 27, 2023 – A Quartz article revealed the role of an Emirati businessman named Nasser Ali Shaban Ahli, with close ties to Vinod Adani, whose name appeared in 2 government investigations into Adani, along with multiple suspected undisclosed related parties of Adani based offshore in China, Dubai, and in tax havens like the British Virgin Islands.

16 February 28, 2023 – A Forbes article outlined how Vinod Adani structured key deals for the Adani Group through a web of entities in Mauritius, the UAE, and the British Virgin Islands, further cementing Vinod’s role as a key related party. It also learned that Vinod is an Indian citizen, contradicting Adani filings.

17. March 2, 2023 – An article in Adani Watch corroborated issues we raised around Chang Chung Ling, who was closely tied to Vinod Adani. The article uncovered that “an entity linked to the Adani Group financially supported a company [owned by the sons of Chang Chung Ling] that violated sanctions imposed by the United Nations Security Council (UNSC) on trade with North Korea.”

18. March 6, 2023 – An article in Live Mint further evidenced concerns about AdiCorp, a small company that had been funnelling money between Adani group companies, stating the transactions with AdiCorp “invokes questions of propriety” over shared relationships with Adani.

19. March 16, 2023 – An Indian Express article found that opaque, Mauritius-based Elara Capital co-owned a defense firm with Adani through a multi-layered structured and was the largest indirect shareholder, reinforcing concerns we raised about the nexus of Adani and Elara Capital.

20. March 23, 2023 – The Financial Review released an investigation revealing hundreds of millions in accounting inconsistencies across Adani’s coal projects in Australia, corroborating our findings.

21. March 24, 2023 – The Financial Review released a follow-up article discussing suspicious impairments in Adani’s Australian entities including dealings with privately controlled entities of Vinod Adani, further corroborating findings in our report.

22. March 25, 2023 – An investigation by The Wall Street Journal detailed the extensive role Vinod Adani played in the Adani Group, and interviewed a former employee of PMC Projects, an entity identified in our report as a “dummy firm” of Adani. The former employee told the WSJ how he created fake and inflated invoices for the entity.

23. March 27, 2023 – An article in Adani Watch detailed how an entity tied to close Adani associate, Chang Chung Ling, had been named by the Central Bureau of Investigation in an alleged criminal conspiracy relating to a coal tender process in Andhra Pradesh. The company – Vyom Tradelinks – was described as a proxy for Adani.

24. April 4, 2023 – An investigation by The Scroll found that the only other bidder in a Maharashtra coal auction won by Adani in March 2023 was connected to Adicorp, raising further questions about the nexus between Adani and Adicorp.

25. April 6, 2023 – An article in Adani Watch provided further detail on the close relationship between Adani and PMC Projects – an entity we believe was an undisclosed related party “used to suck money out of the Adani Group’s publicly listed entities.” The article showed the PMC was working out of an Adani Group office and even used an Adani corporate email address.

26. May 3, 2023 – The Australia Broadcasting Corporation released an investigation headlined “Adani proposed coal ventures to sanctioned Myanmar military despite public vow to cut ties,” flagging how Adani’s actions contradicted its public claims.

27. May 30, 2023 – The Indian Express reported that two offshore funds, Mavi Investment (now APMS) and Lotus Global had been on the radar of Income Tax authorities in India for over a decade, with its owners, Monterosa, petitioning the Supreme Court to block the release of information. This corroborated our view of the surreptitious ownership of Adani stock held in its fund entities.

28. June 18, 2023 – Bloomberg reported on Adani’s undisclosed related party transactions with its law firm, CAM. Gautam Adani’s daughter-in-law, Paridhi Adani, advised on Adani deals at law firm CAM, her father’s firm, where she is a partner. Note that Adani responded to our report by saying an “independent” law firm gave it the all-clear, without naming the firm. Bloomberg asked if the claimed “independent” firm was CAM. Adani failed to answer.

29. June 22, 2023 – Bloomberg reportedthat the U.S. Department of Justice and the SEC were probing Adani. The article, headlined: “Adani Group Draws Regulatory Scrutiny in the US After Short Seller Report” wrote that both agencies were said to be scrutinizing Adani’s disclosures to US investors.

30. June 23, 2023 – A Bloomberg article outlined glaring red flags with Adani’s “fragmented” audit structure, which has roughly 40 different firms auditing different parts of the conglomerate. The article also outlined how Ernst & Young affiliate partners refused to audit Adani Power over credibility concerns.

31. August 30, 2023 – The Financial Times, Guardian, and OCCRP uncovered that 2 offshore funds owning at least 13% of the free float in multiple Adani stocks were secretly controlled by associates of Vinod Adani, masking the relationship with 2 sets of books. This provided yet more evidence to support our findings that offshore entities tied to Adani group surreptitiously own stock, in violation of SEBI’s listing rules.

32. September, 27, 2023 – The Indian Express, reported that an underlying shareholder of Opal Investment, a substantial investor in Adani Power, was a single person company based in UAE. It stated that Opal “built a website after the Mauritius fund was linked to the Adani Group” in our report, despite having been in existence for 18 years. This supports our view that Opal was yet another front for Adani.

33. October 11, 2023 – According to an investigation by Reuters, documents from the British Virgin Islands further supported our allegations of Adani’s undisclosed promoter shareholdings. The documents showed that an Adani related-party entity (Ezy Global) merged with an alleged front company and public shareholder in Adani group companies (Gulf Asia Trade & Investment) run by key associate Nasser Ahli.

34. October 12, 2023 – A Financial Times investigation found through an analysis of export records that Adani had been inflating fuel costs by importing billions of dollars of coal through offshore middlemen entities at elevated prices.

35. October 14, 2023 – Mint reported that the government is probing the accounts of the group’s two airports in Mumbai. This further supported our view that Adani’s financial statements could not be relied upon.

36. October 30, 2023 – An article by Morning Context shone the light on another suspected related party distributor. An expert quoted believed Adani Group had misled its auditors over its disclosures. This corroborated our view of Adani’s open and repeated violation of Indian disclosure rules.

37. November 1, 2023 – An article in the Financial Times highlighted changes in India’s foreign investor rules introduced by SEBI after our report on Adani. The Financial Times stated that the regulatory changes came after our findings on Adani’s “ties to a series of obscure foreign funds.” The article even carried a quote from Cyrill Shroff, father-in-law of Adani Ports CEO, criticizing the move to greater transparency.

38. November 18, 2023 – Reuters reported that India is seeking to restart its stalled investigation into Adani’s role in the U.S. $4.4 billion coal invoicing scam. According to allegations in legal documents, Adani “thwarted” Indian government agencies attempt “to collect evidence from Singapore,” corroborating our view that government action has consistently been stalled or stonewalled by Adani. The article stated that our report was the catalyst for the renewed focus.

39. December 1, 2023 – Adani Watch uncovered exclusive documents showing that funds routed out of Adani group companies ended up in a complex network of companies and funds controlled by Vinod Adani, including sub-classes of bank accounts in Switzerland. This supported our view that Vinod Adani’s network served two key functions in stock parking/manipulation and money laundering in collusion with the Adani Group.

40. December 12, 2023 – Bloomberg reported that a controversial contractor of Adani, PMC Projects, had folded into a new company, Howe Engineering, after regulatory investigations by India authorities. Both entities were owned through an offshore entity in Mauritius, tied to Chang Chung-ling. Adani refused to detail where money paid to the contractors ended up. This corroborated our view that Adani used closely tied contractors to suck money out of the publicly listed entities with no disclosure of the conflict to investors.

41. March 15, 2024 – Bloomberg reported that U.S. prosecutors had expanded its probe into Adani to include potential issues of bribery.

42. May 21, 2024 – The FT and the OCCRP reported new evidence alleging that Adani had sold low-grade coal as high-value fuel in order to defraud Indian state utility companies, citing detailed shipping, export, and entity records.

The Show Cause Notice Does Resolve Some Questions: Did Hindenburg Work With Dozens Of Firms To Short Adani, Making Hundreds Of Millions Of Dollars?

No—We Had One Investor Partner, And Net Of Costs We May Barely Come Out Above Breakeven On Our Adani Short

Our Work On Adani Was Never Justifiable From a Financial Or Personal Safety Perspective, But It Is By Far The Work We Are Most Proud Of

Strategic media leaks that appear to stem from SEBI and the ED previously implied that we generated a massive financial windfall from our Adani shorts.

Prior media have cited sources close to SEBI and the ED who implied that we had 12 or even 16 investor partners in our Adani work. Collectively, according to the sources, those parties generated hundreds of millions in gains. The sensational headlines and strategic ‘leaks’ suggested that we clocked a massive windfall from our report.

The reality, as detailed in the show cause notice, is less dramatic. We only had one investor relationship in our Adani thesis, as is customary for our approach and as we have discussed in multiple public interviews.

We have made ~$4.1 million in gross revenue through gains related to Adani shorts from that investor relationship. We made just U.S.~ $31,000 through our own short of Adani U.S. bonds held into the report. (It was a tiny position.) [3]

Net of legal and research expenses (including time, salaries/compensation, and costs for a 2-year global investigation) we may come out ahead of breakeven on our Adani short.

With a rise in the killing or jailing of journalists in India, and a plummeting of press freedom scores in the country, we anticipated that the apparatus of Indian government may concoct a case to attempt to scare us or others out of the market, or worse.

We knew these risks before we started. Ultimately, that didn’t matter in the face of our resolve to publish in the public interest once the work met our evidentiary standards.

There was never a point where the Adani thesis was financially justifiable for us. It was even less justifiable from a personal risk and safety perspective.

But, to date, our research on Adani is by far the work we are most proud of.

A Wake Up Call On Corporate Governance And Regulatory Enforcement In India

Short selling has long been recognized as a legitimate practice in India as it is around the world. PJ Thomas, the First Economic Advisor to Independent India in 1948 wrote:

“Short selling like other forms of speculation fulfils a legitimate purpose…One of the most essential functions of organised markets is to reflect the competent opinions of all competing interests. To admit only opinion looking to higher prices is to provide a one-side market.” [Pg. 67]

Nowhere is this better illustrated than with Adani Group stocks.

SEBI’s job as a securities regulator is to detect and stop the types of malfeasance that we exposed.[4]

In our view, SEBI has neglected its responsibility, seemingly doing more to protect those perpetrating fraud than to protect the investors being victimized by it.

These actions send a clear message to every public company in India: Are you having a difficult time with your quarterly results? Do you want your stock price to be higher? (Who doesn’t?) Simply have your brother or another relative set up an offshore shell empire to buoy up the stock or rosy up your financials.

The incentives are clear: The gains from fraudulent activities outweigh the small risks of a potential ’slap on the wrist’ fine from regulators. And based on the hundreds of tips and leads we received following the Adani report, Adani is by no means the only lurking and ongoing issue SEBI has failed to address.

The message sent to investors in India is equally loud: You have no real protection from fraud. Corporate governance in India is a myth for businessmen that can buy influence.

Meanwhile, the government has once again sent the message that critics of those in power will be punished, whether by regulatory action or strategic media leaks. We expect SEBI may try to impose ‘bans’ or fines on us to clamp down on the prospect of more criticism of Indian companies.

Regardless of these intimidation efforts, we will continue to speak up about malfeasance at companies anywhere across the globe if it is warranted by the evidence.

Conclusion

At Hindenburg, we work tirelessly to root out fraudulent business practices and corporate wrongdoing. Our reports focus on evidence, without taking political sides. We view India as a vibrant country with unlimited economic potential that faces issues of fraud and corruption, just as all countries do. We believe transparency is always the best remedy and are grateful that our efforts have had a meaningful impact.

We want to thank our readers in India for sending us hundreds of letters of support, tips, leads, and ideas (also thousands of CVs even though we are not hiring at the moment.) We read every single outreach and are humbled by, and greatly appreciate the support.

Legal Disclaimer

This report does not constitute a recommendation on securities. This report represents our opinion and investigative commentary and we encourage every reader to do their own due diligence. Use of Hindenburg Research’s research is at your own risk. In no event should Hindenburg Research or any affiliated party be liable for any direct or indirect trading losses caused by any information in this report. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities covered herein. You should assume that as of the publication date of any short-biased report or letter, Hindenburg Research (possibly along with or through our members, partners, affiliates, employees, and/or consultants) along with our clients and/or investors has a short position in all stocks or bonds (and/or derivatives of the stock) covered herein, and therefore stands to realize significant gains in the event that the price of any security covered herein declines. Following publication of any report or letter, we intend to continue transacting in the securities covered herein, and we may be long, short, or neutral at any time hereafter regardless of our initial conclusions, or opinions. This is not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction. Hindenburg Research is not registered as an investment advisor in the United States or have similar registration in any other jurisdiction. To the best of our ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the stock covered herein or who may otherwise owe any fiduciary duty or duty of confidentiality to the issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Hindenburg Research makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. All expressions of opinion are subject to change without notice, and Hindenburg Research does not undertake to update or supplement this report or any of the information contained herein.

[1] It is still not entirely clear whether the emails are genuine, as email is not generally considered typical ‘service.’

[2] KMIL stands for Kotak Mahindra Investment Limited

[3] Note that the show cause notice included bond trades that fell outside the range of report publication, which seem irrelevant. But based on their calculations we made even less.

[4] See Securities and Exchange Board of India Act, 1992 (As amended by the Finance Act, 2021 (13 of 2021) w.e.f. April 1, 2021). SEBI’s functions include “prohibiting fraudulent and unfair trade practices relating to securities markets.” [Pg. 10]